Colorado’s housing market remains steady as summer buying season settles into more balanced rhythm

Single-family prices continue to climb while buyers remain selective and sellers find success with realistic pricing

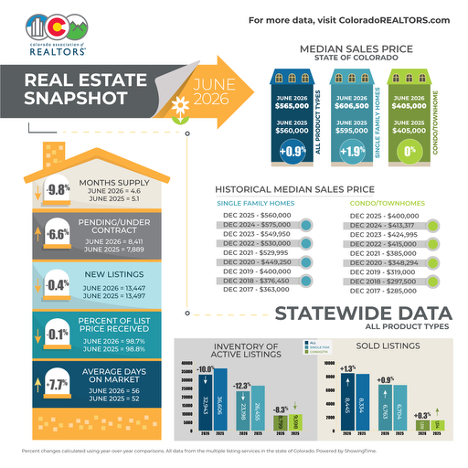

ENGLEWOOD, CO – The Colorado housing market continued its steady pace in June, with signs of a more balanced market taking hold across much of the state, according to the latest Market Trends Housing Report from the Colorado Association of REALTORS® (CAR). While elevated mortgage rates and affordability challenges continue to influence buyer behavior, REALTORS® report that buyers remain active but are taking more time to make decisions, negotiating more strategically and responding favorably to homes that are priced appropriately and presented well.

Statewide, single-family home sales increased 0.9% year over year, while the median sales price rose 1.9% to $606,500. Pending sales climbed 6.6%, signaling continued buyer activity even as the pace of the market remains more measured than in recent years. Townhome and condominium sales also remained stable, increasing 0.3% from one year ago, while prices held essentially flat. Inventory continued to improve seasonally, giving buyers more opportunities while helping create a healthier balance between supply and demand.

“The broader takeaway is that lower inventory does not automatically create a seller’s market,” said Denver County-area REALTOR® Cooper Thayer. “The market’s outcomes remain stable, but the process of reaching those outcomes has become slower, more selective, and more negotiation driven.”

Across Colorado, local markets continue to reflect their own unique dynamics, but a common theme has emerged: buyers have adjusted to today’s financing environment, sellers are becoming more realistic about pricing and concessions, and well-prepared homes continue to attract strong interest.

“Buyers have largely accepted that mortgage rates around the mid-6% range may be the new normal. Rather than waiting indefinitely for rates to fall, many are moving forward with purchases, recognizing they can refinance later if rates improve,” said Grand County-Area REALTOR® Monica Graves.

Rather than the urgency that defined recent years, this summer’s market is being driven by informed buyers, strategic sellers, and realistic expectations.

“While spring and early summer typically bring increased activity, this year’s market feels less like a surge and more like a return to balance. Buyers appear to be adjusting to today’s financing environment, while sellers are becoming more strategic with pricing and concessions,” said Evergreen-area REALTOR® Julia Purrington Paluck. “At the same time, lenders continue introducing financing options that help bridge affordability challenges. Rather than waiting for perfect conditions, buyers and sellers are increasingly finding ways to make transactions work.”

Total Market Overview – Seven-County Denver Metro

Total Market Overview – Statewide

Taking a more in-depth look at some of the state’s local market data and conditions, the Colorado Association of REALTORS® Market Trends spokespersons provided the following assessments:

AURORA

“June and July are typically slower months in the world of real estate sales. It seems that many buyers leave for vacation. Hopefully, they come back soon. The numbers for Aurora, Centennial, Adams County and Arapahoe County sales and sold prices are relatively the same as last month and all the numbers are down slightly from last year. Days on the market are on average 36 days for the same Aurora, Centennial, Adams and Arapahoe counties. The median price in Aurora is $515,000, Adams County median price is $520,000 and Arapahoe County median price is $590,000. The prices are only up or down 1% from 1 year ago. Inventory is down and it seems that many sellers are staying in place. Perhaps they do not want to give up their 3% interest rate or maybe, they just are uncertain as to where to go for the next home. The number of sold properties are down over 1 year ago. That stands to reason given that the number of listings are down from 2025.

“Condos and townhomes are still a very attractive market for home purchasers. The challenge is finding properties where the HOA fees fit within the buyers’ home buying budget. For now, buyers have choices and sellers need to be prepared that many buyers may have many choices.

“For homes that are priced correctly and in pristine condition, sellers are faring much better on the offers they receive,” said Aurora REALTOR® Sunny Banka.

BOULDER/BROOMFIELD COUNTIES

“The typical late-summer slowdown arrived ahead of schedule in Boulder and Broomfield counties this year. Instead of the busy summer market many expected, buyers appear to have checked out early, leaving showings sparse during what is normally one of the busiest times of the year.

“Even with proactive price reductions and beautifully staged homes, activity has remained surprisingly quiet. Home prices in both counties are essentially flat, showing no appreciation since the beginning of the year.

“For sellers who do attract a buyer, homes continue to move at a measured pace. In Boulder County, the average home sells in 64 days, while Broomfield remains somewhat stronger at 46 days on market.

The condo and townhome market continues to face the biggest headwinds. Prices are down 15% in Boulder County and 3% in Broomfield, with rising HOA dues continuing to affect buyer demand.

There are still occasional bursts of excitement when a well-priced new listing hits the market, but they have become the exception rather than the rule. Overall, the market remains sluggish and is expected to stay that way through the remainder of the summer.

“For buyers, however, this may be the opportunity they’ve been waiting for. With motivated sellers, more negotiating power, and little upward pressure on prices, this summer’s real estate slowdown could create some of the best buying conditions we’ve seen in quite some time,” said Boulder/Broomfield-area REALTOR® Kelly Moye.

COLORADO SPRINGS

“A slight cooling for June occurred as we continue our summer selling season. We pulled back slightly on total active properties, down by 2.4% and added a slight increase on properties sold year over year, up 3.8%. Our median price had a slight easing, down .5%. If we just look at single family residences, median price was down 1.5%. June added days on market, up 15.8% for single family homes.

“Nationally similar statistics were seen with overall inventory in June, but prices nationwide pushed up. We are currently sitting at 4.5 months of inventory nationwide. However, a record number of homes delisted going back to April. Delisted homes were up 5.8%, the highest number since the pandemic. Buyer demand falls and more listings continue to stack onto the market, then more sellers realize they cannot sell and pull their homes back off the market.

“Locally we continue to see a slower market when actively showing our buyers homes. Some homes get better activity than others, but overall REALTOR® sentiment shows it is a hard market. Buyers continue to be on the sidelines, and sellers do appear to understand this. Most sellers are prepared to accept concessions as part of an offer. Searches in the MLS continue to show short sales, corporate sales and distressed sales entering the market, although not an alarming rate. Interest rates continue to be elevated for home prices, and many potential buyers have simply settled to rent, saving money at this time,” said Colorado Springs-area REALTOR® Patrick Muldoon.

COLORADO SPRINGS

“This month, there are no eye-catching headlines to report regarding the relatively stable single family/patio homes housing market in Colorado Springs. Year-over-year changes are marginal. Active listings have decreased by just 0.4%, while sales have increased slightly by 1.6%. The year-to-date sales volume shows a minimal increase of 0.6%. The median sale price remains unchanged at 0.0%, while the average sale price has risen by a modest 1.2%. The monthly sales volume increased by a moderate 4.0%.

“These conditions offer great opportunities for both buyers and sellers to buy and sell, with realistic expectations and fair dealings. Homes listed at fair market value are selling quickly. However, it is essential to maintain high inventory levels to prevent a spike in home prices, as this could discourage buyers amid ongoing affordability challenges.

Key Data Points in June 2026 for single family/patio homes:

- Active Listings – Supply: 4,039 homes, compared to 4,055 last year (down 0.4% YOY) and 3,667 in May (up 10.1% MOM).

- Sales – Demand: 1,229 homes compared to 1,197 last year (up 2.7% YOY) and 1,251 in May (down 1.8% MOM).

- Average Price: $577,638 compared to $570,516 last year (up 1.2% YOY) and $577,202 in May (up 0.1% YOY).

- Median Price: $499,900 compared to $500,000 last year (0.0% YOY) and $499,952 in May (0.0% MOM).

- Sales Volume: $709,917,713 compared to $682,908,768 (up 4.0% YOY) and $722,042,516 in May (down 1.7% MOM).

- Days on the Market (DOM): 45 days compared to 40 days last year and 43 days in May.

The current supply of homes is reasonably good across all price ranges. Overall, the supply of single-family and patio homes stands at 3.3 months. Breakdown of the supply by price tier:

- Homes priced under $400,000 have a supply of 3 months,

- Homes priced between $400,000 and $600,000 have a supply of 3.2 months,

- Homes priced between $600,000 and $1 million have a supply of 3.6 months,

- Homes priced over $1 million have a 5.3-month supply.

Looking at the sales by price tier:

- Homes priced under $400,000 accounted for 24.9% (up 3.9% YOY),

- Homes priced between $400,000 and $600,000 represented 41.0% of all sales (down 12.2% YOY).

- Homes priced between $600,000 and $1 million made up 27.2% (up 14.4% YOY).

- Luxury homes priced above $1 million comprised 6.9% (up 19.7% YOY).

Price Reductions: In the current competitive market, 50.7% of active listings in El Paso County and 37.8% in Teller County had price reductions in June. To achieve the highest possible sale price in the shortest time and avoid multiple price cuts, sellers ought to price their properties realistically from the start. Additionally, properties need to be well-maintained and show attractively to draw and wow potential buyers,” said Colorado Springs-area REALTOR® Jay Gupta.

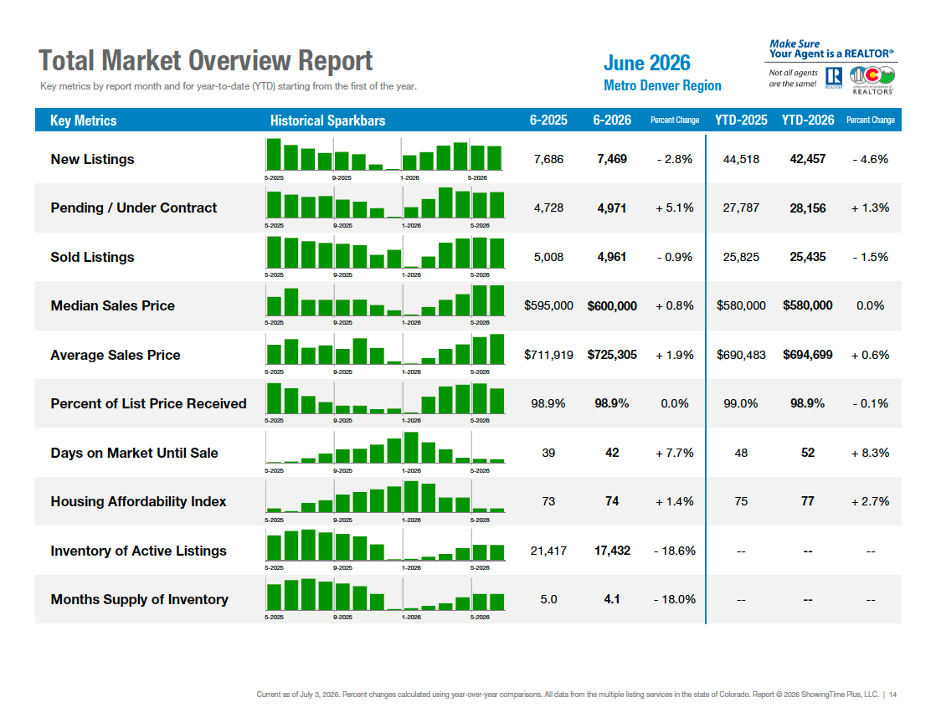

DENVER METRO (Seven County)

“Halfway through 2026, stability remains the headline for the Denver Metro housing market, but the mechanics underneath it have changed. June ended with 17,432 active listings, down 18.6% from last year and much closer to the inventory levels seen in 2024 than the elevated supply of 2025. New listings declined 2.8% year over year, while pending contracts increased 5.1%. Ordinarily, fewer homes coming to market and more homes going under contract would point toward stronger seller leverage. Instead, closed sales remained nearly flat, homes took 7.7% longer to sell, and sellers received the same 98.9% of list price as last June. There are fewer homes available, but there has been no return to urgency.

“The single-family market is where constrained inventory is having the clearest effect. Active listings fell 21.1% year over year to 12,088, reducing supply from 4.6 months to 3.6 months. At the same time, pending contracts rose 5.6%, the median sale price increased 1.6% to $650,000, and the average sale price rose 2.5% to $792,284. In the face of elevated mortgage payments and persistent affordability challenges, limited supply is helping prevent meaningful downward pressure on single-family values. That does not make this a uniformly strong seller’s market, however. Single-family homes still averaged 39 days on market, up 8.3% from last year, and the typical seller received the same percentage of list price as a year ago.

“The attached market is following a materially different path. Condos and townhomes carried 6.2 months of inventory in June and took an average of 55 days to sell. The median sale price declined 1.3% year over year to $395,000 and is now roughly 10% below the segment’s 2022 peak. Year to date, attached sales are down 7.6%, pending contracts are down 3.9%, and the median price is down 1.2%. Rather than simply holding flat, this segment appears to be moving through a gradual price correction as buyers account for the full monthly cost of ownership, including mortgage payments, HOA dues, insurance, taxes, and maintenance. June did provide a modestly better signal, with pending contracts up 3.5% and closed sales up 1.4%, suggesting that demand may be finding better footing as prices adjust.

“The broader takeaway is that lower inventory does not automatically create a seller’s market. Denver is operating with substantially fewer listings than it had last summer, yet homes are still taking longer to sell. June days on market have increased in each of the last four years, from 30 days in 2023 to 34 in 2024, 39 in 2025, and 42 this year. The market’s outcomes remain stable, but the process of reaching those outcomes has become slower, more selective, and more negotiation driven. Buyers are still participating, particularly where value is clear, but they are not responding to limited supply with the urgency seen in prior cycles. For sellers, pricing and presentation remain decisive. For buyers, the market continues to offer time and negotiating room, even without the inventory levels available a year ago,” said Denver County-area REALTOR® Cooper Thayer.

DURANGO/LA PLATA COUNTY

“For four months, Durango and La Plata County single-family sales have outpaced 2025. In June, sales were 55% up in number over June 2025, and new listings coming on the market were +15% in number year over year. With the traditional closing period of approximately 30 days, Buyers were busy choosing homes in May for these June sales.

“Pending single-family inventory, however, is down significantly in June, -13.5% from June 2025 and similar to June 2024. These lower pending numbers today will mean lower sales numbers in August. It is not uncommon for this to happen in a year where there was no snow. Listings came on the market earlier; therefore, buyers were active in our warm early spring weather. These earlier-year sales are ‘borrowed’ from those that would happen later in a heavier snow year.

“If you combine both single-family and condo/townhome inventory, La Plata County has in total 11% more active listings, and sold listings are up 22% year to date over 2025.

“The rise in inventory of condos and townhomes is significantly higher than in the past two years because of a surge of new listings in May. There were fewer sold condos/townhomes in June YOY June, but the number is up 20% year to date.

“Single-family inventory is 7% higher than in June 2025, but to put it in perspective, there are still 200 fewer single-family homes on the market than what existed pre-COVID. Active inventory of condos/townhomes is back to pre-COVID levels.

“Breaking down the regions in the county, 90% more Durango in-town homes came on the market in June 2026 compared to June 2025, currently totaling +10% in new listings for the year. June had 86% more sales year over year. Condo and townhome closings were quiet in June but still remain 15% higher year to date.

- Rural Durango is where we saw a significant bump in sales both in June and May over what we saw in 2025. June had 121% more sales year over year (31 sales vs 14). This region has seen a 54% increase in year-to-date sales. The median price here has remained where it was in 2025, just 1.9% over the median in June 2025.

- The town of Bayfield is growing, and the sales are increasing. Of note, the median sold home in June was just $399,500.

- Rural Bayfield was down in sales with 31% fewer sold homes year over year, and -13% fewer for the year. The median is $670,000, and there are 8.4 months of active inventory of homes for sale-a clear buyer’s market.

- Rural Ignacio had a bump of new listings coming on the market and has reached a 10.6 months’ supply of inventory.

- The resort area near Purgatory Resort single-family sales are up 80% over 2025 with newly constructed homes to choose from. Condos and townhomes have reached a 15-month supply, and sales were steady compared to June 2025.

“La Plata County can often have busy autumn selling seasons, but we are at least in a cooling-off period for the next month,” said Durango-area REALTOR® Heather Erb.

EVERGREEN/MOUNTAIN METRO

“The Colorado foothills housing market settled into a healthy summer rhythm in June, reflecting what many REALTORS® have been observing on the ground for the past several months. Activity remains steady, buyers are engaged, and well-positioned homes continue to sell, but today’s market rewards preparation, realistic pricing, and thoughtful marketing more than it has in recent years.

“While spring and early summer typically bring increased activity, this year’s market feels less like a surge and more like a return to balance. Buyers appear to be adjusting to today’s financing environment, while sellers are becoming more strategic with pricing and concessions. At the same time, lenders continue introducing financing options that help bridge affordability challenges. Rather than waiting for perfect conditions, buyers and sellers are increasingly finding ways to make transactions work.

“Across the Colorado foothills, inventory is holding steady near its highest in over 10 years, while pending contracts and closed sales remained remarkably stable. Median single-family prices increased 3.1% year over year to $726,000, demonstrating continued pricing resilience even as buyers remain selective. Days on market increased to 35 days (a 9% increase year-over-year), reflecting a more deliberate pace than the frenzied conditions of several years ago, but still indicating a healthy level of demand.

“One of the more encouraging trends is that today’s market appears increasingly driven by realistic expectations rather than urgency. Conversations with local agents suggest seller-paid concessions and temporary mortgage rate buydown programs continue to play a meaningful role in helping transactions reach the closing table. Rather than dramatically lowering asking prices, many sellers are choosing to improve affordability by contributing toward buyers’ financing costs, while lenders continue expanding creative loan options.

“Evergreen and Conifer continue to reflect the normalization taking place within the luxury segment of the market. June’s median sales price in the Evergreen/ Conifer market declined significantly from last year, while pending sales increased 25.6% and closed sales rose 22%, suggesting demand remains healthy but is increasingly concentrated in homes offering strong value through location, condition, and pricing. The ultra-luxury segment has become noticeably quieter, contributing to softer pricing at the upper end of the market, while well-positioned homes continue to move at a healthy pace, illustrating that today’s buyers remain active, but are far more deliberate than they were just a few years ago.

That selectivity is becoming one of the defining characteristics of today’s foothills market. Homes that are priced appropriately, updated, and located near community amenities continue to attract strong interest, while properties that miss the mark on price, condition, or location are often seeing fewer showings and longer marketing times. Buyers have more choices than they have had in several years, making overall value—not simply price—the deciding factor in many purchasing decisions.

“The Colorado foothills market is entering the second half of 2026 in a healthy and increasingly balanced position. Buyers have more options and greater negotiating power than they did during the peak seller’s market, while sellers who price strategically and present their homes well continue to find success. The pace may be more measured than in recent years, but the market is proving to be resilient, stable, and well-positioned for the remainder of the summer,” said Evergreen-area REALTOR® Julia Purrington Paluck.

FORT COLLINS

“The Fort Collins showed some signs of life in June, bouncing back a bit after an uncertain May. On one hand, there were many positives: days on market continued to improve, median home value is not escalating unchecked nor receding rapidly, and conditions are generally balanced between buyers and sellers – this creates opportunities on both sides of the transaction. On the other hand, the single-family market has strengthened over the last few months, where the attached market is struggling to find footing. Just another quirk as we enter the back half of the year, without obvious direction.

“The single-family market bounced back from a softer May. Sold listings were up 13.8% as compared to June 2025, even with 13% fewer actively available listings. New listings were down 4% from June 2025, and it appears those peaked back in March, so total inventory should begin to peak and regress in July. Median value was very strong, reaching $650,000, which is the highest median value we’ve seen in 2026. Days on market have slowly crept down to 62 days, and sales vs. list price ratios have crept up to 99.7%, proving buyer demand is healthy and competition for attractive, well-priced listings is strong.

The condo/townhome market tells a different story. To be fair, 2025 was a huge year for the attached market, so in almost every way, it is hard to make reasonable comparisons. New listings were down 19.3%, and active listings were down 13.3% from 2025 figures. It appears that instead of the mid-year peak in inventory, it’ll be a steadier plateau throughout the selling season. Median value held nominally still at $422,915, down just 1.3% from June 2025.

“Affordability is not improving in either market segment due to a combination of steady (or slightly improving) median values and increasing interest rates. Affordability will remain a concern until there is either more inventory, or lower rates and I am certain there will be nothing groundbreaking in either metric in the near future. For the remainder of the year, it is likely the market will continue to tread water, which is probably the best we can hope for,” said Fort Collins-area REALTOR® Jared Reimer.

GRAND COUNTY

“As summer arrived and visitors poured into the mountains of Grand County, activity naturally increased. Open houses were busy, vacation traffic translated into more showings, and many second-home buyers who had been watching the market decided it was time to act.

“One of the encouraging signs was that prices remained remarkably resilient. While appreciation has slowed, Grand County continues to hold its value because of limited developable land, strong recreational demand, and the enduring appeal of mountain living. The county’s long-term fundamentals remain healthy even as the pace of appreciation becomes more sustainable. Public housing data through late spring showed values stabilizing rather than accelerating, with inventory continuing to rise modestly. New construction in affordable housing is great for workers in these resort parts of Colorado. Presales of new construction, deed restricted units, are already happening in Granby Nuche Village, as well as St Louis Landing in Fraser.

Still, each community told a slightly different story.

Winter Park remained the county’s premium resort market. Luxury homes, ski properties, and high-end condominiums continued attracting buyers seeking lifestyle and investment opportunities. Demand stayed strongest for turnkey properties near the resort and downtown amenities. The median sales price for single-family was $1.29 million and condo/townhome was $697,500. Days on market went from an average of 73 days to 90.

Fraser benefited from buyers looking for slightly better value while remaining close to Winter Park. Families and full-time residents continued to drive demand, particularly for newer single-family homes and townhomes. Median single-family sales price $925,000 and condo/townhome was $500,000. Days on market 45-60 days.

Granby continued to attract buyers searching for more space and affordability. Golf course communities, Granby Ranch properties, and horse properties remained popular with buyers wanting year-round recreation at a lower price point than neighboring resort communities. More new construction being sold with 3.99% builder incentives. Single family median price $795K while condos/townhome was $599,000. Days on market slower than last year at 75, compared to 110.

Grand Lake entered its busiest season with strong interest from second-home buyers drawn to the lake lifestyle. Walkability to the historic village, lake access, and updated cabins remained some of the most desirable features in the marketplace. Median single-family sales price $755,000, and condo/townhomes at $452,000. Average 70 days on the market compared to 53 days in 2025.

“Perhaps the biggest shift wasn’t found in the statistics—it was in buyer psychology. Buyers have largely accepted that mortgage rates around the mid-6% range may be the new normal. Rather than waiting indefinitely for rates to fall, many are moving forward with purchases, recognizing they can refinance later if rates improve.

“For sellers, in Grand County, June reinforced an important lesson: today’s market rewards preparation. Professional photography, thoughtful staging, strategic pricing, and strong marketing make a measurable difference. Buyers are willing to pay for homes that are move-in ready, but they are increasingly unwilling to pay premium prices for properties needing deferred maintenance or major renovations.

“Overall, June 2026 was not a market defined by rapid appreciation or bidding wars. Instead, it reflected a maturing mountain market built on stability, choice, and realistic expectations. Grand County remains one of Colorado’s most desirable mountain destinations, and while the pace has become more measured, the long-term outlook continues to be supported by limited supply, exceptional lifestyle amenities, and consistent demand for mountain living,” said Grand County-area REALTOR® Monica Graves.

MESA COUNTY

“Mesa County saw an increase in new listings and properties going under contract, however, by the time of closing, sales compared to last year were down 16.7%. The properties that did close boosted the median price to $412,300, an increase of 3.1% and the average to $466,123. Total active listings are now 1,048, or approximately 4 months inventory based on recent sales. The greatest number of sales in the county are in the city of Grand Junction, North, and Fruita, followed by Northeast, Redlands, Orchard Mesa, and Southeast. Other areas had four or less sales. Prices ranged from $338,000-$780,000. Open houses are generating traffic if they are held when the temperatures are more moderate, as Mesa County is experiencing extreme heat with temperatures going over 100,” said Mesa County REALTOR® Ann Hayes.

PAGOSA SPRINGS

“Beautiful summer has arrived with higher day temperatures, yet 50 degree nights (Mother Nature’s air conditioning) providing everyone with summer activities as fishing, hiking, biking, golfing, horseback riding, town events, and morning and evenings on the deck or patio! The real estate market mimics summer temperatures with highs and lows. Highest YTD home inventory gains compared to 2025 are in home prices $700,000-999,000 (+20.3%) and $2 million-plus (+27.3%), explaining why that market price is unusually quiet, as high inventory gives buyers many homes to choose from. With more choices, the additional inventory didn’t negatively impact selling prices (nor did interest rates because of cash buyers) as savvy sellers in the luxury price point have worked to have their homes show ready, updates and in pristine condition, price adjustments, and more patience in home selling time periods. Inventory in the luxury home price point ($900,000+) is approaching 1.5 years, indicating sellers will need even more patience in selling or price adjustments and seller concessions to entice a buyer.

“Ongoing challenge facing the market is the lack of sufficient homes for sale (inventory) at or under the median sold price year-to-date at $611,000 (up 10.6% from 2025 at $552,500) as sales unit numbers are flat. The slowdown is this price point purchase is not happening because people no longer want to buy homes in this price point. Instead, the market is unevenly stuck because of the lack of homes with sellers staying in place and choosing NOT to sell, especially those spoiled with low interest rates. This creates fewer opportunities for median price buyers to complete a purchase. Typically homes in this price point also need updates that buyers are not willing to do (because of rural higher renovation costs) or have additional update funds. Higher monthly mortgages, cost of living expenses (gas, groceries, utilities) especially affect retirees and first-time buyers and their purchasing power.

“Overall, the June market overview carried positives in all categories, except days on market which were flat at 133 days (YTD 156 days). Pending sales at 39 were up 56% from this time last year due to early entry home inventory. However, YTD pending sales are up 8.9% at 184 homes. Sold listings are up only 4% at 156 homes. Active listings had smaller gains at 317 homes (+3.9%). Months’ supply of inventory is up at 10.5 months (more reflective on homes price above the Average Sales Price (YTD $725,770). List price received YTD (96.4%) is the same as this time last year and contributed to lower inventory in homes priced under the average sales price and higher inventory over the average sales price.

June Median Sold Price $560,000 (+8.7%) – YTD $611,000 (+10.6%)

June Average Sales Price $718,307 (+8.6%) – YTD $725,770 (+2.9%)

June Days on Market 123 (-4.7%) – YTD 133 (+0.8%)

“Oddly even with higher prices, the long-run home ownership demand is steadily working its way back to a normal market. However, affordability struggles and higher home prices will decide on who participates in home ownership. Clearly the Pagosa Springs peaceful rural lifestyle and especially second home ownership continue to drive the real estate market forward,” said Pagosa Springs-area REALTOR® Wen Saunders.

PUEBLO COUNTY

“The Pueblo County single-family housing market continues to show resilience despite a slower pace of activity. Compared to June 2025, new listings declined 19.9% to 289 homes, while sold listings dipped 7.7% to 167. Even with fewer homes changing hands, home values remain steady, with the median sales price increasing 1.3% year over year to $324,000 and the average sales price rising to $333,140. Homes are taking slightly longer to sell, averaging 96 days on the market, while sellers are receiving 97.6% of their most recent list price on average. Inventory also tightened, dropping 13.7% from last year to 843 active homes, resulting in 5.1 months of housing supply.

“Year-to-date, the market has remained relatively balanced, with new listings down 3.7%, sold listings essentially unchanged (+0.7%), and the median sales price at $305,000. Overall, Pueblo County remains a stable market where well-priced homes continue to attract buyers, offering opportunities for both buyers and sellers navigating today’s market conditions,” said Pueblo-area REALTOR® David Ramirez.

SAN LUIS VALLEY

“The San Luis Valley housing market continued to show encouraging activity in June 2025, with inventory remaining healthy across much of the region while pricing and sales trends varied by county. Alamosa County continued to lead the valley with strong momentum, more than doubling its number of homes sold compared to last June while median home prices increased to $335,000 and homes sold in less than half the time they did a year ago. Rio Grande County also posted another strong month, with new listings up more than 42% year over year and median home prices climbing over 22% for the month and 24% year-to-date. Saguache County continued to provide buyers with abundant inventory and faster sales despite lower prices, while Costilla County saw an increase in new listings and sellers receiving an average of 100% of their asking price on homes that sold. Conejos County remained a low-volume market where just a few transactions significantly influenced monthly statistics, with sellers averaging 112.1% of list price, demonstrating continued demand for well-priced properties. Mineral County also experienced slower sales activity but continued to see growing inventory and an increase in new listings compared to last year.

“Overall, the June market highlights that while conditions continue to vary from county to county, buyers are benefiting from increased inventory and sellers who price and market their homes strategically continue to achieve strong results. As the summer selling season continues, local market knowledge remains essential, making it more important than ever for buyers and sellers to understand the unique conditions within each San Luis Valley community before making a move,” said San Luis Valley-area REALTOR® Megan Bello.

STEAMBOAT SPRINGS/ROUTT COUNTY

“Hard to believe we are already half-way through 2026! The Steamboat single-family market received 40 new listings bringing the YTD total to 148 – now just two more than last year. Sales are slightly above last year with 52 closings compared to 49; however, the story for June is that Buyers reacted quickly to new inventory and for the 15 homes that sold the average days on market until a sale was 24 compared to 92 in June of 2025. There are 118 homes for sale ranging from $649,000 in Milner to a newer $24.9M 144-acre ranch with an 8619 square foot home; the median list price is $3,350,000.

“Multi-family sales were well represented by ten closings at The Cottonwoods Condominiums, a new Yampa Valley Housing Authority development with income & deed restrictions, as well as an appreciation cap. These units were sold via a lottery for local residents and represent entry level housing, while the highest multi-family sale was a slopeside 1973 Storm Meadow condo that had been extensively remodeled inside and out for $6M. The median sales price for June was $912,000.

“The Oak Creek/Stagecoach communities continue to sell more homes than in 2025 with fewer new listings coming on the market. Median sales price remains at $980,000 while average sales price increased slightly from May to $1,433,735. Days on market until a sale also dropped slightly to 107 days and with 23 homes currently for sale, this represents approximately 7.5 months’ supply. There is limited multi-family development outside of Steamboat city limits. The number of sales has doubled for the year while new listings are equivalent to last year and 7 units for Buyers to choose from. Stagecoach is home to a State Park with a reservoir and the average sales price for a multi-family property is $450,780.

“To the west of Steamboat and home to the Yampa Valley Regional Airport, lies Hayden and location of the Amazon warehouse that is under construction. New listings remain at two more than last year. Five homes sold in June with a median price of $645,000; sales for the year are at 11 compared to 19. With 29 homes on the market ranging from $392,409 – $15M there is a lot of diversity with rate of sale slower and months’ supply of inventory now at 12.1. Multi-family activity in Hayden is similar to Oak Creek with limited inventory for sale and about 5 months to sell. Summer activity really kicks off in July and there has definitely been a buzz of activity,” said Steamboat Springs-area REALTOR® Marci Valicenti.

SUMMIT, PARK AND LAKE COUNTIES

“Across much of the country, June felt like someone left the oven door open. While many cities baked in temperatures near 100 degrees, Frisco’s warmest day reached a comfortable 77 degrees. It turns out buyers appreciate cool mountain air as much as they appreciate mountain views. Whether escaping the heat or making a long-planned investment, they helped drive residential sales across Summit and Park Counties up nearly 37% compared to last June.

Summit County – June 2026 compared to June 2025

Single Family Homes

- Number of Sales: Up 6.5%

- Average Price: $1,992,559, down 7.3% year over year, with a year-to-date average price of $2,445,024

- New Listings: Down 0.8%

Multi Family Homes

- Number of Sales: Up 45%

- Average Price: $1,228,939, up 44%, with a year-to-date average price of $1,012,167

- New Listings: Up 18%

Park County – June 2026 compared to June 2025

- Number of Sales: Down 14%

- Average Price: $679,014, up 10% year over year and 4% above the 2025 full year average

- New Listings: Down 15%

Lake County – June 2026

- Number of Sales: 12

- Average Price: $763,042

- Active Listings: 76

“Across Summit, Park, and Lake Counties, 1,135 residential listings are currently on the market, 24% more than last month, ranging from an $80,000 mobile home in Park County to a $25 million Breckenridge home. More than 44% of all active listings are priced above $1 million, including 60 properties over $5 million. The average residential list price across the region is $1,587,644.

In June, 146 residential properties closed, ranging from a $95,000 mobile home in Park County to a $5,000,000 home in Frisco. Approximately 56% of all sales closed above the $1 million mark, while 48% were cash purchases. Another 229 properties are currently under contract.

“As the mercury rises, so does appreciation for mountain living. Fortunately, in Summit County, the temperatures stay comfortable even when the market gets busy. Whether buyers are chasing cooler weather, spectacular scenery, or a long-term investment, June proved that Colorado’s high country remains one of the coolest places to own real estate—in more ways than one,” said Summit-area REALTOR® Dana Cottrell.

TELLURIDE/SAN MIGUEL COUNTY

“The real estate market in the Telluride region for June is demonstrating a very consistent trend. Through June, the overall dollar amount of sales is up 9% with the number of sales down 13%. Buyers are picky and seek very specific properties that meets their family’s needs and wants. I used to own three Hagen Daz ice cream stores. The most important thing is what flavor does the buyer want and how many scoops. Real estate buyers usually have in mind what they want before they look and how many bedrooms. Of course, location and views are important so that factor really dictates what sells too. My point is that buyers look for what fits with all of the above. While inventory is reasonable, there are a lot of flavors that just aren’t a popular as they used to be. Hence, buyers are still picky and might want strawberry rather than vanilla,” said Telluride-area REALTOR® George Harvey.

WELD COUNTY

“The Weld County real estate market continued to balance out in June, giving buyers and sellers more opportunities. Single-family home prices were down slightly from this time last year, with a median sales price of $499,000, while townhomes and condos had a median price of $359,950. Homes are taking a little longer to sell, but sellers are still receiving nearly their full asking price on average, showing that well-priced homes continue to attract strong buyers.

“For buyers, this means more inventory, more negotiating power, and increased opportunities for seller concessions. For sellers, success comes down to pricing your home correctly and presenting it well from the start. While the fast-paced market of the past few years has cooled, homes are still selling, and buyers are actively looking for the right property.

Overall, the Weld County market remains healthy and continues to offer opportunities on both sides of the transaction,” said Weld County-area REALTOR® Amy Tallent.

The Colorado Association of REALTORS® Monthly Market Statistical Reports are prepared by Showing Time, a leading showing software and market stats service provider to the residential real estate industry and are based upon data provided by Multiple Listing Services (MLS) in Colorado. The June 2026 reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. CAR’s Housing Affordability Index, a measure of how affordable a region’s housing is to its consumers, is based on interest rates, median sales prices and median income by county.

The complete reports cited in this press release, as well as county reports are available online at: https://www.coloradorealtors.com/market-trends/

###

CAR/SHOWING TIME RESEARCH METHODOLOGY

The Colorado Association of REALTORS® (CAR) Monthly Market Statistical Reports are prepared by Showing Time, a Minneapolis-based real estate technology company, and are based on data provided by Multiple Listing Services (MLS) in Colorado. These reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. Showing Time uses its extensive resources and experience to scrub and validate the data before producing these reports.

The benefits of using MLS data (rather than Assessor Data or other sources) are:

Accuracy and Timeliness – MLS data are managed and monitored carefully.

Richness – MLS data can be segmented

Comprehensiveness – No sampling is involved; all transactions are included.

Oversight and Governance – MLS providers are accountable for the integrity of their systems.

Trends and changes are reliable due to the large number of records used in each report.

Late entries and status changes are accounted for as the historic record is updated each quarter.

The Colorado Association of REALTORS® is the state’s largest real estate trade association representing over 23,000 members statewide. The association supports private property rights, equal housing opportunities and is the “Voice of Real Estate” in Colorado. For more information, visit https://www.coloradorealtors.com.