Colorado housing markets find stability as buyers adapt to higher rates, balanced conditions

ENGLEWOOD, CO – Colorado’s housing market continued its transition into a more balanced and disciplined environment this spring, with both Denver-metro and statewide activity reflecting steady demand, stable pricing, and buyers increasingly adapting to mortgage rates above 6%, according to the latest Market Trends Housing Report from the Colorado Association of REALTORS® (CAR).

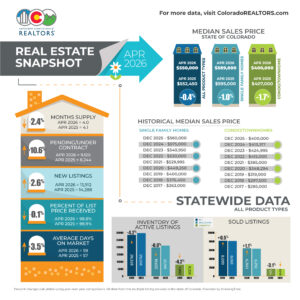

In the seven-county Denver metro area, April market activity mirrored patterns seen over the past several years. Pending contracts climbed 8.8% year-over-year even as new listings declined 5% from April 2025, signaling that buyers are adjusting to current borrowing costs rather than waiting for rates to fall. Home prices remained largely stable, with the median sale price rising just 0.3% to $586,867, while active inventory stayed roughly 2,000 listings below year-ago levels.

Across Colorado, market conditions are settling into a more balanced rhythm. Statewide pending sales increased 7.2% year-over-year and closed sales rose 2.7%, while median home prices dipped less than 1% to $545,000. REALTORS® across the state report that well-priced, move-in-ready homes continue to attract strong interest, while overpriced or higher-maintenance properties are seeing longer marketing times and increased negotiation.

Overall, the market is being shaped less by rapid appreciation or speculation and more by affordability, pricing strategy and seller flexibility as buyers and sellers adjust to a higher-rate housing environment.

“The bigger difference is absorption. Pending contracts rose 8.8% year-over-year in April and are up 4.1% year-to-date, while active inventory ended the month at 15,366 listings, roughly 2,000 fewer homes than were available at the end of April last year. That combination suggests buyers are not necessarily flooding back into the market, but they do appear to be more acclimated to the current rate environment and increasingly accepting that mortgage rates above 6% are not a temporary exception, but the operating baseline for now,” said Denver-area REALTOR® Cooper Thayer. “This remains a market defined by affordability constraints and negotiation, not broad-based price depreciation.”

Looking ahead, the market remains “highly selective, rewarding realistic pricing, thoughtful preparation and creative problem-solving on all sides of the transaction,” said Evergreen-area REALTOR® Julia Purrington Paluck.

Overall, REALTORS® across Colorado describe the market as stable, selective and increasingly driven by realistic pricing, affordability considerations and seller flexibility rather than straight demand.

“Like most places across the state, we continue to see an unpredictable market with properties that are well-priced, in a good location with good views and no work needed going under contract quickly and others lingering on the market. It seems to be a bit more balanced, and I wouldn’t say that buyers or sellers have the upper hand right now. That could change if we see significantly more properties come on the market, but it would take a lot to push us into a full buyer’s market,” said Crested Butte-area REALTOR® Molly Eldridge.

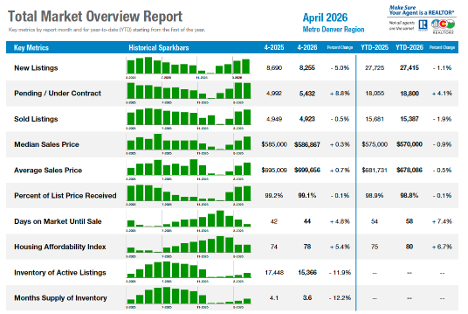

Total Market Overview – Seven-County Denver Metro

Total Market Overview – Statewide

Colorado Housing Markets – March Snapshot

Based on analysis from REALTORS® working in markets across the state

(for a more in-depth analysis by market, see full content in report):

Aurora – Aurora and Centennial’s housing markets remained sluggish this spring, with inventory levels surprisingly lower than last year and little evidence of a typical seasonal surge. Home prices declined 5%–10% in many zip codes, while closed sales also fell year-over-year. Single-family prices stayed mostly flat despite reduced inventory, while the condo and townhome market softened considerably with rising inventory, falling prices, and slower sales. Sellers are offering more concessions, creating attractive opportunities for entry-level buyers willing to consider attached housing options.

Boulder and Broomfield counties – Boulder and Broomfield counties continue to see active buyer interest, though pricing remains relatively flat and homes are taking longer to sell. In Broomfield, rising inventory is giving buyers more options and greater negotiating power, particularly in the condo and townhome market where supply has increased significantly. Boulder County remains tighter on inventory, supporting modest price gains. REALTORS® describe the market as balanced but unpredictable, with some homes attracting multiple offers while others sit longer, making pricing and presentation increasingly important.

Colorado Springs – The El Paso and Teller County housing markets continue to face headwinds as higher inventory, declining prices and economic uncertainty weigh on buyer demand. While sales edged up slightly in April, active listings rose 6.3% and median prices fell 2.7%. Buyers remain cautious amid elevated mortgage rates, inflation concerns and job uncertainty, with the condo and townhome segment seeing additional pressure from rising insurance and HOA costs. REALTORS® report a market increasingly favoring buyers, with more sellers than active buyers and expectations for continued price softening through the year.

Crested Butte/Gunnison – The Gunnison and Crested Butte housing markets remain active and generally in line with 2025 trends, though inventory is beginning to rise as an early snowmelt brings listings to market sooner than usual. Sales volume is slightly lower, but dollar volume and home prices continue to climb, driven largely by strong single-family activity and luxury sales. REALTORS® describe conditions as balanced but unpredictable, with well-priced homes moving quickly while others linger, creating opportunities for buyers to negotiate more aggressively this summer.

Denver Metro – The Denver-metro housing market continued its steady spring pattern in April, with activity levels closely resembling recent years. Pending contracts rose 8.8% year-over-year as buyers increasingly adjusted to mortgage rates above 6%, while inventory remained lower than last year. Home prices stayed stable, with the median sale price up just 0.3% to $586,867. REALTORS® describe the market as balanced to slightly buyer-favorable, with well-priced homes still moving quickly while overpriced listings face longer marketing times and greater negotiation.

Durango/LaPlata County – Durango and La Plata County saw strong spring activity for a second straight month, driven by rising inventory and a lighter snow season. Single-family sales climbed 39% year-over-year in April, while pending sales surged 52%. Inventory growth has created more buyer-friendly conditions, though well-priced homes continue to move quickly. Higher-end buyers remain active, while affordability challenges persist below the $700,000 range due to elevated mortgage rates, insurance costs, and HOA fees. Sellers are increasingly offering concessions to attract buyers.

Evergreen/Foothills – Colorado’s foothills housing market gained momentum this spring as showings, contracts, and closings increased, signaling buyers are adapting to higher mortgage rates rather than waiting for conditions to change. Single-family pending sales rose 15.6% year-over-year while prices remained relatively stable. REALTORS® report a more balanced and selective market, where well-priced homes continue to sell steadily but overpriced or outdated properties face longer marketing times and heavier negotiation. Creative financing incentives and seller concessions are also becoming more common to improve affordability and close deals.

Fort Collins – Fort Collins experienced a slower-than-expected April housing market, with declines in new listings, sales and home values raising concerns about market consistency. Single-family sales dropped 17% year-over-year while condo and townhome prices fell nearly 9%. Buyers remain cautious despite improving affordability, and sellers must price homes carefully to attract attention. REALTORS® note that fewer available homes and shorter days on market are still creating opportunities for competitive offers, though uncertainty continues to shape buyer and seller behavior.

Grand County – Grand County’s housing market is shifting into a more balanced spring season, with buyers becoming increasingly selective across its resort and rural communities. Luxury-driven Winter Park continues to command premium prices, while Granby and Fraser offer buyers more inventory and negotiating room. Grand Lake remains desirable for lifestyle and second-home buyers, while Kremmling and Hot Sulphur Springs continue attracting value-conscious shoppers. REALTORS® describe the market as “smarter,” where disciplined pricing and strong presentation are key to attracting today’s buyers.

Mesa County – As we move further into spring, new listings still lag behind 2025. A slight increase in activity is resulting in pending sales improving 6.7% over 2025, but a good number of transactions are not making it to closing. Sales are nearly 12% behind last April and, as a result, inventory is growing. We now have about a 3.5-month supply however, most of it is above $450,000. Unpredictably, prices still show an increase with the median at $405,000, up 1.5%, and the average at $468,322, up 3.9%.

Pagosa Springs – Pagosa Springs is seeing rising inventory and higher home prices as the market shifts toward more balanced conditions. Inventory jumped 42% year-over-year, driven largely by higher-priced homes, while average and median sale prices climbed sharply. Buyers remain price-sensitive, with updated homes priced near the median moving fastest, while overpriced properties linger longer on the market. REALTORS® report growing opportunities for negotiation as inventory expands, particularly in the luxury segment, though demand for the southwest Colorado lifestyle continues to support the market overall.

Pueblo County – Pueblo County’s housing market remained active and competitive in April, with closed sales rising 8.3% year-over-year and inventory tightening as active listings declined. Homes sold slightly faster, reflecting continued buyer demand despite moderating prices. Median and average sale prices both dipped modestly from last year, giving buyers slightly more negotiating power while sellers received a bit less of their asking price. REALTORS® describe the market as balanced, with resilient demand, constrained inventory and gradually softening pricing conditions.

San Luis Valley – The San Luis Valley market is continuing to balance out in 2026 as inventory rises across much of the region while buyer activity remains steady in several counties. Alamosa, and Rio Grande counties both saw increases in sold listings despite softer pricing, while Conejos County experienced especially strong momentum with sales and median prices rising sharply. Costilla and Mineral counties remain slower-paced markets with growing inventory and longer days on market, giving buyers more leverage. Meanwhile, Saguache County continues to post strong price growth alongside a significant increase in new listings.

Steamboat Springs/Routt County – Steamboat Springs and Routt County saw steady April sales activity, with buyers remaining active despite rising inventory and longer marketing times. Sellers received an average of 96.2% of asking price, though some listings required reductions before going under contract. Inventory increased significantly in both single-family and multi-family segments, creating more balanced conditions. REALTORS® noted a sharp increase in pending contracts compared to last year, signaling that serious buyers remain engaged across a wide range of price points despite broader market uncertainty.

Summit, Lake, and Park counties – Summit, Park, and Lake counties continue to see a selective but active spring housing market, with tight single-family inventory helping support prices while buyers become more cautious. Condo and townhome sales surged 22% year-over-year, reflecting strong demand ahead of the summer season. Luxury inventory remains prominent, with 42% of active listings priced above $1 million. REALTORS® report steady buyer engagement despite economic uncertainty, as pending sales and cash purchases remain strong across the region’s mountain communities.

Telluride – Telluride and Mountain Village posted a strong April with $70.6 million in sales volume across 38 transactions, reflecting a 24% year-over-year increase in dollar volume despite fewer overall sales. Activity remains healthy across most price ranges, while limited inventory and strict land constraints continue supporting price stability. REALTORS® report only modest price adjustments in most cases, with seller and buyer behavior closely mirroring recent years. Overall, the market remains stable, selective, and resilient despite broader economic uncertainty.

Vail – Vail-area resort markets posted strong spring activity during the traditional “shoulder season,” with sales up 17.7%, pending sales rising 33.3% and inventory increasing modestly year-over-year. Median prices declined, though REALTORS® say the shift reflects changing inventory mix more than weakening demand. Activity remained strong across several price ranges, particularly in the condo and luxury home segments. Overall, the market continues to show relative stability, with local supply trends outweighing broader economic uncertainty as the summer selling season approaches.

Weld County – Weld County’s housing market continues moving toward more balanced conditions, with steady buyer demand and moderating home prices. Closed sales rose 7.5% year-over-year in April, while new listings declined, keeping inventory relatively tight. Median prices softened modestly to $499,000, reflecting a healthy correction after years of rapid appreciation. Homes are still selling near asking price, though buyers are gaining more negotiating power as days on market increase. REALTORS® say success now depends more on strategic pricing and presentation than market speed.

Taking a more in-depth look at some of the state’s local market data and conditions, the Colorado Association of REALTORS® Market Trends spokespersons provided the following assessments:

AURORA

“Repeat and ditto are the best words to describe the May real estate sales in Aurora and Centennial. Active listing inventory is down, which is surprising for this time of year. With the exception of 80011, every zip code revealed much lower inventory levels than in 2025. The spring rush did not happen, and if it did, the numbers do not reflect it.

“Year-over-year pricing fell 5 – 10% in many zip codes. Closed sales are also down year over year. It is interesting that, even with lower inventory, we have not seen a price increase on single-family residential homes. Zip codes 80013, 80015, 80018 all had a slight price increase however, not enough to get too excited about.

“Adams County currently has about 1240 homes on the market at a median price of $521,000. Arapahoe County has approximately 1065 homes for sale at a price of $604,000. Aurora has a median price of $525,000 with 815 homes on the market and Centennial is at a median price of $725,000 with only 155 homes on the market. It seems that homes are on the market 30-60 days before they are in a pending status.

“The townhome/condo market is a much different market. Inventory is up considerably and sales are down. Pricing for the condos are also greatly reduced over last year. For an entry level buyer, perhaps they should check out condos and townhomes. Pricing is attractive and sellers seem to be generous with the seller concessions they are offering,” said Aurora REALTOR® Sunny Banka.

BOULDER/BROOMFIELD COUNTIES

“In Boulder and Broomfield counties, the market is bustling but the numbers aren’t moving much. More listings and more choices bring curious buyers, but prices are stagnant and days on the market continue to increase.

“In Broomfield County, more sellers are choosing to move despite their coveted low interest rate, pushing listings up 14%. Increased supply is giving buyers more options and putting slight downward pressure on prices compared to earlier this year. Homes are averaging 56 days on the market, a small increase but still within a reasonable range of what can be considered a balanced market.

“The townhome and condo market in Broomfield remains steady year over year in terms of listings, prices, and sales. However, days on market have risen sharply to 86, creating about five months of inventory. New construction is adding to supply and giving buyers stronger negotiating power in this segment of the market.

“In Boulder County, sellers are more cautious, with listings down 7%. Limited inventory is supporting prices, which are up nearly 3%. Homes are averaging 70 days on market, giving buyers time to be selective.

“From the perspective of a REALTOR® working each day in this market, there is an unpredictability about which houses will sell quickly and which ones will take months. Many of us are experiencing multiple offers and bidding wars in certain pockets of the market, while other homes are taking much longer to sell. Pricing and presentation remain key and while the spring market is fairly lackluster, there are bright shiny spots with homes selling over a weekend.

“Overall, the market is balanced but a bit unpredictable,” said Boulder/Broomfield-area REALTOR® Kelly Moye.

COLORADO SPRINGS

“The Front Range market of El Paso County and Teller continues to drag. April saw a 1.8% increase in total units sold from last year, but we remained 6.3% higher on active listings and our median price continues to pull back, down 2.7%. At the ground level it felt like a drag and is a mixed bag house by house. Many homes see price reductions, some getting multiple offers but overall, buyers continue to sideline under higher home prices, higher gas prices, higher interest rates, and job fears. The townhome and condo market continues to feel more pain than single family due to continued unknowns in insurance and HOA fees.

“Other indicators continue to point to economic pressures that are worth noting. The average car owner is now upside down $7,200 dollars per vehicle in Q1 2026. It is the fourth consecutive annual increase. American economic confidence is now below 2020 levels with 73% of Americans thinking the economy is getting worse. To top it off, the private equity firms, also known as hedge funds, continue to show stress.

“The fact remains that the housing market is running out of buyers. There are 46.3% more sellers than buyers in February, and that number continues to remain out of balance. Denver was ranked as one of the higher depreciating markets, and that is sure to push down the front range. With higher inventory, values dropping, and a lack of buyers both locally and nationwide, I expect that home prices will continue to pull back throughout the year. Sellers who need to sell, should take this time to do so and be realistic about it. I do not see anything getting better for the remainder of this year,” said Colorado Springs-area REALTOR® Patrick Muldoon.

CRESTED BUTTE/GUNNISON

“The Gunnison – Crested Butte area real estate market continues to mirror 2025 but we are starting to see signs of a change with more residential properties coming on the market. The lack of snow this winter means that our hiking and mountain biking trails are open earlier than usual and that could mean more May and June visitors. Typically, the Gunnison market has inventory coming on in March and April while Crested Butte is more like late May or early June. This year, the timeline was pushed up a bit as the snow was melting and the ground became visible. The numbers are not dramatic, but every day new properties are coming up for sale, and I would expect that to continue into June or even throughout the summer.

“The overall market through April has brought a few less sales (down 4% from 143 to 136), but an increase in dollar volume (up 13% from $123 million to $140 million). This is mostly attributable to single-family home sales which are up 15% in number and 21% in dollar volume. Condo and townhome sales are stable throughout the area. Average prices are up from 2025 in the valley – 5% for single-family homes and 26% for condos and townhomes. Looking at inventory overall, the number of listings is about the same as it was last year. However, the number of residential listings is up 24%, providing more opportunities for buyers. This number is still down about 20% from 2019 (pre-Covid) so there is plenty of room for improvement.

“In Crested Butte, the number of sales continues to be similar, but dollar volume is up about 14%. Again, single-family home sales are leading the market in terms of dollar volume. With almost the same number of homes sold (19 in 2026 vs. 20 in 2025), the total volume is up from $49 million to $58 million, an increase of 18%. Obviously, this is reflected in the average price, up 24% this year and currently just over $3 million. Does this mean you cannot find a home in the area for less than $2 million? It does not. But the definition of ‘luxury’ has changed in the last few years here and is demonstrated by these statistics. As more high-end homes are built, some will come up for sale at higher prices and that will push the average price up. Condo and townhome sales are growing as well with 35 sales in the first four months vs. 31 last year. Total dollar volume is up 27.5% and the average price is just over $1 million (up 13% from 2025). Looking at inventory, again the total number of listings is the same as last year, but residential listings are up 26% and I expect that number to grow as we head into the summer.

“In the Gunnison Area, the number of sales continues to lag behind 2025, but the gap is getting smaller. Single-family homes lead the charge here as well with 4 more sales than last year (25 vs. 21) and about $2 million more in dollar volume. The average price of a home is down slightly to $688,000, but the median home price is up from last year to $740,000. Condo sales have made up some ground but continue to be very slow. There have been only seven condo or townhome sales in 2026, and prices are below last year with an average price of $286,000. There are more condos and homes for sale than there were at this time last year in the Gunnison area, so it is a good time to take a look.

“Like most places across the state, we continue to see an unpredictable market with properties that are well-priced, in a good location with good views and no work needed going under contract quickly and others lingering on the market. It seems to be a bit more balanced, and I wouldn’t say that buyers or sellers have the upper hand right now. That could change if we see significantly more properties come on the market, but it would take a lot to push us into a full buyer’s market.

“For now, the suggestion is the same. Buyers should be prepared to make a move if the right property comes along and should feel like they can submit a lower offer to sellers whose properties that have been on the market for a while to see if the seller is ready to negotiate. Our average days on market is much longer than they are in a primary home market so talk to your REALTOR® to decide what length of time makes sense before you start testing things. Sellers who want to sell this summer need to be aggressive with their pricing, not below what your neighbor sold for last month, but probably not above it either,” said Crested Butte-area REALTOR® Molly Eldridge.

DENVER METRO (Seven County)

“The Denver-metro housing market moved fully into its spring rhythm in April, with new listings, pending contracts, and closed sales all landing in a range that looks very familiar compared to the last several years. New listings came in at 8,255 for the month, down 5% from last April, but year-to-date new listings are almost identical to last year, with 27,415 homes hitting the market through the first four months of the year, only 1.1% below the same period in 2025. With the seasonal listing cycle now in full swing, May is still likely to be the peak month for new supply, but so far this year does not look like a major departure from the post-2022 market pattern.

“The bigger difference is absorption. Pending contracts rose 8.8% year-over-year in April and are up 4.1% year-to-date, while active inventory ended the month at 15,366 listings, roughly 2,000 fewer homes than were available at the end of April last year. That combination suggests buyers are not necessarily flooding back into the market, but they do appear to be more acclimated to the current rate environment and increasingly accepting that mortgage rates above 6% are not a temporary exception, but the operating baseline for now.

“Pricing continues to reflect stability more than pressure in either direction. The median sale price across the Denver-metro market was $586,867 in April, up just 0.3% from last year, while the average sale price rose 0.7% to $699,656. The same basic pattern showed up across both major segments, with the single-family median rising 0.8% year-over-year to $635,000 and the condo-townhome median holding flat at $395,000. In other words, despite higher borrowing costs, longer marketing times, and more buyer selectivity, values have not materially broken down. This remains a market defined by affordability constraints and negotiation, not broad-based price depreciation.

“Buyer leverage has improved slightly, but it is still uneven. Homes took an average of 44 days to sell in April, up from 42 days last year, and sellers received 99.1% of list price on average, slightly below last year’s 99.2%. Year-to-date, the market is averaging 58 days on market and 98.8% of list price received, both consistent with a more deliberate, more disciplined environment. The attached segment remains more buyer-favorable, with 5.7 months of supply and 56 days on market, while single-family homes continue to show stronger absorption, especially in desirable neighborhoods and lower price ranges where entry-level inventory is still relatively scarce.

“At a broad level, I would call the market balanced to slightly buyer-favorable from a negotiation standpoint, but that does not mean every buyer has leverage in every submarket. Well-priced single-family homes in high-demand areas are still capable of moving quickly, while overpriced listings, especially in more affordability-sensitive segments, are facing more resistance.

The interest rate backdrop remains the controlling variable. In April, Mortgage News Daily’s 30-year fixed daily survey spent most of the month between roughly 6.29% and 6.56%, averaging around 6.37%. That is not low enough to create urgency, but it appears stable enough for many buyers to plan around. Overall, the first third of 2026 has looked very similar to 2025, 2024, and 2023: steady transaction flow, stable prices, elevated but manageable inventory, and a market where execution matters more than speculation. I expect total sales volume to remain broadly consistent with the last several years, with the main difference being how we get there. This year’s market is likely to be shaped less by dramatic swings in demand and more by the day-to-day mechanics of pricing, presentation, payment sensitivity, and seller flexibility,” said Denver County-area REALTOR® Cooper Thayer.

DURANGO/LA PLATA COUNTY

“The region experienced its second month in a row of sales surpassing year-over-year March and April sales, attributed to the higher amount of inventory on the market in 2026 and the lighter-than-usual snow season. Single-family sold listings were up 39% in number over April 2025 and are up 12% year to date. Condo and townhome sold listings are up 6% April year over year in number, and up 40% year to date.

“Pending sales rose sharply compared to April 2025, up 52% in number; single-family pending sales led the way up 69% over April 2025.

“Inventory is still growing for both single-family and condo-townhome property types, placing the months’ supply of available inventory firmly into a buyer’s market on paper, traditionally defined as any market with over a six-month amount of inventory. The experience is different in the field. Homes on the market do tend to sit if they are in rural areas, have deferred maintenance, or are priced too high for the perceived value, but many homes do come and go rapidly under contract as well. Sellers have become more agreeable to concessions for inspection items than a few years ago.

“Buyers are more active at prices above $700,000, while sales in the lower ranges have fallen. Current inventory is climbing most in the $400,000 – $700,000 range. This could point to a K-shaped economy where those in the upper echelons are doing well, while those breaking into the market under $700,000 make up a population struggling to afford the prices Durango and La Plata County have risen to, along with an interest rate stuck in the mid-6% range, steeply rising insurance and higher HOA fees produced by insurance.

“It is of note that, though inventory is rising, there are fewer homes for sale than what was common pre-COVID, before inventory in the region was gobbled up by out-of-area buyers.

“Newsworthy regions of La Plata County in April are in-town Bayfield, where the inventory of resale single-family homes for sale doubled since April 2025. Rural Bayfield had a phenomenal month of closings but still remains in a buyer’s market with 7.3 months of inventory. The median single-family home in-town Durango is currently $940,000, and in-town Bayfield is $554,775,” said Durango-area REALTOR® Heather Erb.

EVERGREEN/MOUNTAIN METRO

“Spring activity has clearly arrived in the Colorado foothills housing market, bringing renewed energy after a prolonged period of cautious buyer behavior. Showings, contracts, and closings all improved through April, reflecting the seasonal momentum that typically builds this time of year. At the same time, the market continues to feel notably more balanced and selective than the fast-moving conditions buyers and sellers experienced several years ago.

“Across the broader foothills’ region, single-family under-contract activity increased 15.6% year over year while sold listings rose 19.2%. Median pricing remained relatively stable, increasing 1.4% to $710,000. Inventory levels, which expanded dramatically throughout much of 2025, have also begun to stabilize, with active listings down nearly 10% from last year.

“While these numbers reflect improving activity, much of the increase is consistent with normal seasonal spring demand patterns. The more meaningful shift may be that buyers, sellers, lenders, and agents are increasingly adapting to today’s higher-rate environment rather than waiting for conditions to change dramatically.

“Creative financing solutions are becoming a much larger part of the market conversation. Seller concessions for mortgage rate buydowns are increasingly common, and many lenders are now offering temporary one-year buydown programs to help improve affordability. Combined with more strategic pricing and negotiation from both buyers and sellers, these efforts appear to be helping more transactions successfully reach the closing table.

“Buyer behavior also continues to evolve. Showing activity remains healthy across the foothills but, buyers are generally making decisions more deliberately and efficiently than earlier this year. Well-priced homes in desirable locations are still moving steadily, while properties that are overpriced, need significant updates, or present insurance challenges continue to experience longer marketing times and heavier negotiations.

“Evergreen and Conifer continue to reflect this more selective upper-end market dynamic. Median pricing in the area declined 5.5% year over year to $855,000, while average sales price softened 6.4%. However, contract activity increased nearly 25% and sold listings rose almost 40%, suggesting that demand remains active when homes are priced appropriately for current market conditions. Days on market increased to 55 days, reinforcing that buyers remain patient and price sensitive.

“Price-per-square-foot trends across the foothills also suggest the market is stabilizing rather than declining. Values remain below peak 2024 levels in several foothills’ communities, particularly within the luxury segment, but still sit well above pre-pandemic pricing levels overall.

“Mortgage rates continue to shape affordability and buyer psychology, but the foothills market increasingly appears to be adjusting to current conditions rather than waiting for a significant drop in rates. For now, the Colorado foothills market is beginning to feel healthier, more balanced, and more sustainable. While spring momentum is certainly building, the market remains highly selective, rewarding realistic pricing, thoughtful preparation and creative problem-solving on all sides of the transaction,” said Evergreen-area REALTOR® Julia Purrington Paluck.

FORT COLLINS

“During a traditionally busy time, the Fort Collins real estate market took a bit of a step back in April. It’s too early to tell if this is an indication of a deeper trend or just a hiccup, but it is disappointing to see the market behaving in a rollercoaster fashion month to month. It’s hard to find footing, difficult to pick a direction, and buyers and sellers find very little comfort in the uncertainty.

“The single-family detached market had a sizeable drop in new listings this April, down 18% from April 2025. In a month where the market is usually ramping up, this was clearly a step back. There were just 186 sales in April, down 17% from April 2025. With less inventory and fewer sales, you might expect more competition with buyers however, median value was down 3% to $607,750. While conditions are fairly balanced, buyers are still very cautious in most market segments, while sellers need to be on-point and accurate when pricing and presenting new listings to the market.

“The attached condo and townhome segment had a rough April as well. New listings were down 26.6% compared to April 2025, and there were only 52 sold listings, down 14.8% from the same period last year. Median value declined in a large way, down to $379,500, an 8.6% drop from April 2025. While I believe this is just a statistical anomaly, it is a warning that if the value-conscious segment of the market is struggling, there could be further cracks in the market as a whole.

“If buyers are looking for a silver lining in the Fort Collins market: affordability is improving. While this might not necessarily be felt as interest rates have been stubborn and insurance and HOA fees will never decline, there is opportunity to find value. For sellers, understand there are still very serious buyers in the market who are making strong, competitive offers. Days on market has dropped significantly in both single family and attached markets, and there are fewer homes for buyers to choose from which can spur competition, if properly positioned. Let’s hope that May brings further energy and activity otherwise, we could be in for a rough quarter,” said Fort Collins-area REALTOR® Jared Reimer.

GRAND COUNTY

“In April 2026, Grand County felt like a market shifting from slower winter days into a true spring strategy. Winter Park is still the luxury heartbeat. Prices remain high, with April sales around the $1.5 million range, but buyers are more selective and homes are taking roughly three months to sell. The story here is not ‘slow,’ it is ‘premium buyers demanding premium presentation.’

“Fraser feels steadier and more practical. With a median April sale price around $779,000 and days on market near 83, Fraser is moving but not racing. Buyers like the location and lifestyle, yet they are comparing value carefully.

“Granby is the workhorse of the county. April showed a median sale price around $830,000, 159 active listings, and about 100 days on market. Granby has inventory, choice, and continued demand, especially for buyers wanting more space or newer product than the resort core.

“Grand Lake remains the emotional purchase. Buyers here are shopping for water, views, legacy, and lifestyle. The market is more niche, but the charm factor still carries weight, especially for well-located cabins, lake-area homes, and second-home retreats. Median price is $800,000, down 2% from last year and days on market near 69 days. Still considered a sellers’ market in Grand Lake, based on having only 85 listings with buyer demand picking up for the prime lake selling season.

“Kremmling is the value and land story. Typical values are much lower than the resort towns, around $538,000, and values up about 1% year over year. It appeals to buyers wanting space, affordability, and a less resort-driven feel.

“Hot Sulphur Springs is quietly gaining attention. The market shows an average value around $518,000, up 2.9% year over year, making it one of the more affordable pockets with modest upward movement. Overall, Grand County in April 2026 is not a runaway seller’s market, it is a smarter market. Buyers have more room to negotiate, sellers have to price with discipline, and the homes that win, are the ones that tell the clearest lifestyle story,” said Grand County-area REALTOR® Monica Graves.

MESA COUNTY

“As we move further into spring, new listings still lag behind 2025. A slight increase in activity is resulting in pending sales improving 6.7% over 2025, but a good number of transactions are not making it to closing. Sales are nearly 12% behind last April and, as a result, inventory is growing. We now have about a 3.5-month supply however, most of it is above $450,000. Unpredictably, prices still show an increase with the median at $405,000, up 1.5%, and the average at $468,322, up 3.9%,” said Mesa County REALTOR® Ann Hayes.

PAGOSA SPRINGS

“The housing market continues to show signs of higher inventory gains and increased prices across the first four months of the year. April inventory was up 42.2% with 91 new listings that contributed to an early spring with warmer day temperatures and green grass. Much of the inventory gain were with homes priced higher than April’s median and average price points. The April 2026 average sales price compared to April 2025 was up more than 20% at $776,563. April 2026 home sales were sluggish at 23 compared to 28 in 2025 and a reflection of lower inventory in homes priced under the average and median prices.

“Price reactive buyers are waiting for more inventory. Reality shows homes priced under the median and average price points require updates, repairs, and include townhome living. Sales of inventory show some price reactive buyers are taking on these factors to meet their purchase comfort level. Buyers pounce on new inventory homes that are priced at or below average to median price points and beautifully updated. Sellers priced over experience longer days on market. Homes priced in the median sales range climbed in the number of homes sold, while homes priced higher than median and average sales prices declined. The median sales price of $605,000 was up from April 2025, and $636,250 YTD show some buyers are adjusting their purchase expectations to higher prices for the opportunity of a rural Colorado lifestyle.

Average Sales Price – $776,563 (up 20.8% over the 2025 price of $642,907)

Median Sales Price – $605,000 (up 17.9% over the 2025 price of $513,500)

Days on Market – 136 (up 1.0%)

“With 264 current listings, including 225 homes, 39 townhomes/condos, a rising 57% are priced beyond the average and median sales prices. Months’ supply of inventory climbed to 9.2. Pagosa Springs has an early high inventory with more than 72 homes priced above $1 million. Total homes sold in 2025 in this price range were 60. Unless higher priced homes sell, our months’ supply of inventory will climb, a reflection of the inventory gain in higher priced homes and amount of time to achieve a sale.

“Buyers continue to evolve into their purchase price and understand the value and beauty of rural southwest Colorado lifestyle living. A more balanced market is progressing. Spring and summer buyers and sellers continue to set the Pagosa Springs market trend,” said Pagosa Springs-area REALTOR® Wen Saunders.

PUEBLO COUNTY

“In April 2026, the Pueblo County single-family housing market showed strong activity and continued buyer demand despite softer pricing trends. New listings held steady year-over-year at 397 homes, while sold listings increased 8.3% to 223 closed sales, signaling healthy market momentum. Homes sold more quickly as days on market fell 2.2% to 92 days, and inventory tightened significantly, with active listings dropping 5.6% to 988 homes and months of supply decreasing 9.3% to 4.9 months.

“Pricing metrics reflected a modest market correction, as the median sales price declined 2.4% to $324,975 and the average sales price dipped 2.2% to $324,403 compared to April 2025. Sellers also received slightly less of their asking price, with the percent-of-list-price received slipping from 98.8% to 97.1%.

“Year-to-date trends paint a similar picture: sales activity is up 10.1%, while median prices are down 6%, suggesting buyers are gaining a bit more negotiating power even as demand remains resilient. Overall, Pueblo County continues to experience a balanced but competitive market, characterized by solid sales activity, constrained inventory and moderating home prices,” said Pueblo-area REALTOR® David Ramirez.

SAN LUIS VALLEY

“The San Luis Valley real estate market is continuing to balance out in 2026, with inventory levels rising across many counties while buyer activity remains steady in several areas. In Alamosa County, year-to-date sold listings increased 12% compared to last year, though the median sales price declined 15% to $263,500 and days on market increased nearly 40% to 134 days. Inventory also rose 16%, giving buyers more choices.

• Conejos County has seen one of the strongest increases in buyer activity, with year-to-date sold listings up 240% and the median sales price rising 21.2% to $315,000. At the same time, inventory climbed 30%, while homes are selling faster than last year with average days on market dropping nearly 29%.

• Costilla County remains more price-sensitive, with year-to-date median sales prices down 4% to $240,000 despite new listings increasing more than 10%. Months supply of inventory jumped 52.7% to 14.2 months, signaling a slower-paced market with increased buyer leverage.

• In Mineral County, inventory expanded sharply by nearly 73%, while homes took significantly longer to sell, averaging 134 days on market year-to-date. Median prices remain relatively stable at $382,000, down just 2.1% from last year.

• Rio Grande County experienced a 17.9% increase in sold listings year-to-date, though median sales prices declined 32.3% to $325,000. Homes are moving slightly faster than last year, and inventory levels remain relatively stable.

• Saguache County continues to show strong pricing momentum, with the year-to-date median sales price rising 25.5% to $366,500 and average sales prices up 13.6%. New listings doubled in April compared to last year, signaling growing seller confidence, although inventory remains elevated at over 14 months of supply.

“Overall, the Valley continues shifting toward a more balanced market, with increased inventory creating opportunities for buyers while well-priced properties are still attracting strong interest across many communities,” said San Luis Valley-area REALTOR® Megan Bello.

STEAMBOAT SPRINGS/ROUTT COUNTY

“Forty-eight properties exchanged ownership across the county in April, similar to 49 a year ago. Thirteen of those listings incurred a price reduction from their original list price before going under contract; with sellers in Steamboat receiving 96.2% of their list price. Homes that sold in Steamboat averaged 79 days on market, while the condo/townhomes that sold averaged 54.

“The Amble has completed construction of its 42-unit development; 13 condominiums closed with sales- price-per-square-feet ranging from $1,530 – $2,099. The highest single-family sale was a 4,201 square-foot home in The Sanctuary for $5.895 million and the highest multi-family sale was a 2,423 square-foot condo at The Amble for $5.085 million.

“There were 90 new listings for the period compared to 88 in April 2025. Through the first third of the year, Routt County has 13% fewer new listings coming to the market than last year. In Steamboat, inventory of homes for sale is up 40% for single-family homes with 5.8 months’ supply, 30.7% for multi-family with 7.1 months’ supply. Oak Creek/Stagecoach and Hayden areas have inventories similar to last year. The difference being more time on market to sell with Oak Creek at approximately a 5-month supply for both single and multi-family, 7.5 months for a home in Hayden, and 4.5 months for a townhome.

“April 2026 saw a significant surge in activity, with 26 properties pending – a stark contrast to the two properties under contract in April 2025. This activity included properties priced from $500,000 – $2.85 million. While seven listings required price adjustments to secure a buyer, the overall momentum proves that despite broader market noise, serious buyers are actively making moves,” said Steamboat Springs-area REALTOR® Marci Valicenti.

SUMMIT AND PARK COUNTIES

“With a warm winter giving way to fresh snow and freezing temperatures, the high country is doing what it always does in spring: changing its mind every few days. The real estate market is showing similar shifts. Traditionally, the post-ski season brings a noticeable wave of new listings, but that pattern has yet to fully materialize for single-family homes in 2026. Inventory remains tight in that segment, helping support prices even as buyers become more selective.

“At the same time, the multi-family market continues to gain momentum. Condo and townhome sales jumped 22% compared to last April, a strong signal that buyers are still actively positioning themselves for summer in the mountains.

Summit County – April 26 compared to April 25

Single-Family Homes:

• Number of Sales: Flat year-over-year, with the same number of homes sold

• Average Price: $3,229,990, a 37% increase over April 2025, though still 2% below the 2025 full-year average (a $10 million sale helped bolster that average number)

• New Listings: Down 23% from last April

Multi-Family Homes:

• Number of Sales: Up 22%

• Average Price: $842,498, up 4% from April 2025 and essentially flat with the 2025 full-year average

• New Listings: Up 5% from last April

Park County – April 26 compared to April 25

- Number of Sales: 17% more sales

• Average Price: $622,033, a 22% increase over April 2025 and roughly flat with the 2025 full-year average - New Listings: Up 11% from last year

“Across Summit, Park, and Lake counties, 694 residential listings are currently on the market, ranging from a $35,000 mobile home in Breckenridge to a $25 million ski-in/ski-out Breckenridge home. About 42% of all active listings are priced above $1 million including 39 listings over $5 million. The average list price across the region is $1,611,864.

“In April 115 residential closings ranged from a $27,500 single family home in Hartzel to a $10 million Breckenridge home. Approximately 44% of sales closed above the $1 million mark, and cash purchases represented 44% of all transactions. Another 259 properties are currently pending, suggesting buyers are still very much engaged despite ongoing economic uncertainty.

“Spring in the mountains is never predictable. One day it’s powder skis, the next day it’s patio furniture. Real estate feels much the same right now, but the steady pace of pending sales suggests this market may be warming up right alongside the wildflowers,” said Summit-area REALTOR® Dana Cottrell.

TELLURIDE/SAN MIGUEL COUNTY

“April was a strong month for gross volume, totaling $70.6 million across 38 transactions. Monthly statistics show a 24% increase in gross volume, though transactions were down 10% compared to last year. Year-to-date, gross dollar volume is up 15%, while transactions remain slightly lower at -3%. Notably, we have seen year-to-date activity across virtually every price point except for those over $20 million, reflecting positive diversification in the market. We are seeing some asking prices adjusted lower, but generally only 5% to 10%. The first four months of 2026 seem to be remarkably similar in seller strategies and buyer selections. There is still little inventory due to the physical land constraints of the boundaries of Telluride and Mountain Village. Those parameters help keep prices stable. Infrequently, we do see a seller very motivated who lowers their asking price aggressively, but that is the exception, not the rule,” said Telluride-area REALTOR® George Harvey.

VAIL

“April in the resort areas is generally referred to as the Shoulder Season. The period between the end of the ski season and beginning of the summer selling season. However, April 2026 was a active month and the trends followed the direction of the last number of months. Compared to 2025, April was positive in all property activity with sales up 17.7%, pending sales up 33.3 %. New listings were 10.1% positive, total inventory up 3.9% and months’ supply of inventory static at 6.3 months. Days on market until sale was negative 13.7%, which is a positive component in demand for transactions.

“The median sales price was down 16 % for single family/duplex and 54.7% for townhouse/condo units. However, the pricing difference in both categories was driven more by availability of product than demand forcing the trend. In 2025, there was a significant volume driven by a specific development in townhouse/condo product which is sold out. The trend for single family/duplex had the opposite effect as developments in that category are on the rise.

“In the pricing niches year over year, single family/duplex had significant sales in the $1 – $1.5 million range, up 75%, the $600,000 – $1 million range was up 57.1%, $2.5 – $5million plus was up 47.6%. The townhouse/condo market had positive performance in the $300,000 – $600,000 niche, up 171.4%. These trends are similar to what we have been for the period going back into 2025. There is a definite correlation between the actual performance and the inventory in the niche.

“The trends are impacted by macro-economic factors, and the volatility of these factors is difficult to predict going forward. The summer season really kicks in during July, and I am sure we will see some swings in these factors by that time.

“The best projection at this point is relative stability in the market with minor swings caused by components outside our local market. The basis for the stability is the trends that have been existent for the past 12 months which tend to be locally controlled. May and June will definitely be watched closely as we strategize for the summer season,” said Vail-area REALTOR® Mike Budd.

WELD COUNTY

“Weld County is continuing its shift into a more balanced housing market this spring, with a mix of steady demand and moderating prices. Closed sales are up 7.5% year-over-year for April and up 1.9% year-to-date, showing that buyers are still active despite broader market adjustments.

“At the same time, new listings are down 16.2% for the month and down 3.8% year-to-date, keeping inventory relatively tight even as buyer activity holds steady. Home prices have softened slightly, with the median sales price down 5.6% year-over-year for April and down 3.7% year-to-date to $499,000, reflecting a healthy correction after several years of rapid growth. Homes are still selling close to asking price, with sellers receiving 99.5% of list price, indicating continued demand when homes are priced appropriately. The pace of the market has slowed modestly, with days on market increasing to 81 days year-to-date, giving buyers more time and negotiating power compared to recent years.

“Bottom line, Weld County remains a stable and active market, but one that requires more strategy than speed. Buyers are gaining leverage, while sellers who price and present their homes well are still seeing strong results,” said Weld County-area REALTOR® Amy Tallent.

The Colorado Association of REALTORS® Monthly Market Statistical Reports are prepared by Showing Time, a leading showing software and market stats service provider to the residential real estate industry and are based upon data provided by Multiple Listing Services (MLS) in Colorado. The April 2026 reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. CAR’s Housing Affordability Index, a measure of how affordable a region’s housing is to its consumers, is based on interest rates, median sales prices and median income by county.

The complete reports cited in this press release, as well as county reports are available online at: https://www.coloradorealtors.com/market-trends/

###

CAR/SHOWING TIME RESEARCH METHODOLOGY

The Colorado Association of REALTORS® (CAR) Monthly Market Statistical Reports are prepared by Showing Time, a Minneapolis-based real estate technology company, and are based on data provided by Multiple Listing Services (MLS) in Colorado. These reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. Showing Time uses its extensive resources and experience to scrub and validate the data before producing these reports.

The benefits of using MLS data (rather than Assessor Data or other sources) are:

Accuracy and Timeliness – MLS data are managed and monitored carefully.

Richness – MLS data can be segmented

Comprehensiveness – No sampling is involved; all transactions are included.

Oversight and Governance – MLS providers are accountable for the integrity of their systems.

Trends and changes are reliable due to the large number of records used in each report.

Late entries and status changes are accounted for as the historic record is updated each quarter.

The Colorado Association of REALTORS® is the state’s largest real estate trade association representing over 23,000 members statewide. The association supports private property rights, equal housing opportunities and is the “Voice of Real Estate” in Colorado. For more information, visit https://www.coloradorealtors.com.