Colorado housing markets continue shift toward balance as buyers gain options

Pending sales rise statewide despite fewer new listings – stable prices and growing inventory signal a more sustainable market environment heading into summer

ENGLEWOOD, CO – Colorado’s housing market continues its steady transition toward a more balanced and sustainable environment heading into the summer months, according to the latest Market Trends Housing Report from the Colorado Association of REALTORS® (CAR).

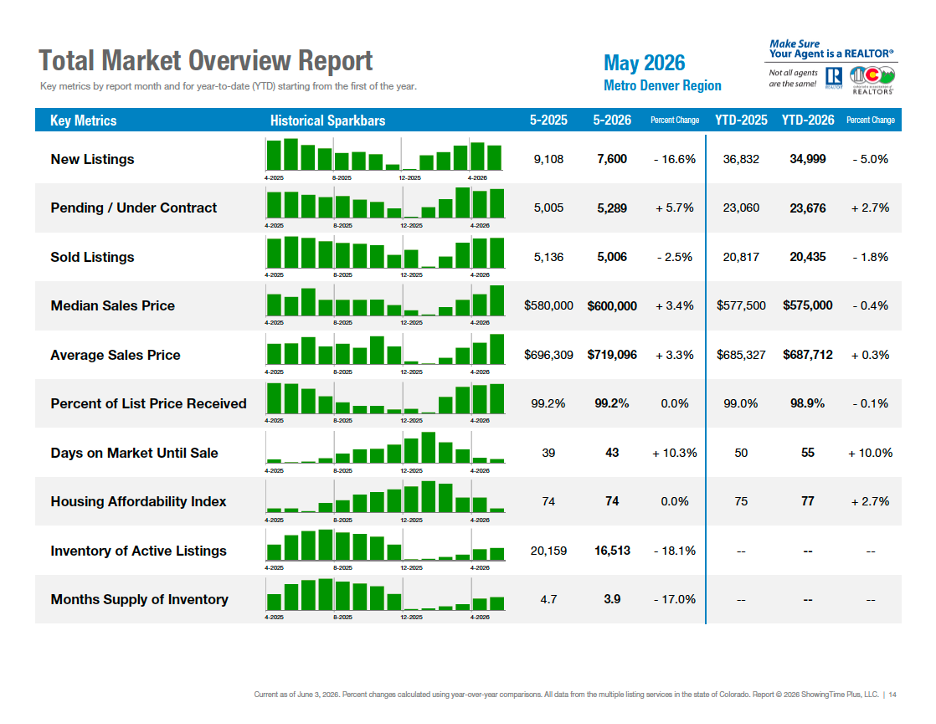

The seven-county Denver-metro housing market is showing its resilience with buyer demand remaining steady despite a slower pace. Through May, new listings were down 5% year-over-year, while sold listings declined just 1.8%. Pending contracts increased 2.7%, signaling that buyers remain engaged, though more selective. Homes are taking longer to sell, with average days on market up 10% year-to-date.

Home prices have remained stable, with the median sale price at $575,000, down only 0.4% from last year. Buyers appear to have adjusted to mortgage rates above 6%, while Colorado’s persistent housing shortage continues to support values.

Inventory remains constrained, with active listings down 18.1% from a year ago and months’ supply falling from 4.7 to 3.9 months. As a result, the market remains balanced but selective. Well-priced, move-in-ready homes continue to attract buyers, while overpriced listings face longer timelines and increased negotiation. Overall, Denver’s market is neither booming nor declining, but maintaining a steady, stable course.

“The bottom line – Denver metro is not racing nor crashing, it is proving resilient and steady,” said Denver-area REALTOR® Cooper Thayer. “For sellers, the opportunity is still there, but pricing discipline and strategic planning are critical. For buyers, the market offers more breathing room than it did a few years ago, but waiting for a major price reset may continue to be a frustrating strategy.”

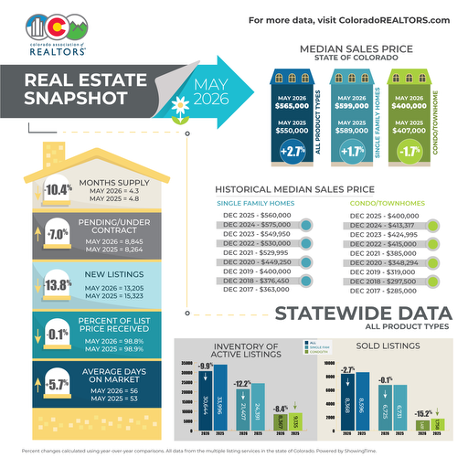

Looking statewide, housing markets continue to move toward balance as buyers gain more choices while demand remains steady. New listings declined nearly 14% compared to May 2025, but pending sales increased 7%, indicating that motivated buyers are still active despite affordability challenges.

Closed sales were down slightly, while median and average sales prices rose 2.7% and 3.3%, respectively. Homes are taking longer to sell, with average days on market increasing to 56 days. Inventory remains significantly healthier than the historically low levels of recent years, with 4.3 months of supply statewide.

Sellers are facing more competition and must price strategically, while buyers see benefit from selection and negotiating power. Overall, the market reflects normalization, with stable pricing, improving affordability and steady buyer activity providing a more sustainable housing environment across the state.

Total Market Overview – Seven-County Denver Metro

Total Market Overview – Statewide

Colorado Housing Markets Snapshot – May 2026

Based on analysis from REALTORS® working in markets across the state

(for a more in-depth analysis by market, see full content in report):

Aurora – The Aurora, Adams, and Arapahoe County housing market remains slow but steady. Listings are slightly up month-over-month in Aurora, though sales have declined compared to last year, while home prices remain stable. Centennial continues to see limited inventory, with prices up 4% year-over-year despite fewer listings. Across most zip codes, low inventory has contributed to fewer sales, but prices have largely held steady with modest gains in some areas. Townhomes and condos remain affordable options, and while inventory is constrained, buyers still have choices and sellers of well-priced, well-maintained homes can expect strong interest.

Boulder and Broomfield counties – Boulder and Broomfield county markets continue to move forward at a measured pace, showing little of the momentum typically associated with the spring and early summer selling season. While activity remains steady, market conditions point to a continued correction characterized by longer marketing times, softer pricing, and increased buyer caution. Current conditions represent one of the slowest spring and early summer markets experienced in recent years, with buyers benefiting from greater negotiating power and sellers facing increased competition.

Colorado Springs – In the current competitive market, 44.2% of active listings in El Paso County and 37.6% in Teller County saw price reductions in May. We had a little bit of stabilization in May across the front range as sold listings increased 8% year-over-year, added slight value (0.8%) to the median sales price, and active listings dropped 2%. To avoid multiple price cuts, sellers must price their properties competitively from the beginning. Furthermore, properties must be well-maintained and attractive to wow potential buyers.

Crested Butte/Gunnison – The Gunnison-Crested Butte real estate market remains much like 2025 with sales activity and overall inventory holding steady. As is typical for this time of year, new listings are arriving at their strongest pace, giving buyers more single-family homes and condos to choose from than last year. While inventory levels are similar overall, we are optimistic that a greater number of well-priced, well-appointed, and well-located properties will enter the market this summer, encouraging buyers to move from the sidelines and make purchasing decisions.

Denver Metro – May brought a fairly clear message for the Denver metro housing market: demand is holding, but the market is moving at a more deliberate pace. Year-to-date, new listings are down 5% compared to last year, while sold listings are down just 1.8%. Pending contracts are up 2.7%, which is the cleaner read on buyer engagement. Buyers are still active, just selective, and homes are taking longer to find the right buyer, with average days on market up 10% year-to-date.

Durango/LaPlata County – For the third month in a row, Durango and La Plata County single-family sales surpassed year-over-year sales, reaching 40% in May. While last month’s sales were attributed to a higher amount of inventory available to purchase, May’s buyer demand far exceeded the new listings on the market, which were down 31% from May 2025. Durango in-town condos/townhomes had a flurry of new listings, up 93% over last May. Rural Durango single-family home sales are up 42% over year-to-date compared to 2025.

Evergreen/Foothills – The Foothills housing market continues its transition toward a more balanced environment, with buyers enjoying the greatest selection of homes in more than a decade. Inventory in Evergreen and Conifer has steadily rebuilt, while demand remains resilient, with year-to-date sales up more than 10% and showing activity remaining strong. Median prices have remained relatively stable near $700,000, though homes are taking longer to sell. Buyers have more negotiating power, while sellers are finding that pricing, condition, and presentation matter more than ever.

Fort Collins – May is typically the strongest indicator of the direction of the real estate market for the remainder of the year and over this past month, the direction was clear – we’re likely not going to have a groundbreaking 2026. There is plenty of energy in the market however, in a month where new listings should bring on the upper limit of inventory, that just has not transpired. So far, 2026 is looking a lot like a two-step forward, two-step back kind of year.

Grand County – May 2026 felt like the market finally woke up from winter. Buyers who had been watching from the sidelines over the past year began re-entering the market but did so cautiously and with more negotiating power than they had during the last few years. Sellers, meanwhile, faced a different reality: competition. Inventory continues to build across Grand County, giving buyers more choices than they’ve seen in years. Grand County’s market found its footing—more inventory, more buyer choice, steady demand, and a return to a balanced mountain real estate market.

Mesa County – Mesa County’s housing market continues to face headwinds, with year-to-date pending sales down 11% and closed sales down 13%, while new listings remain essentially flat. Prices have held steady, but price reductions and seller concessions are becoming more common as buyers take advantage of increased negotiating power. Average days on market has risen to 106, giving buyers more time to evaluate options, though higher interest rates remain a challenge. Looking ahead, the market will be watching for additional inventory in key price ranges, while outlying communities such as Glade Park, De Beque, Collbran/Mesa, and Whitewater have recently shown stronger activity than the Grand Junction core market.

Pagosa Springs – May felt like the market finally woke up from winter. Buyers who had been watching from the sidelines over the past year began re-entering the market but did so cautiously and with more negotiating power than they had during the last few years. Sellers, meanwhile, faced a different reality: competition. Inventory continues to build across Grand County, giving buyers more choices than they’ve seen in years.

Pueblo County – Pueblo County’s single-family market is showing signs of normalization. Inventory remains somewhat limited, homes are selling faster, but buyers are being more cautious and price-sensitive than they were a year ago. Sellers can still succeed, but the days of throwing a ‘For Sale’ sign in the yard and waiting for offers to magically appear before dinner are mostly behind us. For buyers, there may be a little less competition than in previous years, but don’t mistake that for a clearance sale. Well-maintained, appropriately priced homes are still attracting attention,”

San Luis Valley – Although market activity varies from county to county, the overall San Luis Valley real estate market continues to demonstrate stability and resilience. Increased inventory, steady sales activity, and the region’s affordability compared to many Colorado mountain and Front Range markets continue to attract buyers seeking primary residences, second homes, investment opportunities, and recreational properties. As we move into the summer selling season, local market data suggests the Valley remains well-positioned for continued real estate activity throughout 2026.

Steamboat Springs/Routt County – Steamboat Springs entered 2026 with fewer new listings, down 4.5% for single-family homes and 21.9% for multi-family properties, though overall inventory remains higher than last year. Single-family sales were stronger in May, but homes are taking longer to sell, with year-to-date days on market averaging 90. Oak Creek and Stagecoach continue to outperform last year’s sales pace, while Hayden remains the softest market with elevated inventory. As summer progresses, buyers are expected to remain selective, rewarding sellers who price competitively and present their properties well.

Summit, Lake, and Park counties – As we head into the heart of the summer selling season, the market appears balanced between opportunity and caution. Inventory remains well above the extremely limited levels seen during the pandemic years, giving buyers more options and negotiating power, while continued strength in pricing demonstrates that demand for mountain living remains firmly intact. The growing number of pending sales suggests that many buyers are still moving forward despite economic uncertainty, setting the stage for what could be an active and healthy summer market across Summit, Park, and Lake counties.

Telluride – May sales were off significantly with the number of sales at 25 and the dollar amount of sales coming in at $62.71 million. This puts the first five months of sales in the Telluride regional market at $330.14 million over 159 transactions – up 4% from 2025 in pricing although the number of sales were down 11% for the same period of time in 2025. The current market is less about a rising tide lifting up every property, but more about a smaller pool of affluent buyers competing for their dream property.

Weld County –Weld County is continuing to shift into a more balanced pace as we head into summer. New listings down 15.9% year-over-year, and sales fell 22% for the month, showing a slower, more cautious buyer pool. Home prices have softened slightly, with the median price at $504,995 (down 2.8%), but values remain relatively stable overall. Homes are taking longer to sell, averaging 77 days on market, yet still getting offers at 99.3% of list price when homes are priced well. Inventory is limited at 2.9 months’ supply, keeping conditions fairly competitive, though far less intense than previous years.

Taking a more in-depth look at some of the state’s local market data and conditions, the Colorado Association of REALTORS® Market Trends spokespersons provided the following assessments:

AURORA

“For Aurora, Adams, and Arapahoe counties, the best way to describe the market is slow but steady. In Aurora, listings are up very slightly month-over-month with total single-family listings at 875 and solds at 375 down 15% from a year ago and month-over-month. The $525,000 median price is up just slightly from 2026. Centennial’s listings are down year-over-year however, they are up slightly month-over-month. Centennial boasts a median price of $725,000 up 4% over May 2025. Inventory in Centennial is down 23% from a year ago.

“Most zip codes show a lack of inventory, so it stands to reason that the number of sold listings would also be down, which is true across most zip codes. Prices are holding steady. There have been no drastic price swings either up or down for most areas. We’re seeing a modest, year-over-year price increase in a few areas.

“Townhomes and condos continue to be the best price secret out in the market. Aurora’s 80013 zip code has a median condo/townhome price of $340,000 and in 80015, the median price is $380,000. They are often a good value for someone not wishing to maintain a yard.

“Overall, despite the inventory numbers being down, there still seems to be plenty of listings available. For sellers, the well-kept, well-priced property will find a buyer, even multiple offers possibly. For buyers, there are numerous choices and sellers are realizing they need to be more creative with their offerings,” said Aurora REALTOR® Sunny Banka.

BOULDER/BROOMFIELD COUNTIES

“The residential real estate markets in Boulder and Broomfield counties continue to move forward at a measured pace, showing little of the momentum typically associated with the spring and early summer selling season. While activity remains steady, market conditions point to a continued correction characterized by longer marketing times, softer pricing, and increased buyer caution.

“In Boulder County, new listings have declined 11% compared to the same period last year. Home prices have largely held steady since the beginning of 2026, but median sale prices are approximately 5% below where they were one year ago. Properties are still taking about 60 days to sell, but those are listings that are priced competitively and show perfectly.

“The condo and townhome segment continues to face the greatest challenges. New condo listings are down 19%, sales have declined 17%, and prices have fallen 5% year-over-year. In many cases, condominium listings are expiring before securing a buyer, highlighting ongoing demand challenges.

“In neighboring Broomfield County, inventory levels are moving in the opposite direction, with new listings increasing 8%. Despite the additional supply, prices have continued to soften, declining 3.7% since the beginning of the year. The increase in available inventory has provided buyers with more options while placing additional pressure on sellers to price accurately from the outset.

“Across both counties, the market continues to adjust. Current conditions represent one of the slowest spring and early summer markets experienced in recent years, with buyers benefiting from greater negotiating power and sellers facing increased competition.

“As the market continues to normalize, realistic pricing and patience is the name of the game. Sellers who align their expectations with current market conditions and present their homes effectively are achieving results, while buyers are finding opportunities that were scarce during the highly competitive markets of previous years,” said Boulder/Broomfield-area REALTOR® Kelly Moye.

COLORADO SPRINGS

“We had a little bit of stabilization in May across the front range as sold listings increased 8% year-over-year, added slight value (0.8%) to the median sales price, and watched active listings drop 2%. I believed that we would see an increase in listings in May however, the drop shocked me a little bit. It seems that the market is balanced but it really depends on the price and home. We continue to see some homes sit while others get multiple offers. Some buyers are very committed; many are headed back to renting. Pending sales were up though, and it seems that May saw a bump.

“We continue to see distressed sales in many areas. Either short sale, bank foreclosures, or corporate sales enter the market, but not at alarming rates. It is an interesting dynamic to see play out. A listing may get competing offers; the home down the street exceeds average days on market, and two streets over a short sale. This bi-polar market also plays out with both buyers and sellers. A seller is motivated and price drops, and another one thinks their home is worth more than it is. A buyer competes to get their next home, other heads back to renting. A lot of emotions and strife. You must traverse a gauntlet to get a home to the closing table.

“As a whole, Colorado has seen a shift from being a high appreciation state to one of the fastest falling markets with Denver metro leading that trend. But we typically follow the trend 6-8 months later in the Pikes Peak region. Something to look for while we move through the year. Colorado is also seeing a notable increase in mortgage delinquency growth, ranking among one of the top in the nation. Increased property taxes, escrows, and overall costs are adding pressure to homeowners which adds to the confusion on what the market is doing and how a buyer or seller is working within those parameters. Overall, the economy – both in Colorado and across the nation – is showing signs of stress. Housing is the last to go after unemployment rises. Oil shock due to higher prices, AI beginning to affect jobs, and employers not trusting the future could begin to lead to that final blow. We are at a pivot point, and we can hope that unemployment does not begin to increase as we move into the 4th quarter of this year,” said Colorado Springs-area REALTOR® Patrick Muldoon.

COLORADO SPRINGS

“In May, while many areas across the nation saw a decline in the housing market due to rising interest rates, persistent inflation and the costly conflict in Iran, the Colorado Springs’ single-family housing market showed promising growth. There was an 11.3% increase in sales month-over-month and a 7.3% increase year-over-year. The monthly sales volume rose 15.2% from April to May and 11% compared to the same month last year.

“Additionally, the average home price appreciated 3.4% month-over-month and 1.9% year-over-year, while the median price up 4.2% month-over-month and 2% year-over-year. Notably, the number of days homes spent on the market decreased from 54 days in April to 43 days in May.

Key Data Points in May 2026:

- Active Listings – Supply: 3,667 homes compared to 3,671 last year and 3,422 in April.

- Sales – Demand: 1,251 homes compared to 1,166 last year and 1,124 in April.

- Average Price: $577,202 compared to $566,304 last year and $558,220 in April.

- Median Price: $499,952 compared to $490.,000 last year and $480,000 in April.

- Sales Volume: $722,042,516 compared to $650,311,583 last year and $627,025,373 in April.

- Days on the Market (DOM): 43 days compared to 41 days last year and 54 days in April.

“The supply of homes is currently modest across all price tiers. The overall supply of single-family and patio homes is at 2.9 months. Specifically, the supply is 2.6 months for homes priced under $400,000, 2.5 months for those priced between $400,000 and $600,000, 3.3 months for homes priced between $600,000 and $1 million, and 5.2 months for homes priced over $1 million.

“Homes priced between $400,000 and $600,000 accounted for nearly 47% of all sales, showing a 9.5% increase over the previous year. Properties priced under $400,000 accounted for 22.3% of transactions, while homes priced between $600,000 and $1 million accounted for 24.5%. Luxury homes priced above $1 million accounted for 6.4% of total sales, up 22.9% year-over-year.

“In the current competitive market, 44.2% of active listings in El Paso County and 37.6% in Teller County saw price reductions in May. To avoid multiple price cuts, sellers must price their properties competitively from the beginning. Furthermore, properties must be well-maintained and attractive to wow potential buyers,” said Colorado Springs-area REALTOR® Jay Gupta.

CRESTED BUTTE/GUNNISON

“The real estate market in the Gunnison Crested Butte area continues to be very similar to 2025 in terms of activity and the number of properties for sale. This time of year is when the most properties hit the market and that is certainly the case this year. While the total number of listings on the market is about the same as it was last year at this time, there are more single-family homes and condos available for a buyer’s consideration. We are hopeful that this summer will bring a better quality of listing to the market (well-priced, well-appointed, and well-located) and therefore buyers will be motivated to come off the bench to make a purchase.

“In the overall area, the number of sales is down slightly year-over-year (180 vs. 193 in 2025), but dollar volume is up ($177 million vs. $164 million). The number of residential sales is the same for each year with 132 sales through May, but dollar volume for those is also up ($155 million vs. $134 million). Average prices continue to go up as more luxury properties are selling.

“For the north end of the valley around Crested Butte, the tale is the same in terms of the number of sales for each year being equal (97), but an increased total dollar volume ($134 million vs. $118 million). The number of single-family home sales is also the same with 25 homes sold each year, but the average price has increased to $2,970,000 from $2,420,000. Condos and townhomes have seen increased activity with 47 sales this year vs. 41 in 2025 and over $10 million in increased dollar volume.

“The Gunnison area has seen a slight decline in average prices and overall activity. With 58 sales in 2026 vs. 67 in 2025, the total dollar volume is down almost $5 million from $37 million to $32 million. The number of single-family homes sold was the same for each year with 36 homes sold with only a slight decrease in dollar volume ($25 million vs. $25.8 million) and average prices ($693,722 vs. $717,513). Condos and townhomes continue to lag behind 2025 with only 12 sales this year vs. 19 last year at this time,” said Crested Butte-area REALTOR® Molly Eldridge.

DENVER METRO (Seven County)

“May brought a fairly clear message for the Denver metro housing market: demand is holding, but the market is moving at a more deliberate pace. Year-to-date, new listings are down 5% compared to last year, while sold listings are down just 1.8%. Pending contracts are up 2.7%, which is the cleaner read on buyer engagement. Buyers are still active, just selective, and homes are taking longer to find the right buyer, with average days on market up 10% year-to-date.

“Pricing has remained remarkably steady. The year-to-date median sale price is $575,000, down just 0.4% from last year, while the average sale price is up 0.3% to $687,712. That stability may seem surprising given higher mortgage rates, slower transaction volume, and ongoing affordability pressure, but two forces continue to support the market. First, buyers appear to be acclimating to 6%-plus mortgage rates. The shock of moving from roughly 3% rates to nearly 7% rates in 2022 caused a major pullback in demand, but four years later, many buyers seem to have accepted that ultra-low pandemic-era rates were the exception, not the rule. Second, Colorado still faces a deeper housing shortage. Even when monthly inventory feels higher than recent years, the broader reality remains that more people want to live here than we have homes to house them.

“That shortage is especially important for sellers this spring. Active inventory in May was 18.1% lower than the same month last year, and months’ supply fell from 4.7 months to 3.9 months. Sellers have less competition than they did a year ago, even though buyers still have more leverage than they had during the overheated market. The result is a balanced, but selective environment. Well-priced homes in good condition are still moving, while listings that miss the mark are taking longer and requiring more negotiation.

“The bottom line: Denver metro is not racing nor crashing; it is proving resilient and steady. Demand has adjusted to the current rate environment, prices are holding flat, and lower inventory is keeping the market from tipping significantly in buyers’ favor. For sellers, the opportunity is still there, but pricing discipline and strategic planning are critical. For buyers, the market offers more breathing room than it did a few years ago, but waiting for a major price reset may continue to be a frustrating strategy,” said Denver County-area REALTOR® Cooper Thayer.

DURANGO/LA PLATA COUNTY

“For the third month in a row, Durango and La Plata County single-family sales surpassed year-over-year sales, reaching 40% in May. While last month’s sales were attributed to a higher amount of inventory available to purchase, May’s buyer demand far exceeded the new listings on the market, which were down 31% from May 2025.

“Condo/townhome sales are holding steady compared with May 2025, but with a 35% increase in new listings coming on the market in May year-over-year, inventory is starting to rise. It seems as if our selling cycle in 2026 started earlier, and new listings coming on the market peaked earlier than in some years past. Buyer demand is strong. Pending sales rose sharply compared to May 2025; an increase of +30% for single-family homes and 24% for condo/townhomes will result in an uptick in sales for at least another month.

“Single-family inventory has shifted after months of steady increases, with 6.6% less homes on the market than in May 2025. Condo/townhomes are still coming on at a faster pace than last year, with a 35% increase in new listings for the month and 30% greater available inventory.

“Newsworthy regions of La Plata County in May were Durango in-town condos/townhomes which had a flurry of new listings, up 93% over last May. Rural Durango single-family home sales are up 42% over year-to-date compared to 2025.

“Both single-family and condo/townhomes in the Purgatory Resort and North County area had a strong May and 2026 year-to-date though inventory in this market has grown to where there is more than a year’s worth of active homes for sale.

“The median single-family home in-town Durango is currently $1,065,000, and in-town Bayfield is $584,900. The North County/Purgatory home median single-family home is $2,987,500, and the median condo/townhome is $597,500,” said Durango-area REALTOR® Heather Erb.

EVERGREEN/MOUNTAIN METRO

“As we’ve seen over the last year and several years of historically constrained inventory, the Foothills housing market continues its gradual transition toward a more balanced environment. May data shows buyers have more choices than they have seen in over a decade, while demand remains surprisingly resilient.

“Across the Mountain Metro Foothills region, active inventory remains elevated compared to recent years. At the same time, pending sales and closed transactions continue to outpace many expectations, suggesting that today’s market is characterized more by normalization than contraction.

“One of the most notable long-term trends is the steady rebuilding of inventory. Rolling 12-month inventory levels in both Evergreen and Conifer have reached their highest levels in more than 10 years. Evergreen averaged 176 active listings during the past year, while Conifer averaged 67. While those numbers represent a significant increase from the exceptionally tight inventory conditions of 2020 through 2022, they remain well below the levels experienced during the years following the Great Recession.

“Importantly, sales activity has remained stronger than many would expect. Rolling 12-month closed sales remain substantially higher than historical norms, with Evergreen recording nearly 490 annual sales and Conifer approaching 200. This suggests buyers continue to seek the foothills lifestyle and enter the market, even as higher mortgage rates and affordability concerns create additional challenges.

“Supporting that trend, showing activity throughout the foothills has remained healthy despite growing inventory levels. Buyers are actively viewing homes and engaging with the market, although they are taking more time to make decisions and are generally negotiating more aggressively than they did during the highly competitive markets of recent years.

“May statistics reflect this balancing trend. Across the foothills, single-family sold listings increased 5.4% year-over-year while pending sales rose 5.5%. New listings declined 22% compared to last May, helping moderate inventory growth after several years of expansion. The median single-family sales price remained essentially unchanged year-to-date at approximately $700,000, while days on market increased to 36 days, indicating buyers are taking more time to evaluate options and negotiate terms.

“Evergreen and Conifer continue to illustrate the market’s evolving dynamics. Year-to-date sales increased more than 10%, while inventory remained elevated and median prices softened modestly. Buyers are benefiting from increased selection and greater negotiating leverage, while sellers are finding that pricing strategy, property condition, and realistic expectations play a larger role than they did during the highly competitive markets of recent years.

“Local trends continue to mirror what we are seeing statewide. Pending sales have increased across Colorado, and distressed sales remain exceptionally rare, representing only 0.4% of all transactions. This reinforces that today’s market challenges are being driven primarily by affordability concerns, mortgage rates, insurance costs, and increased inventory rather than financial distress.

“As we move into the summer selling season, the key question will be whether buyer demand can continue to absorb the growing inventory base. Thus far, the data suggests a market that is steadily finding equilibrium. Buyers have more opportunities, sellers face more competition, and pricing remains relatively stable—a welcome return to the more balanced market conditions many industry professionals have been anticipating,” said Evergreen-area REALTOR® Julia Purrington Paluck.

FORT COLLINS

“May is typically the strongest indicator of the direction of the real estate market for the remainder of the year and over this past month, the direction was clear – we’re likely not going to have a groundbreaking 2026. There is plenty of energy in the market however, in a month where new listings should bring on the upper limit of inventory, that just has not transpired. So far, 2026 is looking a lot like a two-step forward, two-step back kind of year.

“The single-family market saw nearly 20% fewer new listings this last month compared to May 2025. It seems many potential home sellers are waiting on the sidelines for better conditions, or at least more market certainty when putting their homes up for sale. With fewer new listings, total active listings were down 14.6% compared to May 2025. There were 236 homes sold, down 4.8% from last May. A bright spot for homeowners is that the median sales price jumped to $637,500, likely due to the competition that comes when demand is higher than supply. Many of the move-up level homes (between $650,000 and $900,000) have been multiple offer scenarios with above list price bids. The real question will be, if the supply remains muted, will demand stay strong enough to prop up the market for the remainder of the year, or is the April-May-June demand our peak?

“The condo/townhome market in Fort Collins mirrored the single-family market, but at a higher magnitude. There were just 74 new listings in May, down 42% from May 2026. Homeowners in the attached market are holding tight and holding firm. Total active listings were down to just 159 listings, 36% below May 2025 levels. The lack of supply did not affect values with the median value for attached homes coming in at $395,000, down 1.3% from May 2025.

“Now, we hope that June is a bit of a bounce back month where both inventories show a bit of a pop, so eager (and even fatigued) buyers might get a break finding the right fit. Buyers need to know that while there is room for negotiation, depending on the segment of the market, there may be more competition than expected, and putting your best foot forward in a timely manner is the best approach. Sellers should take note: take the time to prepare your home expertly, do not rush to get to market. Time taken to prepare and present a turnkey, well-priced home will pay off with increased demand and traffic,” said Fort Collins-area REALTOR® Jared Reimer.

GRAND COUNTY

“As spring arrived in the mountains, May 2026 felt like the market finally woke up from winter. Buyers who had been watching from the sidelines over the past year began re-entering the market but did so cautiously and with more negotiating power than they had during the last few years. Sellers, meanwhile, faced a different reality: competition. Inventory continues to build across Grand County, giving buyers more choices than they’ve seen in years.

“In Winter Park and Fraser, the market remained the county’s most active segment. Resort buyers are still attracted to the area’s year-round recreation and proximity to Denver, but they are taking longer to make decisions. Well-priced properties moved, while homes that missed the mark on pricing tended to sit longer. Median single-family home sold price dropped to $925,000 while the median list price in Winter Park hit $1.2 million. Homes were averaging about 51 days on market.

“Granby continued to attract value-conscious buyers looking for larger homes, golf communities, and access to Granby Ranch. Activity remained healthy, but buyers were highly selective. Homes offering updated finishes, views, or short-term rental potential generated the strongest interest. The $709,000 median list price reflects all active inventory in Granby during the period and was down about 12% year-over-year. Properties averaged 78 days on the market.

“Grand Lake told a slightly different story. Lifestyle buyers remained drawn to lake access, boating, and the charm of the historic village. As summer approaches, interest in waterfront and vacation properties has increased, creating optimism among sellers. However, buyers are still expecting realistic pricing and are willing to wait for the right opportunity. Median list price is around $849,000 with median sold price $725,000. Homes are averaging 100 days on market.

“May 2026 was the month Grand County’s market found its footing—more inventory, more buyer choice, steady demand, and a return to a balanced mountain real estate market,” said Grand County-area REALTOR® Monica Graves.

MESA COUNTY

“Mesa County continues to struggle, whether you compare this May to last May, or 2026 year-to-date, the numbers are negative. Looking year-to-date, new listings are flat and pending and solds are down 11% and 13%, respectively. Prices are holding, but price reductions and concessions are becoming more common. The weather has been hot, in the 90s, and is projected to continue to stay high which does affect open house traffic. Average days on market is up to 106, which does give buyers more time, but higher interest rates are still a factor.

“Now that school is out and families go on vacation, it will be interesting to see which way the market goes and whether more inventory in the needed price ranges will be listed. Interestingly, the areas showing better activity this past month were all out of the main Grand Junction primary area in the Glade Park, De Beque, Collbran/Mesa, and Whitewater communities,” said Mesa County REALTOR® Ann Hayes.

PAGOSA SPRINGS

“The first five months of 2026 have been steady for buyers and sellers in the Pagosa Springs market. Year-to-date, new listings are up 10.5% as they enter the market earlier.

“Sellers are enticed to see median and average sales price increases. Year-to-date sold listings for May 2024, 2025, 2026 were exactly the same: 119 each year. More buyers (over the median and average sales price) and sellers (especially at or under the median and average price points) need to engage in the coming months.

- Median Sales Price up 6.1% at $610,000 ($575,080 in 2025)

- Average Sales Price up 4.2% at $754,378 ($723,939 in 2025)

- Days On Market up 2.3% at 136 (133 in 2025)

“Compared to 2025 and 2026, inventory gains were not seen in all price points, including those below (typically condo & manufactured homes) median home prices. The gains were in price points $700,000-$999,999 and $1 – 2 million. Currently, there are 285 homes for sale in Pagosa Springs (243 single-family and 42 Townhouse/Condo).

“With consideration, there are 85 homes on the market priced at $1 million and higher and only 19 have sold in the first five months and 14 are pending. Pending home sales is the leading indicator of sold listings within the next one to two months. However, with a total of 34 homes sold and pending in this price point, 51 homes await buyer interest and showings. Sellers in this price point will need patience, more time to sell (as homes are on the market longer), competitive pricing, a show-ready home, and creative marketing beyond normal to stand out from the large inventory. Meanwhile, buyers searching for a home under the median and average sale prices are waiting for inventory conditions to improve.

“Historically, June and July produce the most listings. However, this year, listings arrived earlier in April because of warmer temperatures and green grass versus melting snow. Sold listings increased 48% as buyers pounced on any new opportunity and listings with price adjustments. Financing homes with current interest rates creates hefty mortgage payments for home ownership. This is especially true for the first-time homebuyer competing with second-home buyers searching for lower home prices. Pagosa Springs has been a big second home market with attractive pricing compared to other Colorado resort communities. That is still true, however, second home buyers appear more discerning, especially when a mortgage is part of their home purchase scenario. Sales in the average to median price points are supporting the fact some buyers are just tired of waiting and making life decisions to purchase. Cash buyers are also contributing to steady the market.

“The current month supply of homes is 9.6 months (higher than most Colorado communities).

May average days on market dropped slightly to 111 days. With less inventory in median and average sales prices, average days on market will surely increase in the coming months as higher price point sales are softening due to large inventory. The summer real estate market in Pagosa Springs is aligning to be a playoff between buyers and sellers. Today, neither is favored as each has their challenges and apprehensions with aspirations toward a more balanced market,” said Pagosa Springs-area REALTOR® Wen Saunders.

PUEBLO COUNTY

“If Pueblo County’s housing market were a rodeo, buyers and sellers are both still in the arena—but everyone seems to have eased off the throttle just a bit. Compared to May 2025, new listings have dropped just over 8% from 346 to 318. Sold listings fell 15.6% from 218 to 184. With fewer homeowners putting their properties on the market, buyers are also taking a little longer to pull the trigger.

“At the same time, home prices remained surprisingly resilient with the median sales price of $316,500 down just 1.9% year-over-year and the average sales price staying flat at $319,691.

“The good news for sellers, average days on market fell almost 11% from 102 to 91 days. While buyers may be more selective, well-priced homes are still finding new owners faster than they were a year ago.

Home inventory fell 9.6% from 918 to 830 homes pushing the months’ supply of inventory from 5.5 down to 5 months, a dip of just over 9%. Despite the slower sales pace, with fewer homes available, pricing has remained steady.

Looking at the first five months of the year:

- 1,535 new listings compared to 1,540 last year (-0.3%)

- 811 homes sold compared to 799 last year (+1.5%)

- Median price $300,000 (-5.1%)

- Average price $315,760 (-1.9%)

“Pueblo County’s single-family market is showing signs of normalization. Inventory remains somewhat limited, homes are selling faster, but buyers are being more cautious and price-sensitive than they were a year ago. Sellers can still succeed, but the days of throwing a ‘For Sale’ sign in the yard and waiting for offers to magically appear before dinner are mostly behind us.

“For buyers, there may be a little less competition than in previous years, but don’t mistake that for a clearance sale. Well-maintained, appropriately priced homes are still attracting attention,” said Pueblo-area REALTOR® David Ramirez.

SAN LUIS VALLEY

“Alamosa County saw year-to-date sold listings increase 13.5% compared to the same period last year, reflecting continued buyer activity despite a decline in new listings and moderating home prices. Rio Grande County recorded a 21.1% increase in sales, while Conejos County experienced one of the strongest gains in the region with year-to-date sales up 150%, highlighting growing interest in rural southern Colorado properties and lifestyle-driven homeownership. Inventory levels and pricing continue to vary by county, creating opportunities for both buyers and sellers depending on location and property type.

“Inventory remains elevated in many areas across the San Luis Valley, providing buyers with more choices than they have seen in recent years. Costilla County reported a 44.2% increase in new listings year-to-date, while Mineral County saw inventory rise 19% from a year ago. Saguache County maintained a healthy supply of available homes, with months of inventory increasing 12.5% year-over-year. These conditions are helping create a more balanced market, giving buyers additional negotiating power while still allowing well-priced properties to attract strong interest.

“Although market activity varies from county to county, the overall San Luis Valley real estate market continues to demonstrate stability and resilience. Increased inventory, steady sales activity, and the region’s affordability compared to many Colorado mountain and Front Range markets continue to attract buyers seeking primary residences, second homes, investment opportunities, and recreational properties. As we move into the summer selling season, local market data suggests the Valley remains well-positioned for continued real estate activity throughout 2026,” said San Luis Valley-area REALTOR® Megan Bello.

STEAMBOAT SPRINGS/ROUTT COUNTY

“So far in 2026, Steamboat Springs has seen fewer new listings come to market, with single-family inventory down 4.5% and multi-family inventory down 21.9% compared to last year. While the pace of new listings has slowed, overall inventory remains higher than it was a year ago, providing buyers with more choices.

“Steamboat’s single-family market was active with 12 homes selling in May, five more than during the same month last year. However, homes are taking longer to sell. The average days on market for May sales increased to 75 days from 62 days a year ago, while the year-to-date average reached 90 days. Given current inventory levels and the pace of sales, it would not be unusual for a property to remain on the market for six months or longer, depending on its price, location, and condition.

“The multi-family market had 26 closings in May matching last year’s volume. Median and average sales prices increased to $1.96 million and $2.24 million, respectively, driven by closings at the new Amble development.

“The Oak Creek and Stagecoach communities experienced stronger activity than Steamboat in May, with more homes selling than during the same period last year. As a result, year-to-date sales are approximately 50% ahead of last year’s pace. New listings have remained relatively flat however, unlike Steamboat, the inventory of homes for sale is lower than it was a year ago. The median sales price stands at $980,000, with the average sales price at $1,405,563. Homes are taking an average of 116 days to sell, and with 18 homes currently on the market, inventory represents approximately a six-month supply.

“Multi-family opportunities remain limited outside Steamboat city limits. Only six townhomes are currently available in Stagecoach, a community anchored by the popular Stagecoach State Park. The average sales price for a multi-family property in the area is $441,136.

“To the west of Steamboat, Hayden has added nine new listings this year, bringing the total to 27, two more than at this point last year. Sales activity has been the softest among the area’s major markets with just one home sale recorded in May at $455,000 after 159 days on market. Year-to-date, only six homes have sold with 26 available for purchase and providing a 10.4-month supply of inventory. The multi-family market in Hayden mirrors conditions in Oak Creek and Stagecoach, with six units for sale and an estimated five-month supply.

“As the summer selling season gains momentum, buyers are expected to remain selective. Sellers who present their properties in excellent condition and price them competitively will likely be rewarded with stronger interest and faster sales,” said Steamboat Springs-area REALTOR® Marci Valicenti.

SUMMIT, PARK AND LAKE COUNTIES

“Summer visitors are beginning to arrive, and buyers and sellers are testing the waters for what many expect to be a busy season. While inventory is gradually building, prices continue to show resilience across much of the region. Buyers are finding more choices than they had a year ago, but well-positioned properties are still attracting strong interest and commanding healthy prices.

Summit County – May 26 compared to May 25

Single-Family Homes:

• Number of Sales: Up 27%

• Average Price: $2,680,308 a 6% increase, and flat for the 2025 full-year average

• New Listings: Up 20%

Multi-Family Homes:

• Number of Sales: Down 32%

• Average Price: $1,078,281, up 19% and up 4% compared to the 2025 full-year average

• New Listings: Down 15%

Park County – May 26 compared to May 25

- Number of Sales: Up 27%

- Average Price: $679,014 a 10% increase and up 4% compared to the 2025 full-year average

- New Listings: Up 17% from last year

“Across Summit, Park, and Lake counties, 891 residential listings are currently on the market, ranging from a $119,000 single-family home in Park County to a $25 million Breckenridge home. About 42% of active listings are priced above $1 million including 50 listings over $5 million. The average residential list price across the region is $1,599,347.

“In May, 115 residential closings ranged from a $175,000 single-family home in Bailey to a $13 million Breckenridge home. Approximately 58% of sales closed above the $1 million mark, and cash purchases represented 42% of all transactions. Another 249 properties are currently pending.

“As we head into the heart of the summer selling season, the market appears balanced between opportunity and caution. Inventory remains well above the extremely limited levels seen during the pandemic years, giving buyers more options and negotiating power, while continued strength in pricing demonstrates that demand for mountain living remains firmly intact. The growing number of pending sales suggests that many buyers are still moving forward despite economic uncertainty, setting the stage for what could be an active and healthy summer market across Summit, Park, and Lake counties,” said Summit-area REALTOR® Dana Cottrell.

TELLURIDE/SAN MIGUEL COUNTY

“May sales were off significantly with the number of sales at 25 and the dollar amount of sales coming in at $62.71 million. May is somewhat ‘off season” which just means ski season has been over for a month and there are not too many locals here, nor tourists or buyers. This puts the first five months of sales in the Telluride regional market at $330.14 million over 159 transactions. This is 4% more than 2025 with the number of sales down 11% for the same period of time in 2025. The current market is less about a rising tide lifting up every property, but more about a smaller pool of affluent buyers competing for their dream property. This is truly a ‘quality over quantity’ when a well healed buyer finds the property that meets their family’s goals,” said Telluride-area REALTOR® George Harvey.

WELD COUNTY

“The Weld County market is continuing to shift into a more balanced pace as we head into summer. New listings are down 15.9% year-over-year, and sales fell 22% for the month, showing a slower, more cautious buyer pool. Home prices have softened slightly, with the median price at $504,995 (down 2.8%), but values remain relatively stable overall.

Homes are taking a bit longer to sell, averaging 77 days on market, yet sellers are still receiving strong offers at 99.3% of list price when homes are priced well. Inventory remains limited at 2.9 months’ supply, keeping conditions fairly competitive, though far less intense than previous years.

“The condo and townhome market is seeing a bigger slowdown, with fewer sales and longer days on market, creating opportunity for buyers.

“This is a more strategic market. Sellers need to price right, and buyers finally have more time and negotiating power,” said Weld County-area REALTOR® Amy Tallent.

The Colorado Association of REALTORS® Monthly Market Statistical Reports are prepared by Showing Time, a leading showing software and market stats service provider to the residential real estate industry and are based upon data provided by Multiple Listing Services (MLS) in Colorado. The May 2026 reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. CAR’s Housing Affordability Index, a measure of how affordable a region’s housing is to its consumers, is based on interest rates, median sales prices and median income by county.

The complete reports cited in this press release, as well as county reports are available online at: https://www.coloradorealtors.com/market-trends/

###

CAR/SHOWING TIME RESEARCH METHODOLOGY

The Colorado Association of REALTORS® (CAR) Monthly Market Statistical Reports are prepared by Showing Time, a Minneapolis-based real estate technology company, and are based on data provided by Multiple Listing Services (MLS) in Colorado. These reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. Showing Time uses its extensive resources and experience to scrub and validate the data before producing these reports.

The benefits of using MLS data (rather than Assessor Data or other sources) are:

Accuracy and Timeliness – MLS data are managed and monitored carefully.

Richness – MLS data can be segmented

Comprehensiveness – No sampling is involved; all transactions are included.

Oversight and Governance – MLS providers are accountable for the integrity of their systems.

Trends and changes are reliable due to the large number of records used in each report.

Late entries and status changes are accounted for as the historic record is updated each quarter.

The Colorado Association of REALTORS® is the state’s largest real estate trade association representing over 23,000 members statewide. The association supports private property rights, equal housing opportunities and is the “Voice of Real Estate” in Colorado. For more information, visit https://www.coloradorealtors.com.