Housing news is better for buyers when it comes to inventory, a slower pace and seller concessions

Affordability remains a challenge amid higher interest rates and economic uncertainty

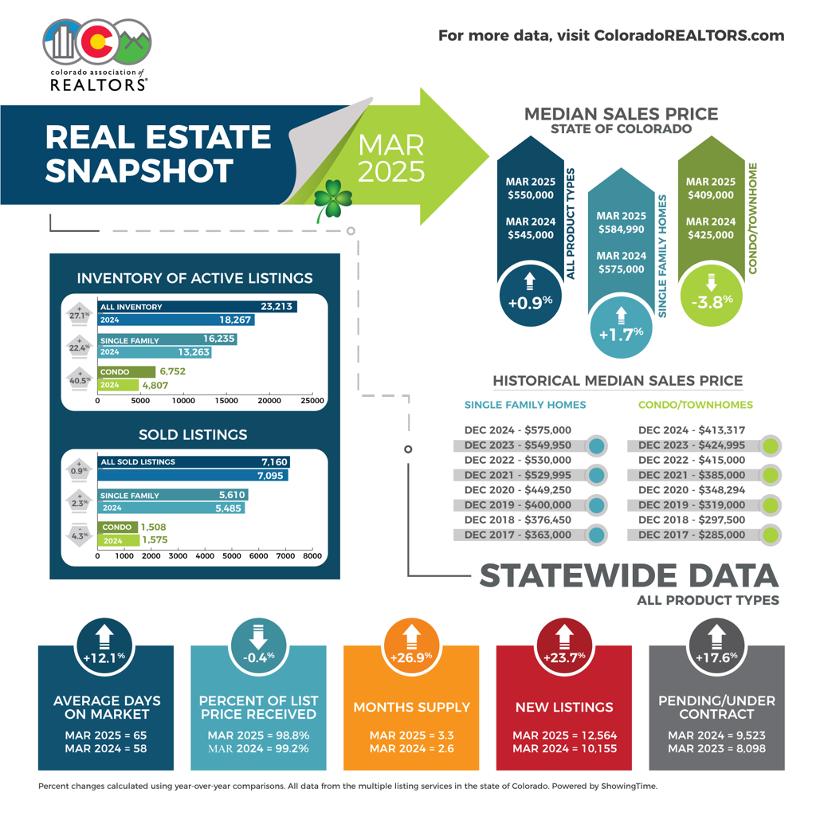

ENGLEWOOD, CO – With an influx of new listings and inventory of active listings well above where housing inventory stood a year ago, the longer-term march toward a more balanced buyer seller market continued in the past month, according to the latest Market Trends Housing Report from the Colorado Association of REALTORS® (CAR) and analysis from the Association’s spokespersons across Colorado.

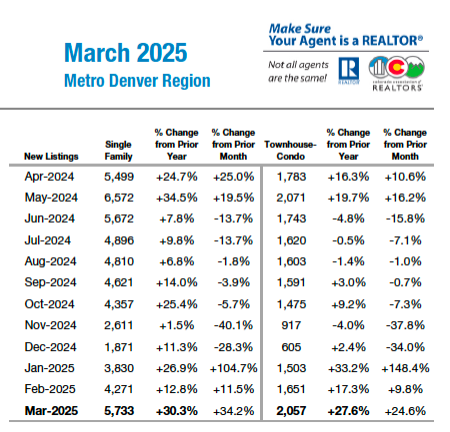

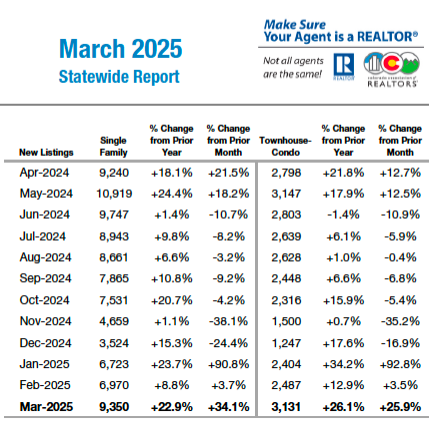

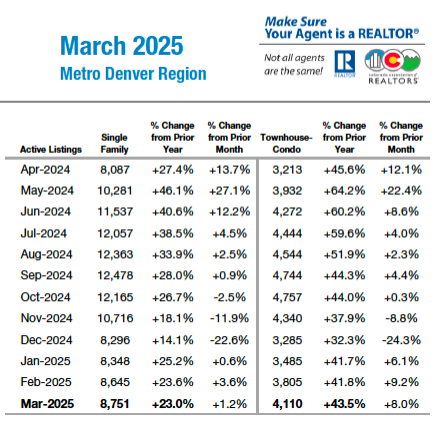

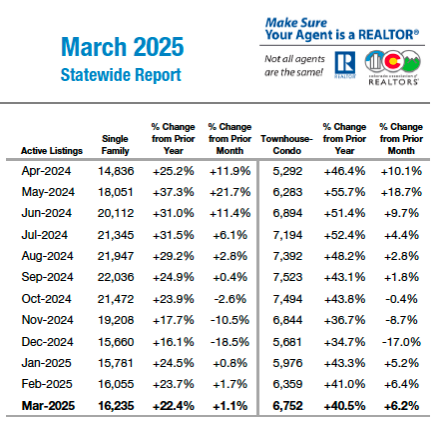

In the seven-county Denver-metro area, 7,790 new listings (5,733 single family/2,057 condo-townhome) hit the market, up nearly 30% from the same time last year. The more than 12,800 active listings across the Denver-metro area in March reflect a 29% increase over March 2024. Statewide, there were roughly 12,500 new listings (9,350 single family/3,131 condo-townhome) up 23.7% from a year prior and active listings rose just shy of 27% from a year prior with 23,213 in the inventory.

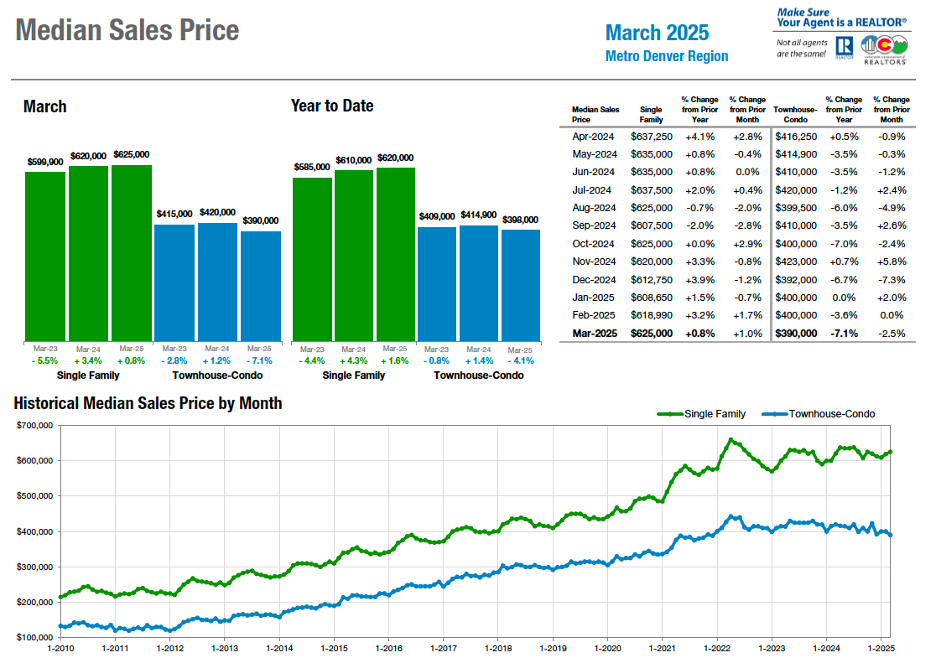

Looking to median sales price, single-family homes in the seven-county Denver area ticked up just 1% from February to March at $625,000 which is also up just less than 1% from a year ago. Condo-townhome median price fell 2.5% from February to March and is down more than 7% from a year prior at $390,000.

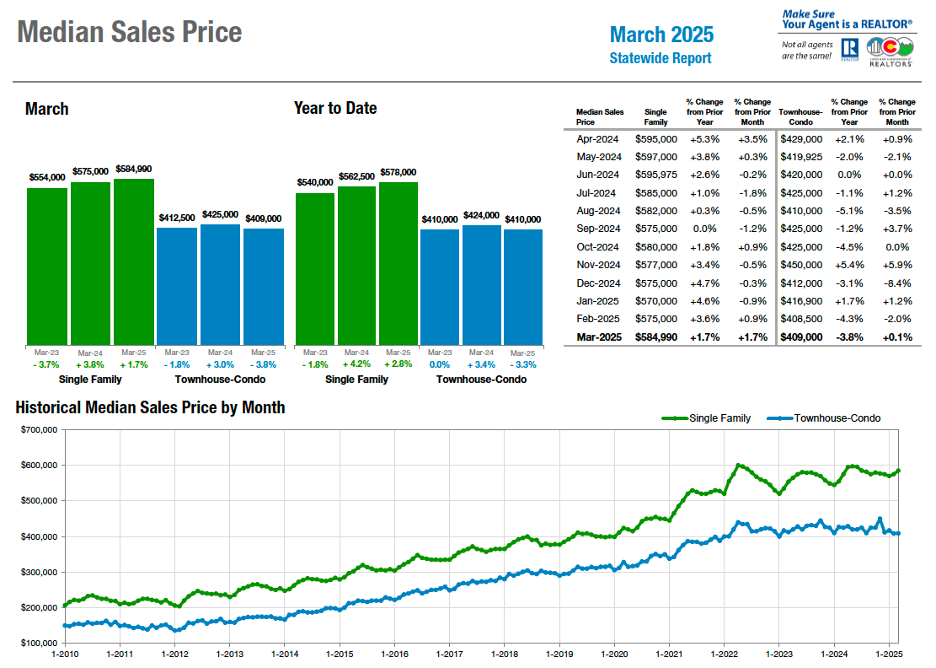

Statewide, the median price of a single-family home hit $584,990, a 1.7% bump in the past 30 days, as well as compared to March 2024. For the condo-townhome market, pricing ticked up 0.1% from February to March however, the $409,000 median is down 3.8% from a year ago.

While homes began to move a little faster from February to March, the overall pace has slowed significantly from just a year ago. In the seven-county Denver area, single-family and condo-townhome average days on market came in at 54, up more than 20% from where things stood in March 2024, 33 days for single family and 37 days for condo-townhome. Statewide, the 64 average days on market for single family is up 12.3% from the 49-day average a year ago. For condo-townhomes, the statewide average of 66 days is up nearly 14% from the 50-day average in March 2024.

“All this is to say that we are in a balancing market and buyers and sellers are having to negotiate together more than any time in the last decade. Location, condition, timing, and urgency all play important roles in how buyers buy and how sellers sell. Pricing isn’t just based on what the historical data says – there are numerous variables at play when determining the ‘sweet spot’ for a house price,” said Fort Collins-area REALTOR® Chris Hardy.

Overall, the news is better today for buyers than it has been in several years when it comes to inventory, a slower pace and ability to find seller concessions however, median pricing remains stubbornly elevated. Affordability and a growing level of economic uncertainty are keeping many prospective buyers on the sidelines once again as we move deeper into the traditional spring buying season.

“The current economic unrest has led to doubts among potential buyers, dampening what would otherwise be a robust buyer pool. This imbalance between supply and demand is impacting prices, leading to a more cautious market overall. There are a few quick sales here and there and even an occasional bidding war but the market for the most part, belongs to the buyers these days, as they have the upper hand,” said Boulder/Broomfield-area REALTOR® Kelly Moye.

“The market pressures are particularly pronounced in the affordable housing segment. While the foothills market offers a mix of affordable and luxury options, the condo and townhome market is particularly stressed. Issues with condo insurance and a lack of new affordable housing have contributed to a 50% increase in inventory, leading to noticeable price drops,” said Evergreen-area REALTOR® Julia Purrington Paluck.

“Last month, it appears more sellers acted upon their recent conviction than buyers, with a notable spike in inventory. Even if fewer buyers are ready to make a move, real estate markets tend to ‘push and pull’ towards equilibrium. When more inventory is available and sellers are forced to compete, buyers gain the confidence to enter the market with greater options and negotiating power,” said Denver County-area REALTOR® Cooper Thayer.

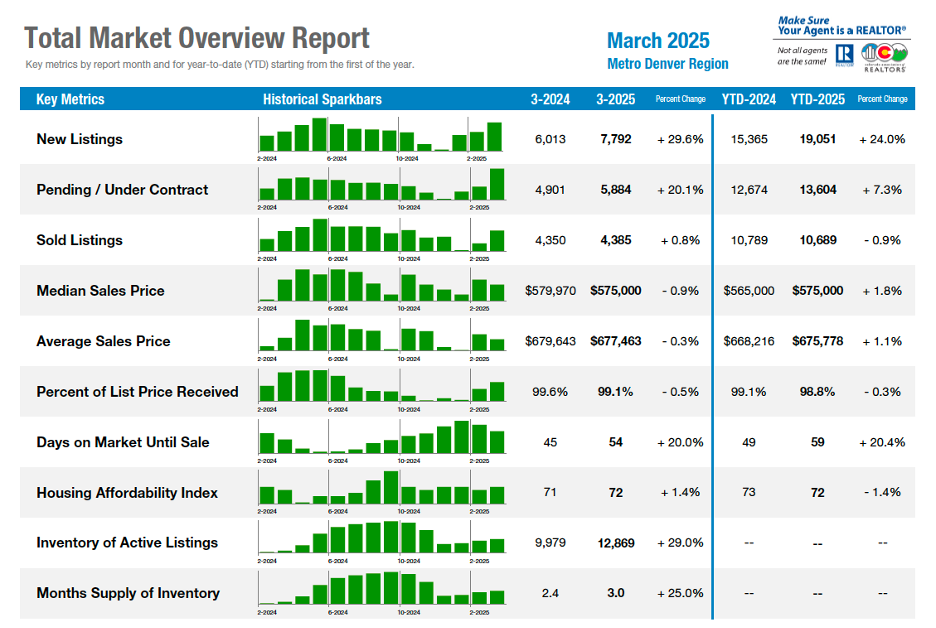

Total Market Overview – Seven-County Denver Metro

Total Market Overview – Statewide

NEW LISTINGS – DENVER METRO AREA

NEW LISTINGS – STATEWIDE

ACTIVE LISTINGS – DENVER METRO AREA

ACTIVE LISTINGS – STATEWIDE

MEDIAN PRICE – DENVER METRO AREA

MEDIA PRICE – STATEWIDE

LOCAL MARKET SUMMARIES

Taking a more in-depth look at some of the state’s local market data and conditions, the Colorado Association of REALTORS® Market Trends spokespersons provided the following assessments:

AURORA

“Typically, a big month and an exciting indicator of what lies ahead, March turned out to be lackluster when it comes to home sales. Overall, inventory is up about 8% and prices have remained about the same. We’re seeing a few zip codes up 1-2% while others are down 1-2%.

“The median price in Aurora is $534,000 with average days on market at 58 as it feels more and more like the market is shifting to a buyer’s market. With inventory and days on market up, we’re seeing a sound window for buyers. Not only do buyers have more choices at basically the same price, they also have longer to think about their choice, and they’re starting to see some lower interest rates – with FHA’s right at 6% – down from the 7% and 8% that we have recently seen.

“Looking at specific zip codes around the city, we see median pricing for single-family residential in 80010 (original Aurora) at $433,000; 80013 (Central Aurora) median price is $504,000; 80015 (South Aurora) median price is $535,000; 80016 (Southeast Aurora) $834,000. In the Englewood, Greenwood Village 80111 zip code, we have a median price of $1.365 million, up 17% over this time last year. Adams County median pricing is down year over year at $529,900. Arapahoe County median price on single family residential is $585,000, up over 2024.

“The condo/townhome market is also a great option for buyers. In most of the Aurora/Arapahoe County/Adams County zip codes the number of condos/townhomes available is up significantly while pricing is down. Yes, real estate is all about location however, the window for buyers is definitely open at this time. This is the best market for buyers that we’ve seen in the past 5 years,” said Aurora REALTOR® Sunny Banka.

BOULDER/BROOMFIELD COUNTIES

“The real estate market in Boulder and Broomfield counties is experiencing a significant uptick in inventory, with new listings flooding the market in preparation for a strong spring season. Boulder County has seen a 15% increase in inventory, while Broomfield is up 11%. Despite many sellers holding off due to low interest rates, the rise in available homes signals more opportunities for buyers. However, ongoing economic uncertainty has kept many buyers hesitant, resulting in a drop in sold listings across both counties.

“While Boulder County has seen flat prices so far this year and a rise in days on the market to 75 days, Broomfield’s market is performing slightly better with a 6% increase in home prices and a faster average days-on-market of 50 days. The affordability in Broomfield continues to attract more buyers, helping to sustain the area’s real estate market. However, the current economic unrest has led to doubts among potential buyers, dampening what would otherwise be a robust buyer pool. This imbalance between supply and demand is impacting prices, leading to a more cautious market overall. There are a few quick sales here and there and even an occasional bidding war but the market for the most part, belongs to the buyers these days, as they have the upper hand,” said Boulder/Broomfield-area REALTOR® Kelly Moye.

COLORADO SPRINGS

“The housing market continues to be resilient despite a 28% increase in March listings compared to a year ago and economic uncertainties including tariff talk that is both in and out of the news. Home values continued to rise, and we sold 10% more homes year over year most likely as result of the pull back on interest rates pulling buyers off the sidelines.

“Nationwide, we have begun to see consumer charge-offs jump 6.3%, the highest level in 13 years. This does seem to show some stress on the consumer when we tie that to automobile delinquencies at their highest level since 2009. Federal spending is also setting records. But these numbers are not reflected in the housing statistics. The housing market currently continues to buck this trend, even though days on market increased 9.3%, values continue their trend up in our area.

“As we hit April, we have tariffs hitting, trade wars going, stock market fluctuations that would make one sick. Gold shot up to record highs and then pulled back. Bitcoin pulled back along with the stock market. I believe we are in uncharted territory, and it is anyone’s guess on where we go now. While preparing this analysis, the 10-year yield shot up 50 basis points in 48 hours. I’m guessing that, until that settles down and we start to see some balance, buyers may once again pause. While we leave March in the rearview mirror, April will be a very interesting month to watch housing, stocks and the overall economy,” said Colorado Springs-area REALTOR® Patrick Muldoon.

COLORADO SPRINGS

“Amid an incredibly chaotic political and economic environment, horrendous inflationary and affordability challenges, and unprecedented job uncertainties, in March 2025, the Colorado Springs single-family and patio homes real estate market saw an astounding sales increase of 45.1% compared to the previous month. Both monthly and year-to-date sales volumes reached the highest levels for March since March 2023. Additionally, the average and median prices for March were at record-high levels, and a record-high inventory in March since March 2014, with a 40.7% increase year-over-year. Likely, fear of the forecasted ridiculous increases in home building costs is driving on-the-fence buyers to purchase now.

“The abundance of available homes presents a fabulous opportunity for buyers to find properties that suit their preferences. It also allows them to negotiate more favorable offers with motivated sellers,” said Colorado Springs-area REALTOR® Jay Gupta.

Key Highlights from the Colorado Springs Market:

- Active Listings – Supply: In March 2025, 2,629 single-family and patio homes were for sale in Colorado Springs on the Pikes Peak MLS. It represented an enormous 40.7% increase year-over-year and an 8.4% increase compared to the previous month. The inventory level was the highest for March since 2014. The overall months’ supply of active listings stood at 2.5 months. For homes priced under $400,000, the supply was quite low at 2 months. Homes priced between $400,000 and $600,000 also experienced low supply at 2.2 months. In the price range of $600,000 to $1 million, the supply was healthy at 3 months. However, for homes over $1 million, the supply was healthy at 4.7 months.

- Sales – Demand: Last month, 1,059 single-family and patio homes were sold in the Colorado Springs area, representing a massive increase of 45.1% compared to the previous month and a healthy 12.5% increase compared to March last year.

The monthly sales volume increased enormously by 50.0% from the previous month and 20.0% year-over-year. Year-to-date sales volume increased astoundingly by 72.1% compared to last year. Compared to March 2015, 10 years ago, the monthly and year-to-date sales volumes have massively increased by 127.7% and 126.9%, respectively.

- Days on the Market: The average number of days on the market in March 2025 was 62, same as last month and 56 days in March last year.

- Sales by Price Range: Last month, 25.0% of homes sold were priced under $400,000, while 45.3% sold for between $400,000 and $600,000. Homes priced between $600,000 and $1 million accounted for 24.1%, and those over $1 million represented 5.6% of the sales.

Comparing March 2025 to the previous year, there was a minute 0.2% increase in the sale of single-family homes priced under $400,000 and a healthy 22.0% increase in homes priced between $400,000 and $600,000. And, a substantial 33.2% increase in homes priced between $600,000 and $1 million and a robust 90.3% increase in homes sold for over $1 million.

- Average & Median Sales Prices: Last month, the average and median sales prices of single-family and patio homes reached historically high levels for March, at $562,548 and $495,000, respectively. The average sales price rose 6.6% year-over-year, 44.0% since March 2020, 5 years ago, and an impressive 116.9% increase since March 20115. Similarly, the median sales price climbed 5.3% year-over-year, 40.5% since March 2020, 5 years ago, and an incredible 120.0% increase since March 20115.

- Price Reductions: Last month, 37.5% of active listings in El Paso County and 30.0% in Teller County had price reductions. While the market is still doing well, sellers must price their homes competitively and stage them attractively to entice buyers.

DENVER METRO (11-County)

“After a slower start to the year, listing activity in the Denver-metro area has finally picked up pace with over 7,700 new listings hitting the market in March, and home prices holding steady despite a daunting economic environment. Each month that passes without reprieve from near 7% mortgage rates, more and more homebuyers and sellers are becoming acclimated to the ‘new normal’ in the real estate market. Last month, it appears more sellers acted upon their recent conviction than buyers, with a notable spike in inventory. Even if fewer buyers are ready to make a move, real estate markets tend to ‘push and pull’ towards equilibrium. When more inventory is available and sellers are forced to compete, buyers gain the confidence to enter the market with greater options and negotiating power.

“In March, about 3,400 single-family homes sold at a median price of $625,000, a moderate 0.8% increase over March of last year. Around 2.6 months of inventory are currently active for sale, presenting a fairly balanced market by the Denver metro area’s historically competitive standards. Patience is key for sellers this spring, as the average time on market currently sits at around 54 days, a 20% jump from this time last spring. However, even with more homes to compete with and more days with a sign in the yard, a relatively normal number of closings are occurring each month.

“Townhouse and condominium sellers aren’t as lucky as their single-family counterparts, currently experiencing a similar spike in inventory but with a year-over-year decline in sold listings of about 6.8%. High HOA dues, as a result of rising insurance and maintenance costs, are forcing sellers to compensate to make their listings attainable for buyers, which has pushed median sale prices down more than 7% since last spring. Buyer motivation is lagging in this segment, and my advice to sellers is to price moderately, and go the extra mile to make your home stand out amidst over 4.3 months of condo/townhouse inventory,” said Denver County-area REALTOR® Cooper Thayer.

CRESTED BUTTE/GUNNISON

“The first quarter of 2025 has been slow and steady in the Gunnison and Crested Butte real estate market. The Crested Butte area had just two more sales this year than last (51 vs. 49) resulting in $3 million more in volume ($73 million vs. $70 million). The Gunnison area had an 8% increase in sales (103 vs. 95), but a 19% drop in dollar volume ($97 million vs. $120 million).

“Unlike other areas of the state, we have not seen a big increase in inventory. The Crested Butte area inventory is actually down about 6% overall with the number of single-family homes for sale down about 17% from this time last year. As the snow melts and we wait for our busy summer season, I anticipate new properties to come on the market in the coming months. In the Gunnison area, overall inventory is up 18% and the number of single-family homes for sale is up 50% from April 2024. Buyers in the Gunnison area should be actively looking to see if their dream home is for sale.

“In a smaller market like ours, average and median prices can be skewed if there are more or less high dollar sales, and we have a lot of micro markets where buyers and sellers should be homing in on to determine what price makes sense. For this reason, to get an idea of the market trends, it can be helpful to look at price per square foot. This is a not always a good method to price a specific property, but it can give you an idea of how things look overall.

“In the Crested Butte area, prices continue to go up. The average price per square foot for sold single- family homes was $832 in 2024 and is $869 for the first quarter of 2025. The average asking price per square foot for single-family homes is $1,166. This could reflect that the homes that are for sale now are newer construction or have higher end finishes or it could be that sellers need to look more carefully at what buyers have actually been willing to pay. With building costs being quoted at $800 – $1200 per square foot, buying an existing residence could be a better option if you find something you like.

“Looking at condos at the ski area, there is a similar trend. The average price per square foot for sold condos in 2024 was $640 and that has increased to $745 for the 1st quarter of 2025. The average asking price per square foot for condos in Mt. Crested Butte is $899. Like many other areas of Colorado, homeowner association dues are increasing as insurance is going up along with maintenance costs. Increasing dues could result in prices coming down as buyers want to adjust their purchase price to accommodate those ongoing expenses, but that has yet to materialize.

“In the Gunnison area, prices are adjusting a bit. The average price per square foot for sold single-family homes has dropped 8% comparing 2024 to the first quarter of 2025 (from $448 to $413). The average asking price per square foot for single-family homes is $483.

“In general, Crested Butte and Gunnison continue to be attractive for buyers. We are hopeful that we will see increased inventory this summer to give those buyers more to choose from and give sellers an opportunity to cash in on the appreciation they have seen over the last 5-10 years,” said Crested Butte-area REALTOR® Molly Eldridge.

DURANGO/LA PLATA COUNTY

“As we head into spring in La Plata County, the burst of activity we experienced is settling into a year that’s still a bit more active, but a lot like the last as far as the numbers show. With a virtually snowless winter, people listed their homes earlier than usual in the rural areas. Overall, in 2025, the county had 28% more new listings, but March slowed and new listings only outperformed March 2024 by four homes. Rural Durango had 50% more listings to come on market year to date over last year; neighboring Silverton/San Juan County had 82% more early-season listings than 2024 year to date.

“While buyers also became active early, and sales generally tracked in single-family, condos and townhomes have had a rough go in 2025 thus far. While the number of new listings was 5% greater year to date, sales were down 21% in number of units sold. March was particularly off, with 47% fewer closed sales than March 2024. This resulted in inventory climbing to over four months’ supply of homes, making the market lean still closer to a buyer’s market than it has been in some time.

“The median price in the county has climbed 6% since March 2024 for single-family homes and has declined 8% for condos and townhomes. This is just a snapshot of the homes that sell in a certain month, but give a general idea of pricing. The median price of a single-family home in-town Durango is currently $812,500, and in-town Bayfield $522,000.

“Our Purgatory Resort area homes are hurting with 16 new single-family listings in 2025 and still zero sales. Buyers aren’t purchasing condos and townhomes, instead, the sales of that segment decreased 25% in number. Four single-family homes currently show under contract and we should have sales to review by the end of the ski season.

“The unknowns, as we come more steadily into our selling season, will be the effects of stock market crash and partial rebound, the chaos of the tariffs, and other economic uncertainty. There is word from those in the tourism industry that bookings are sharply down for the summer so far. While we see many sales due to second homes, we sell more than half our homes to the residents already in our county. Will we see a pause in people making life changes with uncertainty of jobs, economy, and recession talk, or will there remain a buildup of residents wanting to make a change? Will those who have put off moving to enable them to keep their 3% current mortgage now realize they have stuck with their homes longer than is comfortable and the urge to move overcomes the uncertainty of the economy? The next few months will tell. My prediction is the people who can move will still decide to ‘move’ forward,” said La Plata County-area REALTOR® Heather Erb.

EVERGREEN/MOUNTAIN METRO

“Inventory is back on the rise as new listings hit the market at an accelerating pace and sales remain steady. After years of low inventory, the situation is now healthy and balanced. Although we continue to see seasonal fluctuations in new listings, contracts, and closings, one trend from the past year stands out: active listings are increasing at a higher rate than closings. As a result, both months of inventory and days on market are steadily increasing.

“Currently, the overall Mountain Metro Market has about three months of inventory—up from 2.1 just a month ago and significantly higher than two years ago. Notably, this year’s seasonal low in December and January still exceeded the inventory peak seen in 2021. Over the last five years, our rolling 12-month average of monthly supply has risen from under one month to nearly 3.5 months. It’s important to clarify that this does not indicate a full buyers’ market, nor are prices falling. In fact, both the median and average sales prices in the entire foothills market have increased over 3% year over year, now sitting at $720,000 and $840,000, respectively. In the Conifer-Evergreen area, the average price has soared by nearly 10%, reaching $1.17 million.

“Many agents in the region agree that while the market is bustling—with numerous showings, offers, and even multiple offers—sales (closings) are lagging behind this activity. We are witnessing multiple offers below asking price, deals that don’t reach agreement, and some that fall apart due to inspection or insurance issues. Negotiations are becoming more complex and take longer to finalize. Currently, the number of price decreases in the market is on par with the number of new listings and pendings, while over 10% of pending listings are returning to the market.

“These trends likely stem from the rising cost of living, especially housing, which is increasing faster than wages. Buyers face challenges with higher interest rates and insurance costs, while sellers need to achieve ‘top dollar’ for their existing homes to afford their next purchase. Many sellers are transitioning from homes with low interest rates to new properties at higher rates, potentially leading to less value for a larger payment.

“The market pressures are particularly pronounced in the affordable housing segment. While the foothills market offers a mix of affordable and luxury options, the condo and townhome market is particularly stressed. Issues with condo insurance and a lack of new affordable housing have contributed to a 50% increase in inventory, leading to noticeable price drops. Conversely, the luxury market (properties over $2 million) has seen a rise in active listings but a decrease in days on market over the past year. This segment is thriving as buyers are generally cash buyers and are not affected by higher interest rates, with pending listings in March nearly doubling from a year ago, indicating a robust and growing market since January 2024,” said Evergreen-area REALTOR® Julia Purrington Paluck.

FORT COLLINS

“The ‘sweet spot’ is defined as ‘an optimum point or combination of factors or qualities.’ In sports, it’s that point on a bat, racket, or golf club that provides the optimum transfer of energy to the thing being struck. In real estate sales, the sweet spot is generally the price of a home that creates the most interest to attract offers.

“This month’s sales data showed a marked increase in listings; up nearly 20% compared to last March. This trending increase in inventory warrants a look at pricing and how important the right price is when sellers find themselves in a competitive market for buyer’s eyeballs. Is there a ‘sweet spot’ for pricing a home within a given price bracket? With the median price in the Fort Collins area hovering at $605,000, there are an equal number of sales above and below that number. In a bell curve graph, $605,000 would be at the top of the ‘bell.’ Yet when you look at the number of days it takes to get an offer on a given property, the average for March was 32 days. This is a far cry from the heyday of 2022 when most homes were on the market for just a few days before receiving multiple offers.

“The numbers say that there are 20% more listings on the market than this time last year and it is taking over a month to get an offer on a house and then roughly another month for that house to close. With just over 2 months of inventory in place, it looks like buyers spend more time shopping for the homes that are available. When a seller needs to sell their home quickly, the three components of real estate sales drive that pace: price, location, and condition. For the purposes of this report, let’s look at price and what might appear to be a sweet spot in a couple of price brackets. Digging in the data, it turns out there is massive variability. Many homes received an offer in March in as few as 2 or 3 days. Some homes didn’t receive an offer in more than 5 months. On the fringes, there are clearly factors other than price that determine how quickly or slowly these homes sold.

“In the middle of the data, however, I found some interesting results. It’s not necessarily conclusive but very interesting. Here’s an example: Homes selling between $550,000-$599,000 (below the median price) took roughly 45 days or so to get an offer. Homes selling between $600,000-$650,000 took just 19 days. This is not to say that the sellers who listed at $599,000 should have raised their price, but it may tell us something about buyer motivations across different price brackets. Buyers in the below median price point are going to be highly sensitive to interest rate fluctuations. Sellers in the below median price point may be less likely to concede large concessions to help a buyer reduce their interest rates since the seller likely needs as much of their net proceeds as possible to purchase their replacement property. Sellers and buyers in the higher price brackets may have a bit more flexibility on these two issues.

“All this is to say that we are in a balancing market and buyers and sellers are having to negotiate together more than any time in the last decade. Location, condition, timing, and urgency all play important roles in how buyers buy and how sellers sell. Pricing isn’t just based on what the historical data says – there are numerous variables at play when determining the ‘sweet spot’ for a house price,” said Fort Collins-area REALTOR® Chris Hardy.

GRAND COUNTY

“March in Grand County delivered weather extremes from snow to rain and wind and lots of sunshine in between. Winter Park Ski Resort is where the majority of our tourism is and that’s where we often see limited showings, due to properties being rented out as nightly rentals. But, as the end of the month approached, showings have increased and the number of active listings have increased as well.

Here is a breakdown based on inventory and pricing for the communities in Grand County for March year over year.

Single Family Homes

Active listings – Up 21%

Days on market until sold – up 140%

Units sold – Down 18%

Sales volume – Up 21%

Average sale price -$1,516,730 up 47%

Condos

Active listings – Up 33%

Days on market until sold – up 143%

Units sold – down 36%

Sales volume – down 24%

Average sale price – $705,342 up 17%

Townhomes

Active listings – Up 11%

Days on market until sold – up 23%

Units sold – up 133%

Sales volume – up 104%

Average sales price – $874,917 down 12%

“Looking at this breakdown of March 2025 vs March 2024, we can see that the number of listings has gone up, days on market to get a property sold is almost double the number of days it is taking to move them, but the values are continuing to appreciate. The only area where we are seeing a reduction in price sold, is with townhomes in Winter Park/ Fraser and Granby. This is due to the number of new construction of townhomes in general, causing the supply to go up and demand is down. The majority of the price decrease is happening in Granby, where average price of a townhome in 2024 was $900,000 and now the average price is $680,500.

“March has always been a transition month of heavy tourism leading to more sales, which shows in this data that March sales were up in single-family homes and townhomes, but down in sales volume for condos. That is probably due to inventory is up 41% in the condo market, with not very much new construction in the condo world,” said Grand County REALTOR® Monica Graves.

PUEBLO

“The month of March delivered some positive numbers across the Pueblo real estate market with new listings up 8.4%, 10.8% year to date and pending sales were up 3.9% compared to March 2024. Sold listings were down 12% from last March and are down 11.4% year to date. We’re seeing an increase in showings and active listings are up 18.5%. We’re sitting at a 4.8-month supply of homes across the market and watching interest rates falling a bit into the low 6% range. This is all good news for buyers.

“Our median price was up 2.1% from a year prior to $312,450 and the percent-of-list-price received was about the same as 2024 at 97.7%.

“We had 28 new building permits in March with 16 in Pueblo West. Agents are ready for a strong spring selling season,” said Pueblo-area REALTOR® David Anderson.

SAN LUIS VALLEY

“Here’s a quick look at the real estate market across the San Luis Valley as of March 2025. Whether you’re considering buying, selling, or just keeping tabs on the market, these trends offer a helpful snapshot of where things are headed.

In Alamosa County, new listings increased significantly—up 63.6% from last year—but sales dropped by a third. The median sales price fell 18.4% to $277,500, while homes are spending more time on the market, averaging 110 days. Despite the price dip, sellers are now receiving closer to their asking prices, with 97% of list price received year-to-date.

Rio Grande County remains one of the strongest markets in the region. Sales rose nearly 29% in March, and the median price jumped to $563,500—up an impressive 65.7%. Inventory is tightening, and homes are spending less time on the market. This continues to be a competitive seller’s market.

In Conejos County, high-value properties have pushed the median sales price to $250,000, more than double what it was a year ago. While the number of closed sales has dipped, sellers are seeing stronger offers and more listings entering the market, signaling rising interest and activity.

Costilla County saw a 70% increase in new listings and a 40% bump in closed sales year-to-date. However, prices are trending down with the median sales price falling 13.7% to $209,800. This, along with longer days on market, makes it an opportune time for buyers to enter.

Mineral County continues to show strength with limited inventory and rising prices. The median sales price is now at $390,000, up nearly 5%, and homes are selling for 96% of list price. With just 1.7 months of inventory available, demand is clearly outpacing supply.

Finally, Saguache County is seeing a healthy balance. New listings are up 80%, while median sales prices have increased modestly to $320,500. Homes are selling faster and with a higher percentage of list price received compared to last year.

“Each county is showing unique trends, but overall, we’re seeing a mix of price growth, low inventory, and increasing buyer activity across the region,” said San Luis Valley, REALTOR® Megan Bello.

SUMMIT, PARK, AND LAKE COUNTIES

“Picture the Summit and Park County real estate market like an all-you-can-eat mountain buffet. You walk in hoping prices have dropped like day-old fondue—but instead, everything’s getting fancier and the line is growing. Translation? Prices aren’t going down; they’re going up.

Let’s break it down like a waiter rattling off specials:

📈 Prices: Up 10.4% (median)

🏘️ Listings: Up a hearty 47%.

🛒 Sales: Up 11% compared to last March. So yes, people are shopping—and buying.

Affordable Entrées Now Available

Not everything is caviar and champagne. We’re seeing a big jump in affordable single-family homes hitting the market:

- Homes priced $300,000–$600,000: Year-over-year listings are up a sizzling 183%.

- Homes priced $1.5–$2 million: Listings are up 94%.

- Multi-family homes priced $2–$2.5 million: Up 100%.

Average Sale Price for Single-Family Homes (March 2025):

- 🏔 Summit County: $2,658,832 (33 sales, 11 more than last year)

- 🌲 Park County: $655,077 (13 sales, down 1)

- 🧊 Lake County: $495,000 (just 1 sale, down 1)

Average Multi-Family Home Prices:

- 🏢 Summit County: $868,799 (64 sales, 5 fewer than March ‘24)

What’s on the Market Right Now? Out of 600 active listings (48 more than last month), you can choose between:

- A $125,000 mobile home in Park County

- Or go full Gatsby with an $18 million luxury, 13,765-square-foot home being built on a ridge, overlooking Lake Dillon.

There are nine properties priced above $10 million, and nearly half the listings (48%) are over $1 million.

March’s 106 Residential Sales Say It All:

- Lowest sale: A $275,000 Silverthorne condo

- Highest sale: A Breckenridge single-family stunner for $8.7 million

And don’t think high-end buyers are sitting on the sidelines.

- 47% of sales were over $1 million

- 36% were cash deals—down 5% from February, but still strong enough to make you wonder if everyone’s carrying briefcases full of Benjamins.

So, is this a buyer or seller’s market? It’s like musical chairs with fewer chairs but fancier cushions. Inventory is up, demand’s still strong, and savvy buyers are moving fast.

Bottom Line: If you’re waiting for the market to cool like last night’s pizza—don’t hold your breath. The heat’s still on,” said Summit-area REALTOR® Dana Cottrell.

VAIL

“March is usually a significant month for the first quarter and was a bit stronger. However, unit sales were better than January and February but are still 16.3% negative versus 2024. Year to date, unit sales are down 24.3% versus the same period in 2024. Pending sales for the month are up 28%, which is the strongest performance in the year to date with the preceding months showing a decline versus 2024. Inventory of listings is up 23.5% and slowly growing to the levels experienced pre Covid. Based upon today’s rate of sale, the inventory has reached 5.9 months which is effectively what is considered a stable supply by historic standards.

“Following the trend of the past year, the dollar performance is positive and driven by market share of the upper price niches becoming a dominant unit share. Based on the inventory by price niche, we would expect the trend to continue. Macroeconomic factors will be the catalyst for any change in the trend. Mortgage rates are still below the recent peaks and the volatility of the investment markets may entice more investors to bring real estate into their portfolio.

“We now enter our shoulder season and await the summer season to start in June and we hope the macro economy will have settled into a growth pattern,” said Vail-area REALTOR® Mike Budd.

The Colorado Association of REALTORS® Monthly Market Statistical Reports are prepared by Showing Time, a leading showing software and market stats service provider to the residential real estate industry and are based upon data provided by Multiple Listing Services (MLS) in Colorado. The March 2025 reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. CAR’s Housing Affordability Index, a measure of how affordable a region’s housing is to its consumers, is based on interest rates, median sales prices and median income by county.

The complete reports cited in this press release, as well as county reports are available online at: https://www.coloradorealtors.com/market-trends/

###

CAR/SHOWING TIME RESEARCH METHODOLOGY

The Colorado Association of REALTORS® (CAR) Monthly Market Statistical Reports are prepared by Showing Time, a Minneapolis-based real estate technology company, and are based on data provided by Multiple Listing Services (MLS) in Colorado. These reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. Showing Time uses its extensive resources and experience to scrub and validate the data before producing these reports.

The benefits of using MLS data (rather than Assessor Data or other sources) are:

Accuracy and Timeliness – MLS data are managed and monitored carefully.

Richness – MLS data can be segmented

Comprehensiveness – No sampling is involved; all transactions are included.

Oversight and Governance – MLS providers are accountable for the integrity of their systems.

Trends and changes are reliable due to the large number of records used in each report.

Late entries and status changes are accounted for as the historic record is updated each quarter. The Colorado Association of REALTORS® is the state’s largest real estate trade association representing over 25,000 members statewide. The association supports private property rights, equal housing opportunities and is the “Voice of Real Estate” in Colorado. For more information, visit https://www.coloradorealtors.com