Housing markets finding some balance as full spring season begins

Steady sales, stable pricing and rising inventory signal a more buyer-friendly, negotiation-driven environment despite ongoing economic uncertainty

ENGLEWOOD, CO – Housing markets across the seven-county Denver metro and statewide showed signs of balance and rhythm in the first quarter of 2026 including modest gains in pending and closed sales, stable median home pricing, and an uptick in inventory creating a more buyer friendly, negotiation-driven environment heading into the full spring season, according to the latest Market Trends Housing Report from the Colorado Association of REALTORS® (CAR).

SEVEN COUNTY DENVER METRO

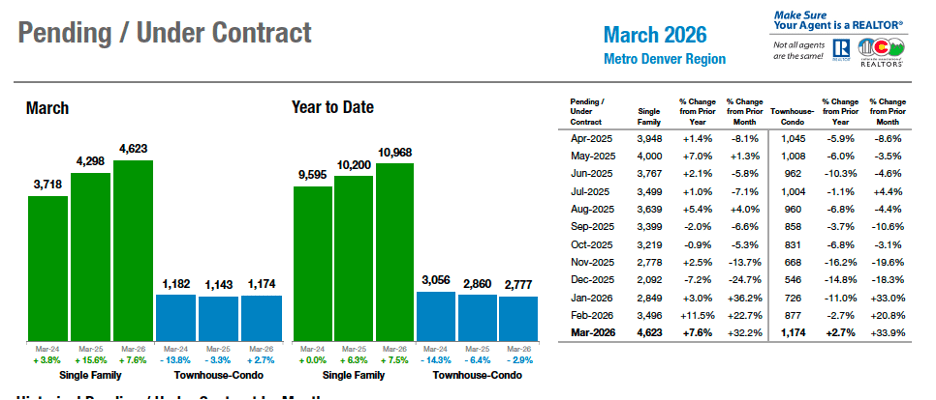

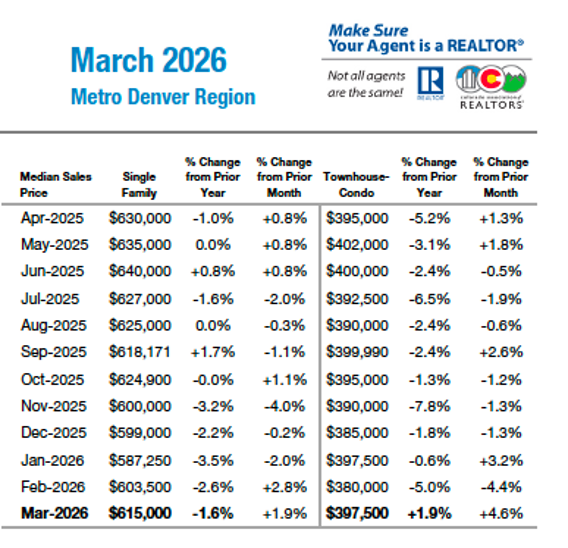

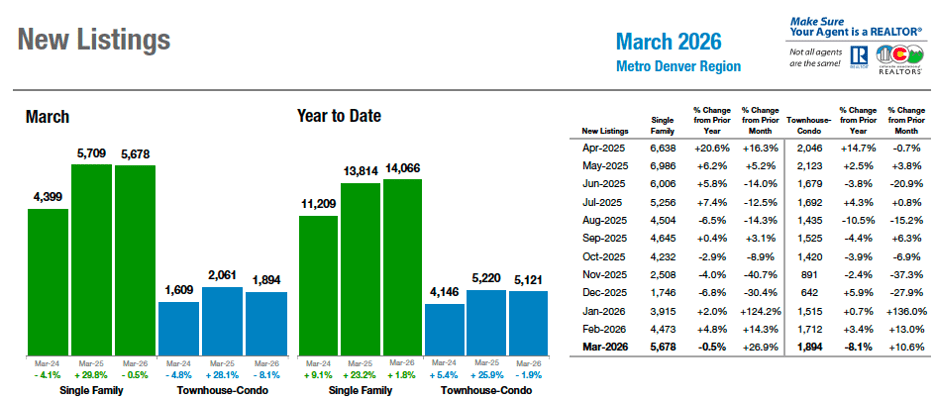

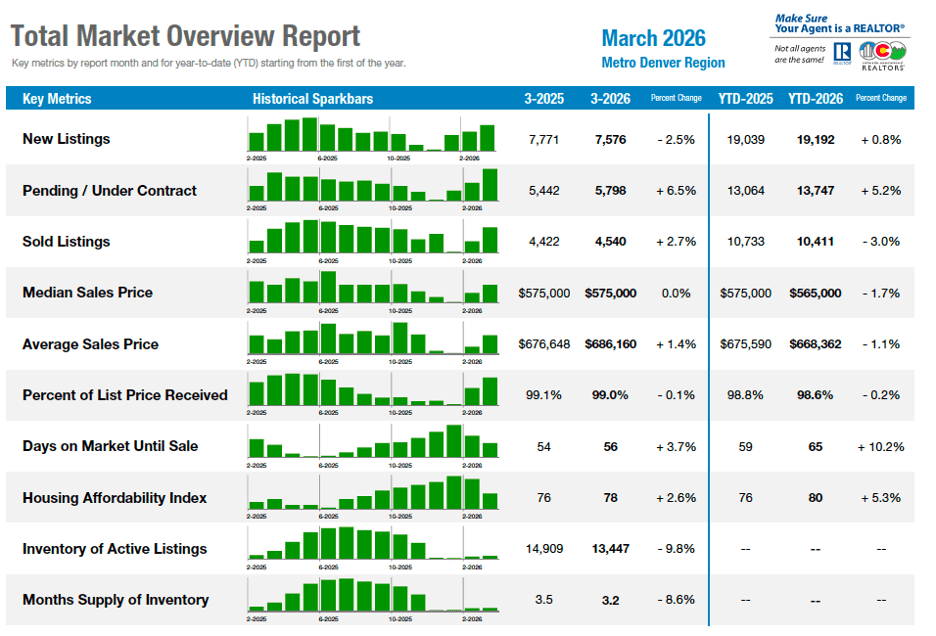

In the seven-county Denver metro region, first quarter statistics revealed a market that has found its rhythm, according to Denver-area REALTOR® Cooper Thayer. March posted 5,798 pending contracts, up 6.5% year-over-year, alongside 4,540 closed sales (+2.7%) and 7,576 new listings (-2.5%). The median sale price across the Denver metro held flat at $575,000 and in line with Q1 results from 2023, 2024, and 2025.

PENDING/UNDER CONTRACT – SEVEN COUNTY DENVER METRO AREA

Average days on market ticked up to 56, active inventory sits at 13,447 listings, and months of supply dropped to 3.2. Pending contracts on single-family homes rose 7.6%, sold listings climbed 5.2%, and months of supply tightened to 2.7 with a median sale price of $615,000.

MEDIAN SALES PRICE – SEVEN COUNTY DENVER METRO AREA SINGLE-FAMILY

The attached home market continues to have its challenges with average days on market increasing nearly 26% to 68 days and 5.1 months of supply keeping condos and townhomes in buyer-favorable conditions thanks mostly to high HOA dues and insurance costs impacting demand.

NEW LISTINGS – SEVEN COUNTY DENVER METRO AREA

“Inventory has expanded across the foothills as more sellers enter the market ahead of the spring season, providing buyers with more options and contributing to a more balanced negotiating environment,” said Evergreen-area REALTOR® Julia Purrington Paluck. “As the spring market progresses, the key question will be whether increased buyer engagement translates into a higher pace of closed sales. If mortgage rates stabilize near current levels, the foothills market may see improved conversion from listing through contract to closing. If rates rise again, the market is likely to remain active but will move forward at a more measured and negotiation-driven pace.

In addition to assessing where things have been, REALTORS® are keeping their focus on what lies ahead as well.

“The variable that matters most heading into Q2 is one the market cannot control: geopolitical uncertainty and its effect on mortgage rates,” added Thayer. “If geopolitical disruption pushes rates meaningfully higher, expect days on market to stretch further and pricing to soften. Either way, the homes that are priced to the market and presented well are still trading. The rest are sitting a little longer.”

Total Market Overview – Seven-County Denver Metro

STATEWIDE SUMMARY:

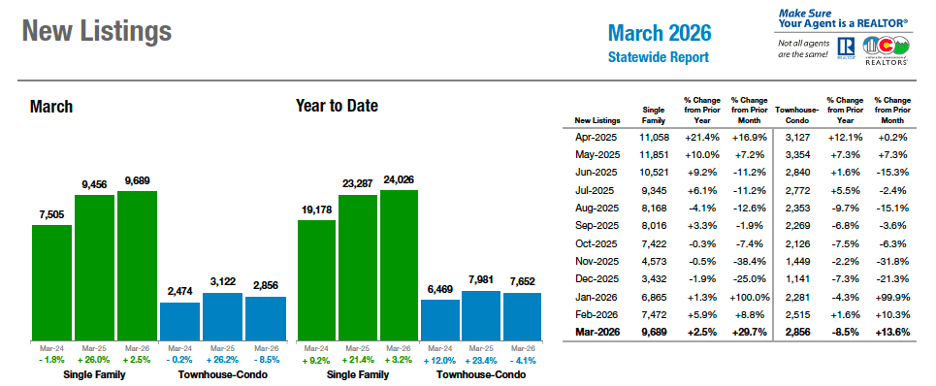

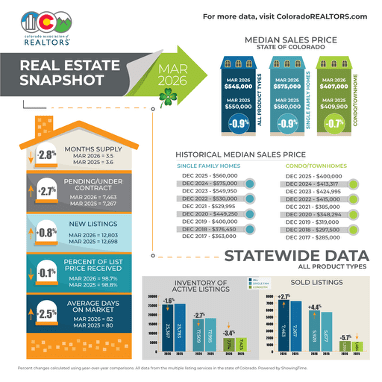

Looking to the full statewide market performance, there were 12,803 new listings in March with 9,541 pending sales, up 7.2% from a year prior, as well as 7,463 sold listings, up 2.7% from March 2025.

The median sale price across the state dipped slightly (0.9%) from a year ago to $545,000.

“Day-to-day activity may feel busy, but that is likely because the year started off very slow. Overall, this spring market is still behind where it usually is and has a long way to go to match the stronger spring markets of the past. The war in Iran and higher interest rates may be playing a role in buyer demand and overall consumer confidence,” said Boulder/Broomfield-area REALTOR® Kelly Moye.

NEW LISTINGS – STATEWIDE

Statewide, the average days on market hit 70, up from 66 a year ago. Active inventory sits at 25,367, down 1.6% from March 2025 and pushing the months supply of inventory down 2.8% from a year ago to 3.5 months.

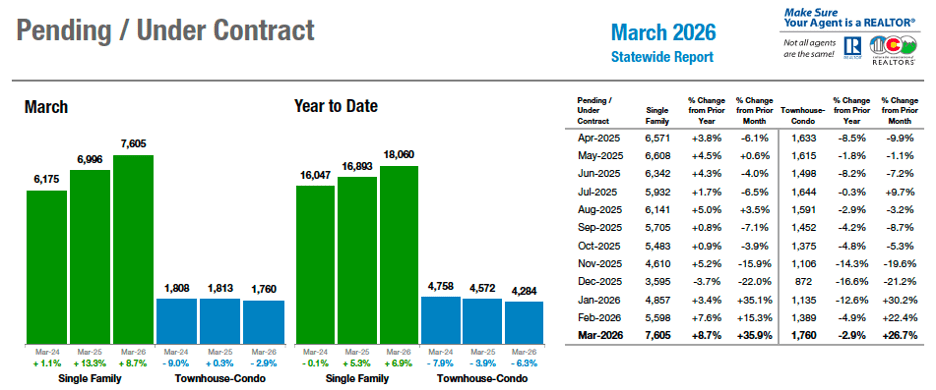

PENDING/UNDER CONTRACT – STATEWIDE

Similar to the seven-county Denver metro area, the attached home market faces HOA and insurance cost challenges that contribute to an increase in average days on market – up more than 15% to 76 days – and 5.1 months of supply delivering buyer-leaning conditions in many markets across the state.

Total Market Overview – Statewide

Colorado Housing Markets – March Snapshot

Based on analysis from REALTORS® working in markets across the state

(for a more in-depth analysis by market, see full content in report):

Aurora – Aurora and Centennial housing markets are off to a slower-than-expected spring, with inventory down by as much as 45% in some areas compared to last year. Prices have declined 1% to 8%, sales have decreased and homes are taking longer to sell. Economic concerns, including rising cost of living, are weighing on buyers. With median prices ranging from about $510,000 to $669,700, sellers should expect roughly 60 days on market as they await a potential seasonal uptick in activity.

Boulder and Broomfield counties – Boulder and Broomfield housing markets are off to a slower-than-usual spring, with limited new listings and uneven activity. While Boulder has seen modest gains in sales and prices, some homes are selling quickly while others linger on the market. The condo and townhome segment is struggling due to higher HOA and insurance costs. Broomfield prices remain flat or down and homes are taking longer to sell, reflecting cautious buyers amid economic uncertainty and higher interest rates.

Colorado Springs – The Pikes Peak market showed signs of stagnation in March, with slight declines in sales and prices and a notable increase in inventory. Buyer demand remains uneven, with some homes seeing strong interest while others sit with little activity. Condo and townhome values have dropped significantly, and broader economic uncertainty driven by rising interest rates and global instability is hurting confidence. The market is expected to remain slow and price-sensitive, with longer selling times and increased pressure on sellers to price competitively.

Crested Butte/Gunnison – Crested Butte and Gunnison markets are tracking closely with 2025 trends but show early signs of a potential shift heading into summer. Overall sales are down, though dollar volume has declined less sharply and inventory is rising. Crested Butte remains relatively stable, with gains in the condo and townhome segment, while Gunnison lags last year despite increased listings and contracts. With more inventory expected and seasonal momentum building, the region is preparing for a potentially stronger summer market.

Denver Metro – The market continues to demonstrate stability and consistency with gains in sales activity and flat pricing mirroring trends from the past three years. While the market is moving at a slower, more deliberate pace, overall transaction volume remains steady. Single-family homes are driving performance, while condos and townhomes face softer demand due to rising costs. Looking ahead, mortgage rate volatility tied to geopolitical uncertainty will be the key factor influencing buyer activity and market momentum.

Durango/LaPlata County – The Durango-area market saw strong momentum in March with a sales surge driven by increased inventory and modest price growth. Single-family demand has largely kept pace with supply while the condo and townhome segment is rebounding after a slow 2025, aided by more affordable pricing. Despite rising inventory across price points, high costs and interest rates may temper activity, though seasonal demand and expanding options could continue to support buyer engagement heading into summer.

Evergreen/Foothills – The foothills housing market is experiencing increased activity heading into spring with more showings, listings and contracts, but a slower pace of closings reflecting a more deliberate, negotiation-driven environment. Rising inventory is giving buyers more leverage, keeping prices relatively stable. Mortgage rates continue to shape behavior, with future market momentum depending largely on rate stability and improved conversion from contracts to closings.

Fort Collins – The Fort Collins housing market remains highly unpredictable with uneven activity across price points. While inventory has increased and some segments, particularly move-up homes, are seeing strong demand and multiple offers, other areas are experiencing limited buyer interest and longer selling times. Prices have remained relatively flat or declined slightly and the condo market is struggling despite increased sales. Overall, mixed conditions and affordability challenges are expected to persist, creating continued volatility in the months ahead.

Grand County – The Grand County housing market is softening but remains stable with rising inventory and slight price declines creating a more balanced environment. Buyer activity has slowed as purchasers become more deliberate. Demand, especially for well-priced, move-in-ready homes, remains steady. Resort-driven lifestyle continues to support long-term interest, even as broader market conditions cool. With strong rental demand and increased choices, the market is neither favoring buyers nor sellers, but instead shifting toward a more measured, equilibrium state.

Mesa County – Inventory continues to grow across Mesa County in March. New listings were up more than 14% year over year but pending and sold sales were both in the negative, over 6%. Prices are holding with the median at $410,000 and average sales price at $470,965. We have more listings over $500,000 than we do under and that limits choices for many of our buyers. Condos and townhomes are offering some affordability however, HOA dues are a consideration when qualifying for financing.

Pagosa Springs – Pagosa Springs is offering increased opportunities for buyers with rising inventory, especially at entry-level and high-end price points. Sales have surged alongside new listings. Although, homes are taking longer to sell and median prices have declined. Higher-priced properties are moving more slowly as buyers grow more selective while lower-priced homes are seeing strong demand. Despite affordability challenges tied to interest rates, strong selection and seasonal momentum could support continued activity heading into summer.

Steamboat Springs/Routt County – The Steamboat Springs market showed mixed signals in the first quarter with fluctuating monthly sales, fewer new listings and declining single-family prices despite steady overall activity. While March closings slowed, pending contracts suggest potential near-term gains. The condo and townhome segment remains stable with rising prices, even as inventory grows. Surrounding areas are seeing modest activity and limited supply, pointing to a market that remains competitive but is gradually stabilizing as it heads into the second quarter.

Summit, Lake and Park counties – The Summit and Park County housing markets showed mixed performance in March with softer demand and declining prices in the single-family segment, while multi-family properties demonstrated greater resilience with stable or rising values. Limited snowfall and reduced tourism contributed to slower activity, though inventory remains diverse and heavily weighted toward higher price points. Despite recent softness, strong pending activity, and a high share of luxury and cash transactions point to a potentially more active spring and summer season ahead.

Telluride – The Telluride market continues to be driven by high-end buyers with strong luxury sales activity in Mountain Village and Telluride despite broader economic uncertainty and rising interest rates. Wealthy buyers remain largely insensitive to price, focusing instead on lifestyle fit. While overall transactions remain below long-term averages, rising dollar volume and fewer deals suggest a market that is stabilizing and increasingly concentrated in the luxury segment.

Vail – The Vail housing market is facing heightened uncertainty following a challenging winter marked by low snowfall and reduced tourism with potential ripple effects on the local economy and housing demand. While sales activity has shown modest gains, prices have softened and inventory has increased. Market performance remains relatively stable overall but, trends between property types and broader economic pressures make the outlook for the spring and summer seasons difficult to predict.

Weld County – The Weld County market is stabilizing in early 2026 with steady new listings, slightly reduced inventory, and modest declines in sales. Homes are taking longer to sell while prices have leveled off after years of growth. Despite slight price dips, sellers continue to receive strong offers near list price. The condo and townhome segment is experiencing a more noticeable slowdown, though pricing remains relatively stable, reflecting a balanced but cooling market.

Taking a more in-depth look at some of the state’s local market data and conditions, the Colorado Association of REALTORS® Market Trends spokespersons provided the following assessments:

AURORA

“Hope and tradition would have the Aurora/Centennial markets in a robust spring rush. Sadly, the numbers show otherwise. For all Aurora zip codes and most Centennial zip codes, the listing inventory is down from this time last year. We expected to see a significant increase in homes for sale across the market, but it simply isn’t so. Inventory is down over this time last year and in some cases as much as 45% lower than this time last year. Pricing is also down anywhere from 1% to 8% depending on the zip code. It follows that the number of sold properties are down from March of last year while average days on market is up from last this time last year.

“Today’s buyers are concerned about gas prices, jobs, and the overall cost of living and feeding a family right now. The median home price in Aurora is $510,000, in Centennial, $669,700, in Arapahoe County the median price is $580,000, and in Adams County the median price is $519,900. Sellers should plan for at least 60 days on market if the home is priced well and shows well. Hopefully, the next few weeks or months will bring much needed rain and a spring home-buying rush,” said Aurora REALTOR® Sunny Banka.

BOULDER/BROOMFIELD COUNTIES

“The spring real estate market in Boulder and Broomfield counties is off to a slower start than usual this year. Spring is normally a busy time when many homeowners list their properties, but that has not really happened so far. In Boulder County, new listings are down 5%. In Broomfield County, listings are only slightly higher, up about 6%.

“Even with fewer homes for sale, there has been some steady buyer activity in Boulder. Sales are up 4%, and prices have gone up a little, rising 3% since January and 7% compared to last year. At the same time, the market feels uneven. Some homes are selling quickly and even getting multiple offers, while others are sitting on the market much longer, taking around 80 days to sell.

“The condo and townhome market in Boulder is having a tougher time. There are 10% fewer listings, and prices have dropped about 4%. Higher HOA fees, mostly due to rising insurance costs, seem to be making buyers more cautious in this part of the market.

“In Broomfield County, prices are not showing much movement. They have stayed flat since the start of the year and are down 7% compared to last year. Homes are also taking longer to sell. Single-family homes are averaging about 66 days on the market, while condos and townhomes are taking close to 100 days to sell, which is one of the longest times seen in years.

“Day-to-day activity may feel busy, but that is likely because the year started off very slow. Overall, this spring market is still behind where it usually is and has a long way to go to match the stronger spring markets of the past. The war in Iran and higher interest rates may be playing a role in buyer demand and overall consumer confidence,” said Boulder/Broomfield-area REALTOR® Kelly Moye.

COLORADO SPRINGS

“The Pikes Peak region had an interesting March, and maybe a little worrisome. What continued to feel like a market shift ended up being flat. Sold listings were down 0.8% for a one-year change, and the median price pulled back 1.8%, and then we added 9.4% more listings to the mix. While we are seeing some homes get great activity, across the market many agents also saw very few showings on their homes. The growing inventory along with a lack of buyer demand continues to soften prices and yet, buyers are still not comfortable with buying and jumping in the market. The townhome and condo market is taking the brunt of the decline, seeing a 15.1% drop in values on median price from a year ago.

“National news that matters to the economy is the war in Iran which has created fluctuations in interest rates and additional uncertainty. As I write this, we are on a two-week pause. We have seen more hedge funds limit withdrawals. Jamie Dimon with Chase Bank is now stating the private equity market is worse than most believe. When he talks, we should listen. Unemployment remains low, but at street level most people are apprehensive about the economy. Gas prices broke records which also put downward pressure on stocks, metals, and buyer sentiment.

“This year is going to be touch and go. I believe the spring rush is short lived and a year of grinding is in front of us. The private equity market is in trouble; we don’t know how bad it is yet. Auto loans are going delinquent at a rapid pace and homes typically follow. The default industry for homes is seeing an increase. By mid-summer we are likely going to see days on market increase and motivated sellers will begin to drop prices. Sellers should price right on day one. Overpricing listings is costing sellers time and money as days on market increase. Buyers will have a great selection of homes to choose from if they also find affordability,” said Colorado Springs-area REALTOR® Patrick Muldoon.

CRESTED BUTTE/GUNNISON

“The Crested Butte and Gunnison real estate markets continue to parallel 2025 through the first quarter of the year however, there are signs that we may have a shift heading into the summer months.

“Overall, the number of sales in the Gunnison Crested Butte Association of REALTORS® market area is down 14%, but the dollar volume is only down 5%. When you look at residential sales specifically, the difference in the number of sales and the dollar volume is negligible year over year, but we do have a 7% increase in inventory.

“The Crested Butte area market had exactly the same number of sales in the first quarter of 2026 as we saw in 2025 with dollar volume down a bit (3%). The number of single-family home sales was down 25% (12 vs. 16), but that only resulted in a decline of 2% in dollar volume. Looking to the condos/townhomes market, we had 35% more solds this year (23 vs. 17) with 22% more dollar volume in 2026 than in 2025. There are 24% more residential properties for sale this year than last and I anticipate that number will go up as we head into the summer selling season.

“The Gunnison market continues to lag behind last year but shows signs of picking up. Gunnison is ahead of 2025 in both active listings and properties under contract compared to this time last year. A particularly busy spring will hopefully be the start of a great 2026. So far, we have only 23 sales vs. 38 last year – down almost 40% with dollar volume down 32%. Single-family home sales have been a stronger point with only one less sale than last year and dollar volume down just 11%.

“The valley is watching the snow melt and preparing for summer. There are already trails open and things are greener than usual in mid-April. Both ends of the valley are anticipating more inventory and more visitors to help create a busy summer real estate season,” said Crested Butte-area REALTOR® Molly Eldridge.

DENVER METRO (Seven County)

“The first quarter of 2026 reinforced what should now be an undeniable pattern: this market has found its rhythm. March posted 5,798 pending contracts, up 6.5% year-over-year, alongside 4,540 closed sales (+2.7%) and 7,576 new listings (-2.5%). The median sale price across the Denver metro held flat at $575,000. These numbers land in a remarkably similar range to Q1 of 2023, 2024, and 2025. The annual cycle repeats with near-mechanical consistency. What distinguishes 2026 is pace, not direction. Average days on market ticked up to 56, active inventory sits at 13,447 listings, and months of supply dropped to 3.2. The market is operating at a more deliberate speed, but the volume of transactions and the dollars flowing through closings have been strikingly stable across the last three annual cycles.

“Single-family homes are doing the heavy lifting. Pending contracts rose 7.6%, sold listings climbed 5.2%, and months of supply tightened to 2.7 with a median sale price of $615,000. The attached segment remains the pressure point, with days on market stretching to 68, a nearly 26% increase, and 5.1 months of supply keeping condos and townhomes firmly in buyer-favorable territory. HOA dues and insurance costs continue to weigh on demand in that segment, and sellers need to price accordingly.

“The variable that matters most heading into Q2 is one the market cannot control: geopolitical uncertainty and its effect on mortgage rates. We have watched significant rate volatility over the past several weeks, and that kind of instability can shake confidence. But so far, buyers are not flinching. Showing volume in March was identical to March 2025, one of the most direct real-time measures of buyer engagement we have. If rates stabilize or drift lower, this market has the underlying demand to accelerate. If geopolitical disruption pushes rates meaningfully higher, expect days on market to stretch further and pricing to soften. Either way, the homes that are priced to the market and presented well are still trading. The rest are sitting a little longer,” said Denver County-area REALTOR® Cooper Thayer.

DENVER APARTMENT MARKET UPDATE

“The Denver Apartment Market is struggling for a variety of reasons in 2026. My recent conversation with Scott Rathbun from Apartment Insights and Apartment Appraisers & Consultants helps tell the full story.

“After a record delivery of new apartment units, Denver has officially overbuilt the seven-county metro area. Denver Metro issued the following permits for multifamily units: 21,406 in 2021, 19,085 in 2022, 10,549 in 2023, 10,255 in 2024, and 12,021 in 2025. This type of construction hasn’t been seen in the Denver-metro area since the 1970s and is double the annual permits of the post-recession, pre-Covid economic recovery (2012-2020). Permits aren’t pulled until a developer is ready to break ground, and now it takes 30-months on average to build an apartment community from permit to completion.

“Looking closer at those permitted units, in 2024 (30 months after the 2021 spike of permits) Denver delivered 23,000 newly constructed apartment units. Historically, Denver metro delivers 10,000-13,000 units/year. In 2025, Denver delivered 14,000 new apartment units – except for the prior year (2024), that would have been an all-time record year of construction. The prediction by year-end 2026 is 11,000 completed units.

“Stabilized vacancy increased to 7.6% (from 6.2% just a year ago) and all property vacancy (which includes property in lease-up) is now 11.17% (from 6.9% in 2022 and 2021 respectively). The last time that Denver experienced a 7%-plus vacancy rate was in 2019. Vacancy is highest in Denver County and Arapahoe County (tied for 8.2%), followed by Jefferson County (7.0%), Douglas County (6.9%), Adams County (6.7%), and was the lowest in Boulder/Broomfield at 6.7% vacancy. Denver County and Arapahoe County experienced the highest vacancy, because those counties have a higher density of multifamily units. At the end of 2025, the Denver-metro area had more than 30,000 total vacant apartments.

“Now that Denver is experiencing above average vacancy due to record construction, developers try to buy occupancy by offering concessions. Denver is experiencing the highest amount of concessions in the past 19 years (9.5% average for the entire metro area which represents an average of 4-5 weeks free rent for every property in the metro area — some developers are offering 12 weeks free for a 15-month lease).

“Gross rents are down 4.7% year-over-year and average $1,777 across the metro area; effective/net rents, with concessions factored in, average $1,608. Net rents are down 7.2% quarter-over-quarter and down 9.8% year-over-year. Denver has experienced negative year-over-year rent growth for nearly two years (seven consecutive quarters). This is the largest rental decline in 21 years.

Average Rents by County:

$1,620/month: Adams (vs. $1,705 a year ago)

$1,638/month: Arapahoe (vs. $1,746 a year ago)

$1,858/month: Boulder/Broomfield (vs. $1,959 a year ago)

$1,784/month: Denver (vs. $1,867 a year ago)

$1,950/month: Douglas (vs. $2,013 a year ago)

$1,776/month: Jefferson (vs. $1,864 a year ago)

$1,754/month: Denver Metro Area Average (vs. $1,842 a year ago)

“What’s next for Denver metro apartment construction? The forecast is that we will begin to absorb more vacant apartments than we complete newly constructed units which will cause vacancy to decrease. Scott Rathbun is predicting that the overall vacancy rate will decrease from its current 7.6% to 6.9% at the end of 2026, 6.2% at the end of 2027, and 5.4%* at the end of 2028.

“A 5% vacancy is considered stable and then rents begin to increase again which is generally when new construction permits begin to increase due to favorable market conditions,” said Denver-area Multi-Family REALTOR® Kyle Malnati.

DURANGO/LA PLATA COUNTY

“March was a busy month for closings. Sold listings increased 34.8% overall compared to March 2025, encouraged by the vast amount of inventory coming on market. There are 23% more active listings than in March 2025 and the median price has ticked up 1.7% over March 2025.

“Single-family buyers in the county have mostly kept up with supply, with a 23% increase in new listings over March 2025 (14% YTD over 2025 YTD) and a 25% increase in sales compared to March 2025 (10.5% YTD over 2025 YTD).

“Townhomes/condos are continuing to pick up in number of sales after a dismal 2025, with a 70% increase in sold listings over March 2025 and a 49% increase year to date over the same period in 2025. This segment is still seeing a growth in total inventory of homes on the market, which will hopefully reverse in 2026. It’s possible that the increase in cost of insurance, and therefore HOA fees, kept buyers away in 2025, but the continuing rise of single-family home prices has increased the share of sales this segment is now seeing.

“Durango in town single-family homes haven’t had more than a handful of homes for sale at any time in years, and the median price here has pushed to $940,000 year to date. Townhomes/condos are having their day with a 75% increase in sales year to date, helped by a lower price point of just $400,000 in March. For many buyers wanting to live near Durango, the choice has become either purchasing a condo closer to our engaging downtown or adapting to a rural lifestyle further from city limits.

“For those choosing the drive into rural Durango, single-family homes still command high prices, but one can purchase a much larger, newer home for the same cost-the median is $876,000 in March. Further still from rural Durango is the City of Bayfield, where home sales in March had a median of $481,250, a much more affordable price than in Durango.

“The housing market near Purgatory Resort had an excellent end to a very limited ski season, as experienced in most of Colorado. Four single-family homes sold in March compared to none sold year to date over the same period in 2025. Townhome/condo sales also increased 66.7% for the 2026 season, making for sound past decisions by developers currently building in the area who bet the market would remain strong.

“With rates currently around 6.5%, we expect market momentum to slow down. Countering this will be the excitement buyers often feel this time of year when inventory is popping and the summer selling season is edging closer. Hopefully, buyers will decide to make a move still, even if their choices will be different from what they would make without the higher rates,” said Durango-area REALTOR® Heather Erb.

EVERGREEN/MOUNTAIN METRO

“The foothills market entered spring 2026 with a noticeable increase in activity, though the pace of completed transactions continues to lag buyer engagement. Showings, new listings and homes going under contract have all increased across the region, reinforcing the sense among local agents that the market has become more active. At the same time, closings have not accelerated at the same pace, highlighting a market where transactions require more negotiation and time to reach completion.

“Across the foothills, listings are attracting increased showing activity and buyers are actively writing offers. At the same time, the pace of completed transactions has not accelerated at the same rate. This disconnect is one of the defining characteristics of the current market.

“One of the most telling indicators is the widening gap between median and average days on market. Median timelines suggest that well-priced homes are still selling within a reasonable timeframe. However, the rising average days on market, now at its highest level since 2015, shows that a growing portion of listings are sitting significantly longer. This pattern reflects a market where demand remains present but increasingly selective.

“Inventory has expanded across the foothills as more sellers enter the market ahead of the spring season, providing buyers with more options and contributing to a more balanced negotiating environment. Average days on market increased roughly 7% year over year, while list-to-sale price ratios have softened slightly, reinforcing that buyers are exercising greater leverage and negotiating more actively.

“Evergreen and Conifer continue to serve as key indicators for the region. In Evergreen, the median price for detached single-family homes is approximately $933,000, with the average price just above $1.1 million. While pricing has remained relatively stable, increased inventory and longer marketing times are contributing to more varied outcomes depending on pricing strategy and property condition.

Mortgage rates remain the most significant factor shaping market behavior. After moving just under 6% earlier this year, rates have stabilized in the low-to-mid six percent range. While this has supported renewed buyer activity, affordability continues to influence decision-making. Buyers are participating, but doing so more deliberately, often requiring stronger alignment on pricing and terms before proceeding to closing.

“As the spring market progresses, the key question will be whether increased buyer engagement translates into a higher pace of closed sales. If mortgage rates stabilize near current levels, the foothills market may see improved conversion from listing through contract to closing. If rates rise again, the market is likely to remain active but will move forward at a more measured and negotiation-driven pace.

For now, the foothills market is best described as active, stable, and increasingly selective,” said Evergreen-area REALTOR® Julia Purrington Paluck.

FORT COLLINS

“When chatting with other Fort Collins REALTORS®, the phrase ‘weird market’ seems to be the most common description in the last year or so. The March 2026 real estate market has certainly earned that moniker. And while the term ‘weird’ is subjective, let me put some tangible tags on this market. Only in a weird market can you have multiple, above-list-price offers in a specific price point, only to have tumbleweeds outnumber showings in another. Only in a weird market can you have spiking March inventory in one product type, just to have it retreat in another. And only in a weird market can you have less inventory with more demand and still have prices retreat. Buckle up for not just a weird month in the market, but for a potentially peculiar, prolonged period.

“The single-family detached market saw massive gains in new inventory, up 21.2% to 349 listings, while overall listings remained 9.7% higher than March 2025. This helped dilute the buyer pool a bit and spread the demand out. Anecdotally, the single-family move-up market ($650,000-$900,000) seems to be on fire as folks who may have purchased within the last decade are outgrowing or growing tired of their current setup and needing bigger space or better locations. Multiple, above-list-price offers are common and frustrating for many buyers, as there are too few turnkey options for them to choose from.

“Median value remained essentially level, down 2.1% from March 2025 to $595,000. Outside of the move-up market, it’s a different story. Lower-end properties are plentiful, but buyers are finding it difficult to qualify with rates at current levels. On the high-end market, buyers are more likely to be selective and less motivated to make a move unless the stars align – which is difficult in a ‘weird market.’ Because of the diluted demand, average days on market is up 18.2% compared to March 2025 and is up nearly 12% year over year.

“The attached condo and townhome market had a rough March. The magic number is 22% — as compared to March 2025, new listings are down 22%, total active listings are down 22% and monthly supply is down 22%. Luckily, there is still buyer demand in the condo/townhome market, simply because it is a more affordable product. However, even with a 23.7% increase in attached sales, median value dropped 3.5% to $414,500. Stable demand plus reduced inventory should push prices up, but only in a weird market would they come down, as they did. Inventory should shoot up in April if the attached market has any shot at firming up in 2026.

“March was meant to be a big test for the stability of the market, and I’d probably give it ‘C’ grade. Passing, but barely. The biggest tailwind in the market is that affordability is continuing to improve, both through marginally better interest rates and slightly lower median values. Rates or prices will not improve substantially enough for that to truly impact the market, so my prediction is that we will continue to see odd, unusual, abnormal, bizarre and otherwise very weird months ahead in this market,” said Fort Collins-area REALTOR® Jared Reimer.

GRAND COUNTY

“This first quarter of 2026 can be explained like the mountains, they don’t rush, they don’t spike, and they don’t crash, but they do shift. If you have spent any time at the Winter Park ski resort, you can see the real estate market behaves a lot like the snow pack this year, especially March 2026, it was minimal. Mary Jane closed early for the first time in many years as tourism and tickets at the counters fell.

“There has been a slowdown but not a crash, just a softening. The tone in March has shifted, new listings increased 9.8% in single-family homes but decreased 7.7% in townhome-condos. Inventory increased 9.9% in single-family homes and 3.6% in townhome-condos. Prices are beginning to level off or pull back slightly with the median sales price down 3.8% on single family to $1.125 million and a staunching 15.8% down to $537,000 on attached properties. But in March, we see that days on market decreased 12.7%, which may be a silver lining for the coming of spring and summer.

“All we know is that buyers are not rushing, they are thinking, and that is where Winter Park/Fraser, Granby, and Grand Lake sit today, not hot, not cold, but balanced. Inventory has grown, giving buyers more choices, negotiation is back on the table, rental demand is still strong (~$2,600/month average), supporting investor confidence, and in Grand County we are calling it a stable market with slight appreciation but no clear advantage to buyers or sellers.

“We have the mountain effect which, in my opinion will help our market when it comes to sales. Resort mountain areas like Winter Park and Grand Lake don’t follow the same rules as a city. The mountain markets are driven by something deeper: Lifestyle. People don’t buy here just for ROI, they buy for ski mornings, summer trails, family legacy, and a place to get away from the city life. That’s why, even as the broader market cools, places like Winter Park, Granby, and Grand Lake will still see growth and continued demand for turnkey, lifestyle-driven properties. The serious buyers will show up.

The new reality from this past March is homes that are dialed in—priced right, staged right, marketed right—still move. The rest, sit,” said Grand County-area REALTOR® Monica Graves.

MESA COUNTY

“Inventory continues to grow across Mesa County in March. New listings were up more than 14% year over year but pending and sold sales were both in the negative, over 6%. Prices are holding with the median at $410,000 and average sales price at $470,965. We have more listings over $500,000 than we do under and that limits choices for many of our buyers. Condos and townhomes are offering some affordability however, HOA dues are a consideration when qualifying for financing,” said Mesa County REALTOR® Ann Hayes.

PAGOSA SPRINGS

“The first three months of 2026 had promising inventory for buyers in the Pagosa Springs market. Year-to-date new listings were up 16.8% creating a 6.5-month supply of homes and we have an average 160 days on market. Compared to last month, sales and listings were on an upward swing. Sales were up 56.3% at 25 homes (compared to 16 homes in February 2025) and listings increased 11.3% indicating homes entering the market earlier than last year. Buyers seeking homes priced above the average and median sales prices especially have an abundance of home inventory.

- Median Sales Price down 8.5% at $583,500 ($637,527 in 2025)

- Average Sales Price up 0.4% at $705,029 ($702,235 in 2025)

- Days On Market up 12% at 160 (142 in 2025) Months of Supply: 6.5

“March showed some higher inventory gains in homes priced under $499,000 (typically condo and manufactured homes). Entry level local and second-home buyers pounced on those inventory gains. The biggest inventory gains were homes priced at $1 million and more. However, those buyers are more selective and hesitant because they have the most selection of home inventory. Currently, there are 236 homes for sale in Pagosa Springs:

- ACTIVE HOMES UNDER $499,999 (Mostly Condo | Manufactured Home):69

- ACTIVE HOMES $500,000-699,999 (Median-Average Price):55

- ACTIVE HOMES $700,000-$999,999: 55

- ACTIVE HOMES $1 million plus: 57 (39 homes $1,000,000-$1,999,999)

“With consideration, there are already 57 homes on the market priced at $1 million and higher and only eight have sold in the first three months with a handful under contract. This higher price point is sluggish for sales. In 2025, 60 homes sold at $1 million plus (less than 2024).

“Historically, the summer season attracts more buyers, especially high-end buyers. More high-end homes enter the market heavily in May and June for the summer sell season. Sellers at this price point will need patience, more time to sell, price their home competitively, show-ready, and creative marketing beyond normal to stand out from the inventory. All price points below $1 million have inventory volume gains compared to this time last year. A light snow winter contributed to inventory gains with homes coming on the market earlier. As a result, buyers are excited to have more home selection and sellers are thrilled for more showings. It appears the buyers and sellers who have entered the market are doing so because life circumstances have dictated them to do so.

“Financing homes with current interest rates is creating some hefty mortgage payments. This is especially true for first-time homebuyers who are also competing with second-home buyers searching for lower home prices. Historically, Pagosa Springs has been a big second-home market with attractive pricing compared to other Colorado resort communities. That is still true however, second-home buyers appear more discerning, especially when a mortgage is part of their home purchase scenario. Cash sales are still driving the higher price market ($900,000-plus). What appears to be one of the best buying and selling environments in years could be softened by uncertain and heightened living costs due to the Iran war or, it may also encourage more relocation toward the less complex Pagosa Springs rural lifestyle,” said Pagosa Springs-area REALTOR® Wen Saunders.

STEAMBOAT SPRINGS/ROUTT COUNTY

“Single-family numbers in Steamboat Springs exhibited an interesting reversal: in 2025, February was slow with only two sales while March jumped to 13; by 2026, the trend flipped, with February hitting 13 sales and March dropped to three. While the March closings were light, 17 homes went under contract. If they all close in April, the number of sold listings in April 2026 will surpass that of 2025. The market remained competitive through Q1; despite 10 fewer new listings, we still saw a net increase of three sales. Median sales price through March is down 21.4% to $1.572 million and average sales price is also less at $2.384 million.

“New listings for multi-family in Steamboat tell a similar story with 20% fewer new listings this year. However, there is more condo/townhome inventory for sale than there was last year. Sold listings were similar to 2025 with 31 transactions vs. 34. First quarter results have median sales prices up 3.6% to $896,000 and average sales prices up 24% to $1.269 million.

“Stagecoach and Oak Creek have only had 12 new home listings come on the market for the year – but that is three more than Q1 2025. Sales pace is equivalent with four transactions; however, median sales price is $1.050 million (+15.9%). The current inventory of homes on the market is 12, representing 4.8 months of supply. The townhome/condo market is limited with only five units on the market; an average sales price $434,667 and 3.3 months of inventory.

“Housing activity in Hayden for the quarter reveals five homes sold at an average sales price of $608,070. At present, there are 20 homes on the market with 15 of those priced below $900,000.

“Disregard the lion; March followed the weather and arrived like a lamb. We are now closing the quarter as a ‘sheep’—one that is steadily gaining mass as we transition into Q2,” said Steamboat Springs-area REALTOR® Marci Valicenti.

SUMMIT AND PARK COUNTIES

“March felt a bit like a bluebird day with thin coverage; beautiful on the surface but missing some of the depth we rely on. A lighter natural snow year put more pressure on snowmaking, which performed remarkably well, but tourism still softened. That ripple effect showed up in real estate activity, particularly in Summit County’s single-family segment where fewer buyers stepped in and prices eased.

“Meanwhile, the multi-family market quietly carved its own line, with values holding strong and even gaining ground, a reminder that different segments don’t always ride the same run.

Summit County – March 2026 compared to March 2025

Single-Family Homes:

• Number of Sales: 24% fewer single-family homes sold.

• Average Price: $2,591,292, a 3% decrease March 2026 compared to March 2025, and 14% down compared to the full year average in 2025.

• New Listings: are down 11% from last March.

Multi-Family Homes:

• Number of Sales: 8% fewer sales.

• Average Price: $943,921, up 9% March 2026 compared to March 2025, and 1% down compared to the full year average in 2025.

• New Listings: Down 3% from last March.

Park County – March 26 compared to March 25

- Number of Sales: 15% more sales

• Average Price: $677,427, a 3% increase March 26 compared to March 25, and 8% down compared to the full year average in 2025 - New Listings: Down 35% from last year

“Across Summit, Park, and Lake counties, 621 residential listings are currently on the market, ranging from a $35,000 mobile home in Breckenridge to a $21 million ski-in/ski-out Breckenridge home. More than half (55%) are priced above $1 million, with 37 listings over $5 million. The average list price is $1,673,974.

“In March, 106 residential closings ranged from a $155,000 single-family home in Alma to a $7.8 million Breckenridge home. About 63% of sales closed above the $1 million mark, and cash deals were 48% of all transactions.

“Early indicators for April suggest the market is starting to move. With 262 properties currently pending, this spring and summer may turn out to be a pretty fun ride,” said Summit-area REALTOR® Dana Cottrell.

TELLURIDE/SAN MIGUEL COUNTY

“Telluride regional market sales continue to be boosted by high-end sales in Mountain Village and the town of Telluride. With the national economy being messy and interest rates rising, the wealthy and especially the ultra-wealthy continue to buy whatever they want and aren’t very price sensitive. It’s more about finding what they want that best fits their family’s desires.

“March sales volume in San Miguel County came in at $71.12 million over 35 sales. Both stats are up over February sales, but below the last five-year average. I believe the market is becoming clearer and somewhat leveling out with increasing dollar amounts of sales over fewer transactions.

“As hard as the future is to predict, there are more wealthy individuals in the United States and globally than in history,” said Telluride-area REALTOR® George Harvey.

VAIL

“The Vail area experienced one of the most dramatic and challenging periods in the past 50 years. The snowpack and visitations were down significantly which impacted the economy and presents a major impact for the valley due to drought and significant shortfalls of reserves in the reservoirs moving into spring and summer months. The impact on small businesses could create significant failures. This in turn could have impact on jobs and force some locals to leave the valley. Should this occur, a possible impact on rental properties and opening price point homes is possible. Thus, the spring and summer markets are a difficult situation to forecast at this point.

Looking at the Real Estate Market in total units:

- Closed sales for March 2025 versus 2026 – positive 4.2%

- Closed sales YTD 2025 versus 2026 – positive 2.7%

- Pending sales March 2025 versus 2026 – positive 16.7%

- Pending sales YTD 2025 versus 2026 – positive 8.0%

- New listings March 2025 versus 2026 – minus 4.2%

- New listings YTD 2025 versus 2026 – minus 2.6 %

- Average Sales Price March 2025 versus 2026 minus 3.7%

- Average Sales Price YTD 2025 versus 2026 minus 3.3%

- Percent of list price received March 2025 versus 2026 – minus 1.4%

- Percent of list price received YTD 2025 versus 2026 between – minus 0.7%

- Inventory of active listings March 2025 versus 2026 – positive 6.9%

- Months supply of inventory – positive 6.5%

“Looking at pricing niches, we see differences between single family/duplex and townhome/condo. Single family/duplex has an overall performance of 8.7% with only three niches showing negative and the rest positive. Townhome/condo overall performance is negative in all but two niches however, last year, a number of new projects on the market were selling while this year that inventory is sold out.

“The first quarter performance has followed the trend of the past year maintaining reasonable stability with performance within norms despite macro economic turmoil. Thus, the real unknown is macro and outside the local market control.

“We will continue to work diligently in our market to maintain performance and deal with the factors outside us and deal with them as they occur,” said Vail-area REALTOR® Mike Budd.

WELD COUNTY

“The Weld County housing market is showing signs of stabilization as we move further into 2026. New listings remain steady, with 1,739 homes hitting the market year-to-date, a slight 0.4% increase compared to the same period in 2025. While inventory is still relatively limited, it has tightened slightly, with 1,097 homes currently for sale, down 6.6% year over year, representing about 2.6 months of inventory.

“Home sales softened slightly with 1,060 homes sold year-to-date, representing a 2.2% decrease from last year. Homes are also taking a bit longer to sell, with average days on market increasing to 87 days, up 8.7% from the previous year.

“Pricing has remained relatively stable overall. The median sales price is $500,000 year-to-date, down 2.9% from 2025, while the average sales price sits at $565,682, a 1.7% year-over-year decrease. Despite these small adjustments, sellers are still receiving strong offers, averaging 99.1% of their list price.

“The townhouse and condo segment has experienced a more noticeable slowdown in activity, with new listings down 22.5% year-to-date and sales down 7.8%. However, prices in this segment remain fairly stable, with a median price of $355,000 year-to-date, just 1.9% lower than last year.

“Overall, Weld County continues to demonstrate a balanced but slightly cooling market, where inventory remains relatively tight, homes are taking a bit longer to sell, and prices are stabilizing after several years of rapid growth,” said Weld County-area REALTOR® Amy Tallent.

The Colorado Association of REALTORS® Monthly Market Statistical Reports are prepared by Showing Time, a leading showing software and market stats service provider to the residential real estate industry and are based upon data provided by Multiple Listing Services (MLS) in Colorado. The March 2026 reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. CAR’s Housing Affordability Index, a measure of how affordable a region’s housing is to its consumers, is based on interest rates, median sales prices and median income by county.

The complete reports cited in this press release, as well as county reports are available online at: https://www.coloradorealtors.com/market-trends/

###

CAR/SHOWING TIME RESEARCH METHODOLOGY

The Colorado Association of REALTORS® (CAR) Monthly Market Statistical Reports are prepared by Showing Time, a Minneapolis-based real estate technology company, and are based on data provided by Multiple Listing Services (MLS) in Colorado. These reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. Showing Time uses its extensive resources and experience to scrub and validate the data before producing these reports.

The benefits of using MLS data (rather than Assessor Data or other sources) are:

Accuracy and Timeliness – MLS data are managed and monitored carefully.

Richness – MLS data can be segmented

Comprehensiveness – No sampling is involved; all transactions are included.

Oversight and Governance – MLS providers are accountable for the integrity of their systems.

Trends and changes are reliable due to the large number of records used in each report.

Late entries and status changes are accounted for as the historic record is updated each quarter.

The Colorado Association of REALTORS® is the state’s largest real estate trade association representing over 23,000 members statewide. The association supports private property rights, equal housing opportunities and is the “Voice of Real Estate” in Colorado. For more information, visit https://www.coloradorealtors.com.